Johansen Cointegration Test (JCT)

The Johansen Cointegration Test (JCT), developed by Søren Johansen, is a statistical test used to determine whether two or more non-stationary time series are cointegrated. Cointegration implies that although the individual time series may be non-stationary, there exists a linear combination of them that is stationary. This suggests a long-run equilibrium relationship between the series.

Introduction to JCT

- Definition: Cointegration refers to the existence of a stationary linear combination of two or more non-stationary time series. If such a linear combination exists, the series are said to be cointegrated, and they share a common stochastic trend.

- Long-Run Equilibrium: Cointegration suggests that the variables have a long-run equilibrium relationship. Even though the individual series may deviate from this equilibrium in the short run, they will tend to revert back to it over time.

- Testing Framework: The JCT is based on the Vector Autoregressive (VAR) model and uses the rank of the coefficient matrix to determine the number of cointegrating relationships.

- Engle-Granger Two-Step Method: An alternative cointegration test is the Engle-Granger two-step method, but the Johansen test is generally preferred due to its ability to handle multiple cointegrating relationships and its superior statistical properties.

Deep Understanding of JCT

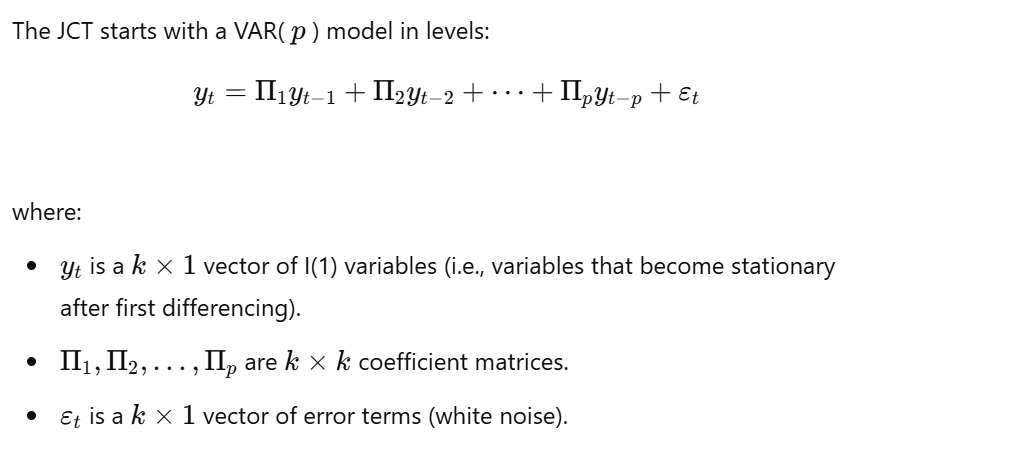

VAR Model as a Starting Point

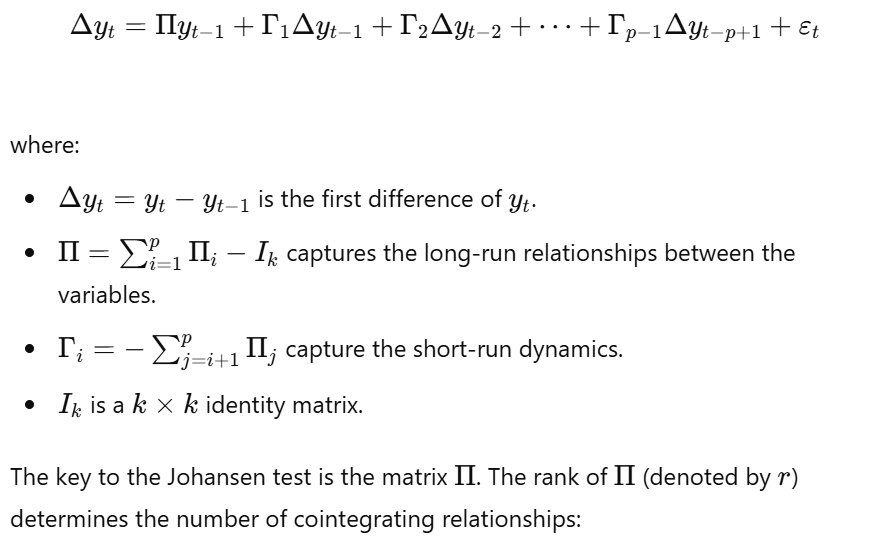

Vector Error Correction Model (VECM)

The VAR model is then reparameterized into a Vector Error Correction Model (VECM):

Test Statistics

The Johansen test uses two test statistics to determine the number of cointegrating relationships:

- Trace Test: Tests the null hypothesis that the number of cointegrating relationships is ( \leq r ) against the alternative that it is greater than ( r ).

- Maximum Eigenvalue Test: Tests the null hypothesis that the number of cointegrating relationships is ( r ) against the alternative that it is ( r + 1 ).

Issues in JCT

- Lag Length Selection: Choosing the appropriate lag length ( p ) for the VAR model is crucial. Information criteria (AIC, BIC, HQIC) are commonly used.

- Deterministic Components: The JCT requires specifying whether to include a constant and/or a trend in the cointegrating relationship and/or the VAR model.

- Distributional Assumptions: The JCT assumes that error terms are normally distributed. Departures from normality can affect test results.

- Small Sample Properties: The JCT can have poor small-sample properties.

- Sensitivity to Outliers: The JCT can be sensitive to outliers.

- Unit Root Tests: It is important to confirm that the variables are I(1) before performing the JCT. Unit root tests such as the Augmented Dickey-Fuller (ADF) test or the Phillips-Perron (PP) test are commonly used.

- Identification of Cointegrating Vectors: The cointegrating vectors are not uniquely identified. Normalization or other restrictions are typically imposed.

- Spurious Cointegration: Cointegration relationships can sometimes be spurious due to common trends or omitted variables.

Hypothesis Testing in JCT

- Specify the Lag Length: Choose ( p ) using information criteria.

- Test for Unit Roots: Confirm that the variables are I(1).

- Choose Deterministic Components: Decide on including a constant and/or a trend.

- Estimate the VAR Model: Estimate the VAR model in levels.

- Perform the Johansen Test: Use the trace test and maximum eigenvalue test.

- Determine the Number of Cointegrating Relationships: Based on test statistics and critical values.

- Estimate the Cointegrating Vectors: Obtain beta and alpha.

- Interpret Results: Analyze the long-run equilibrium relationships and adjustment coefficients.

Software Implementation

Statistical software packages like R, Python, and EViews provide functions for performing the Johansen cointegration test.

Conclusion

The Johansen cointegration test is a valuable tool for determining whether two or more non-stationary time series are cointegrated. However, it is important to carefully consider issues such as lag length selection, deterministic components, and distributional assumptions, and to interpret the results with caution. Cointegration suggests a long-run equilibrium relationship between variables and has important implications for forecasting and policy analysis.

No Comments