Choosing the Right Life Insurance Policy

Selecting the right life insurance policy is crucial for ensuring financial security and meeting long-term financial goals. Different types of life insurance policies offer various benefits depending on individual needs. Below are the primary types of life insurance policies and their key features:

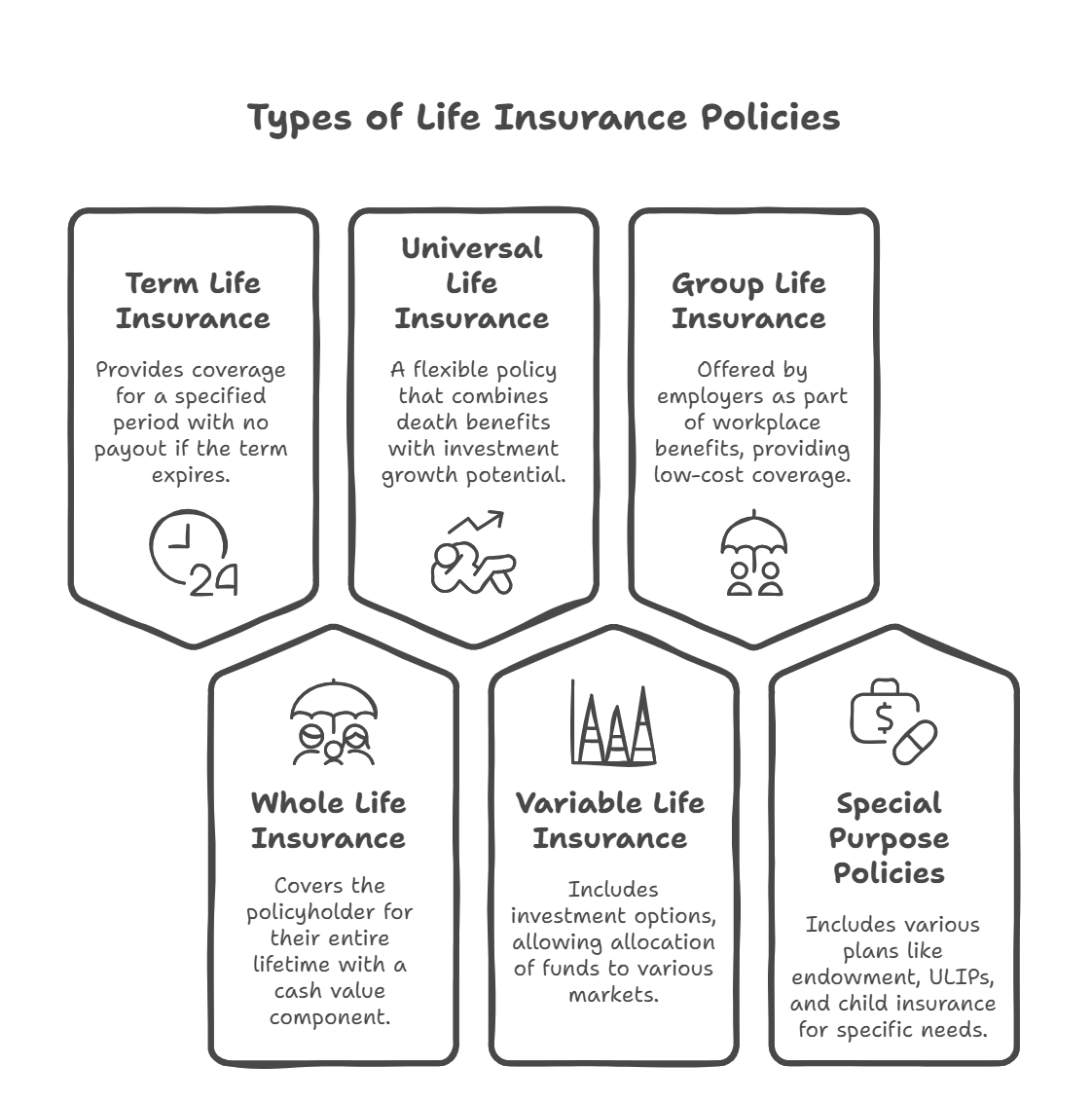

1. Term Life Insurance

Definition

Term life insurance provides coverage for a specified period, such as 10, 20, or 30 years. If the policyholder dies during the term, the beneficiaries receive the death benefit. If the term expires and the policyholder is still alive, there is no payout.

Key Features

- Pure risk coverage with no investment component.

- Affordable premiums compared to other types of life insurance.

- Can be converted into permanent life insurance in some cases.

- Ideal for income replacement during working years.

Example

A 35-year-old individual buys a 20-year term policy with a ₹1 crore sum assured. If they pass away during the policy term, their family receives ₹1 crore. If they survive the term, no payout is made.

2. Whole Life Insurance

Definition

Whole life insurance covers the policyholder for their entire lifetime. It provides a guaranteed death benefit and has a cash value component that grows over time

Key Features

- Lifetime coverage with fixed premiums.

- Accumulates cash value that can be borrowed against.

- Higher premiums than term insurance.

- Useful for estate planning and wealth transfer.

Example

A policyholder pays premiums for 20 years. If they pass away at age 80, their beneficiaries receive the sum assured along with accrued bonuses.

3. Universal Life Insurance

Definition

A flexible life insurance policy that combines death benefits with investment growth potential. Policyholders can adjust their premium payments and death benefits.

Key Features

- Flexibility to modify premiums and coverage amounts.

- Accumulates cash value based on market interest rates.

- Higher premiums than term life insurance but more flexible than whole life policies.

Example

A business owner with fluctuating income can adjust their premium payments as per financial needs while maintaining life coverage.

4. Variable Life Insurance

Definition

A life insurance policy that includes investment options, allowing policyholders to allocate funds to stocks, bonds, and mutual funds.

Key Features

- Investment component with market-based returns.

- Death benefit and cash value depend on market performance.

- High risk and high return potential.

- Suitable for individuals with high-risk tolerance.

Example

A young investor purchases a variable life insurance policy and invests in equity funds. If markets perform well, their policy’s cash value and benefits increase.

5. Group Life Insurance

Definition

A life insurance policy offered by employers to employees as a part of workplace benefits.

Key Features

- Low-cost coverage, often paid partially or fully by employers.

- Limited coverage amount.

- Ends when employment is terminated.

- Ideal as supplementary coverage, not a replacement for personal insurance.

Example

An employer offers a ₹10 lakh group life insurance policy. If an employee passes away while employed, their family receives ₹10 lakh.

6. Other Special Purpose Life Policies

A. Endowment Plans

Combines life insurance with savings, providing a lump sum payout at maturity or upon the policyholder’s death.

B. Unit Linked Insurance Plans (ULIPs)

Offers both investment and insurance benefits, allowing policyholders to invest in equity or debt funds while maintaining life coverage

C. Joint Life Insurance

Covers two individuals under one policy, paying out on the death of either policyholder.

D. Child Insurance Plans

Designed to secure a child’s financial future, offering payouts at different milestones like education and marriage.

E. Pension Plans

Helps individuals accumulate funds for retirement, providing periodic income after retirement age.

Conclusion

Choosing the right life insurance policy depends on personal financial goals, risk tolerance, and long-term security needs. Term insurance is best for affordability, whole life and universal life provide lifelong coverage, while variable life suits risk-taking investors. Special purpose policies like ULIPs and pension plans cater to specific financial objectives

No Comments