Personal Tax Planning

Tax planning is an essential component of financial management that involves using legal provisions to minimize tax liability while ensuring compliance with tax laws. Proper tax planning helps individuals optimize their financial resources, save on taxes, and increase disposable income for investments and future financial security.

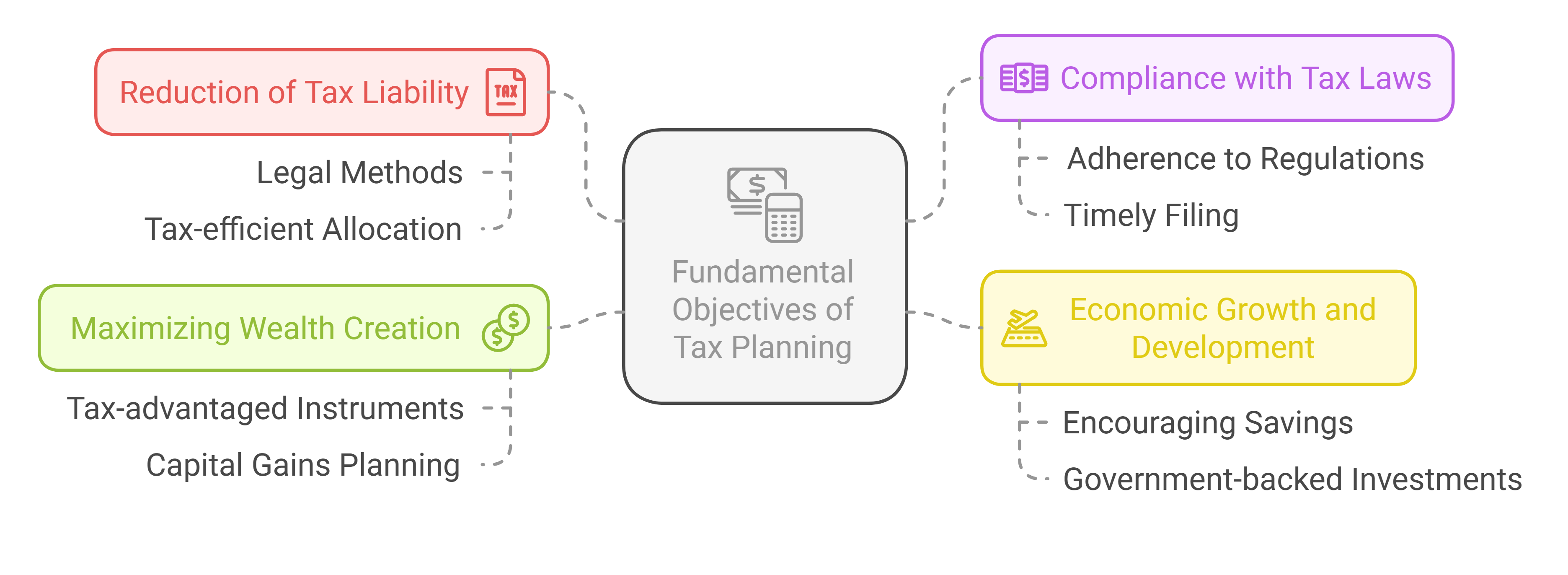

1. Fundamental Objectives of Tax Planning

The key objectives of tax planning include:

A. Reduction of Tax Liability

- Legal methods are used to lower taxable income, such as investing in tax-saving instruments and claiming eligible deductions.

- Ensuring tax-efficient allocation of investments to reduce tax outflow.

B. Compliance with Tax Laws

- Adhering to government regulations to avoid penalties and legal complications.

- Filing income tax returns on time and maintaining proper documentation.

C. Economic Growth and Development

- Encouraging savings and investment in government-backed financial products.

- Supporting national development through tax-efficient investments like Public Provident Fund (PPF) and National Savings Certificates (NSC).

D. Maximizing Wealth Creation

- Efficient tax planning helps individuals accumulate wealth by investing in tax-advantaged financial instruments.

- Strategies like capital gains tax planning and investment in tax-free bonds help in long-term wealth preservation.

2. Tax Structure in India for Individuals

The Indian tax system follows a progressive tax structure, meaning higher-income individuals are subject to higher tax rates.

A. Income Tax Slabs (As per the Latest Tax Regime)

The tax structure for individuals depends on the chosen tax regime:

- New Tax Regime: Lower tax rates with fewer deductions.

- Old Tax Regime: Higher tax rates with multiple deductions under sections like 80C, 80D, and 24(b).

B. Key Components of the Tax Structure

- Income Tax: Levied based on earnings from salary, business, property, capital gains, and other sources.

- Capital Gains Tax: Applied on profits from the sale of capital assets like stocks and real estate.

- Tax Deducted at Source (TDS): Tax collected at the source of income, ensuring compliance before earnings reach the taxpayer.

- Wealth Tax (Abolished in 2015): Previously applicable on net wealth exceeding ₹30 lakh.

C. Key Tax-Saving Sections in India

- Section 80C: Investments in PPF, NSC, ELSS, tax-saving fixed deposits (FDs), and life insurance premiums allow deductions up to ₹1.5 lakh.

- Section 80D: Provides deductions for health insurance premiums paid for self, family, and parents.

- Section 24(b) & 80EEA: Interest paid on home loans is eligible for tax benefits.

- Section 10(14): Certain allowances like House Rent Allowance (HRA) are exempt from tax.

3. Common Tax Planning Strategies

A. Maximizing Deductions

- Section 80C: Tax deductions up to ₹1.5 lakh for investments in PPF, EPF, NSC, tax-saving FDs, and life insurance.

- Section 80D: Health insurance premium deductions (Up to ₹75,000 for senior citizens).

- Home Loan Interest (Section 24B): Interest on home loans deductible up to ₹2 lakh.

- Education Loan (Section 80E): Tax benefits on education loan interest.

B. Income Shifting Strategies

- Transferring assets to family members in lower tax brackets to minimize overall tax liability.

- Setting up a Hindu Undivided Family (HUF) to distribute income efficiently.

- Gifting money to parents or spouse: Investments made from their income may attract lower or no tax.

C. Tax-Free and Tax-Deferred Income

-

Tax-Free Income:

- Interest from PPF and Sukanya Samriddhi Yojana.

- Dividends from agricultural income.

- Maturity amount of life insurance policies under Section 10(10D).

-

Tax-Deferred Income:

- National Pension System (NPS), where tax is deferred until withdrawal.

- Capital gains reinvested under Sections 54 and 54EC.

No Comments