Planning for Retirement

Retirement planning is a crucial component of personal financial planning, ensuring financial security and independence after an individual stops working. A well-structured retirement plan helps maintain a comfortable standard of living and provides for healthcare, lifestyle, and unexpected expenses.

1. Role of Retirement Planning in Personal Financial Planning

Retirement planning is an essential aspect of personal financial management. It involves accumulating sufficient savings and investments to support one’s lifestyle after retirement.

1.1 Why Retirement Planning is Important?

- Longevity Increase – With life expectancy rising, retirees need more savings to sustain themselves.

- Inflation Impact – The cost of living will continue to rise, reducing purchasing power over time.

- Reduced Dependence on Family – The traditional joint family system is declining, making self-reliance necessary.

- No Guaranteed Pension – Many private-sector employees do not receive pensions, necessitating personal savings.

1.2 How Retirement Planning Integrates with Financial Planning?

Retirement planning is closely linked to other financial goals, such as:

- Wealth Accumulation – Saving and investing in assets that provide returns above inflation.

- Risk Management – Ensuring adequate insurance coverage for medical and emergency needs.

- Tax Planning – Utilizing tax-efficient investment options to maximize savings.

2. Pitfalls to Sound Retirement Planning

Many individuals make mistakes that impact their retirement security. The most common pitfalls include:

2.1 Starting Late

- The earlier one starts saving, the less one needs to contribute each month.

- Example: A 25-year-old investing ₹2,000 per month for 10 years at 10% annual return will accumulate more than a 35-year-old investing ₹5,000 per month for 10 years.

2.2 Underestimating Future Expenses

- Many retirees underestimate costs such as healthcare, leisure, and inflation-adjusted daily living expenses.

- Example: ₹30,000 of expenses today will become ₹96,000 per month in 30 years at 4% inflation.

2.3 Ignoring Inflation

- Inflation erodes purchasing power, making it crucial to invest in assets that offer returns above inflation.

- Fixed deposits and savings accounts alone may not be sufficient for long-term wealth accumulation.

2.4 Relying Solely on Employer Benefits

- Many assume that Employee Provident Fund (EPF) and gratuity will be sufficient. However, these may not be adequate for covering post-retirement needs.

- Government pension schemes are not available to private-sector employees who joined after 2004.

2.5 Lack of Asset Diversification

- Investing in a single asset class (such as only real estate or fixed deposits) can limit growth potential.

- A balanced portfolio includes equities, debt instruments, real estate, and fixed-income securities.

3. Estimating Income Needs for Retirement

3.1 Factors Influencing Retirement Income Needs

- Current Monthly Expenses – A good rule is to assume 70-80% of pre-retirement expenses will continue post-retirement.

- Healthcare Costs – Medical expenses typically increase after retirement.

- Inflation Adjustment – Future expenses must be projected using an estimated inflation rate.

- Planned Lifestyle – Whether an individual plans to travel, buy property, or engage in leisure activities impacts income needs.

3.2 How to Calculate Required Retirement Corpus?

A basic formula for estimating the required corpus:

Retirement Corpus = (Annual Expenses at Retirement × Expected Retirement Duration) / (Expected Rate of Return - Inflation Rate)

Example Calculation

- Current Expenses: ₹50,000 per month

- Retirement Age: 60

- Life Expectancy: 85

- Inflation Rate: 6%

- Expected Return on Investment: 8%

- Annual Expenses at Retirement: ₹1,42,000 per month (₹17,04,000 per year)

- Retirement Corpus Needed: ₹3.5 to ₹4 crore.

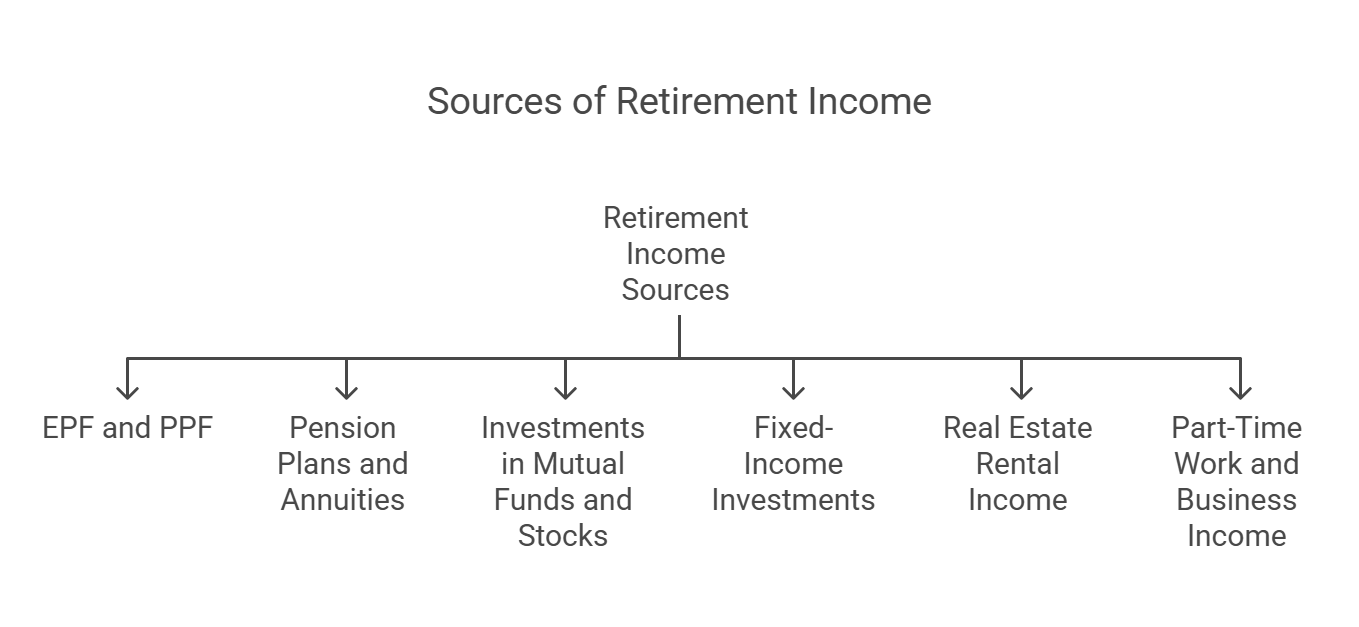

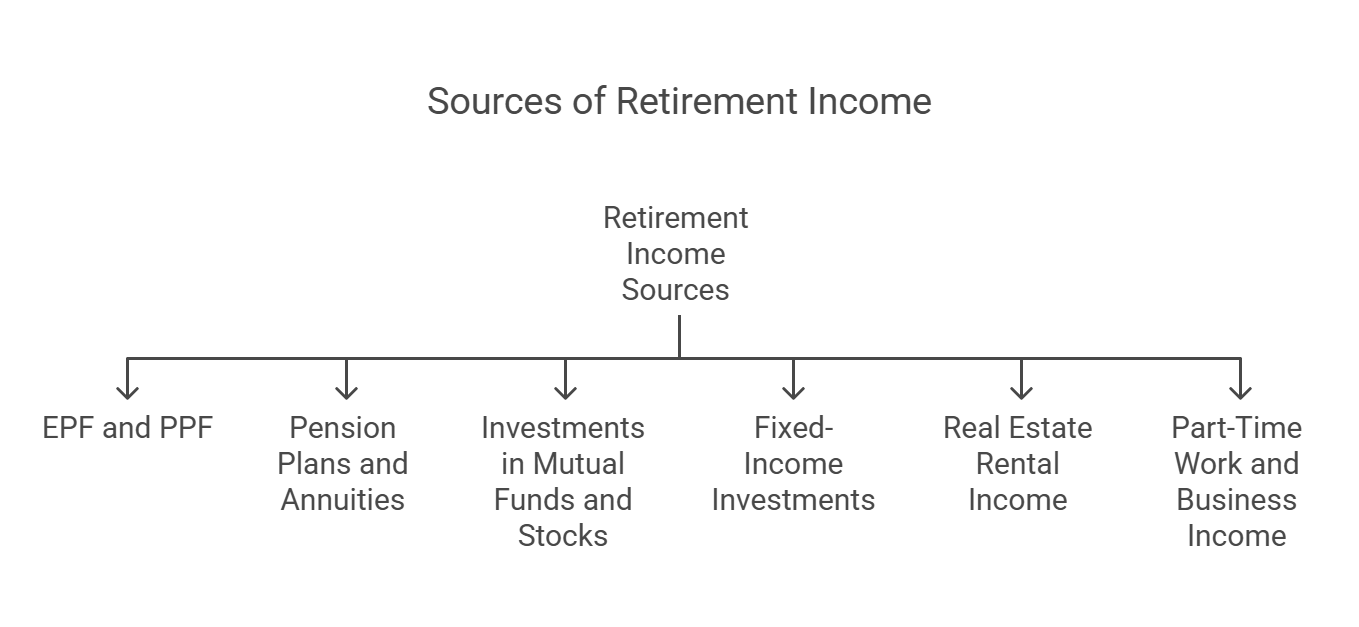

4. Sources of Retirement Income

To ensure financial stability in retirement, individuals must plan multiple income streams:

4.1 Employee Provident Fund (EPF) and Public Provident Fund (PPF)

- EPF is a compulsory savings scheme for salaried employees with both employer and employee contributions.

- PPF is a government-backed savings scheme offering tax-free returns, suitable for self-employed individuals.

4.2 Pension Plans and Annuities

- National Pension System (NPS): A government-backed pension scheme with tax benefits.

- Insurance-Based Pension Plans: Offered by insurance companies to provide guaranteed annuity payments.

- Immediate and Deferred Annuities: Provide a regular payout after investing a lump sum.

4.3 Investments in Mutual Funds and Stocks

- Equity Mutual Funds: Long-term investments that beat inflation.

- Debt Mutual Funds: Provide stable returns with lower risk.

- Dividend Stocks: Offer passive income from company profits.

4.4 Fixed-Income Investments

- Senior Citizens Savings Scheme (SCSS): A government-backed scheme offering higher interest rates for retirees.

- Fixed Deposits (FDs): Provide fixed returns but may not beat inflation.

- Government Bonds: Safe investment options with predictable returns.

4.5 Real Estate Rental Income

- Owning rental properties can provide a steady monthly income, but requires management and maintenance.

- Reverse Mortgage: A scheme where retirees can mortgage their home to receive periodic payments.

4.6 Part-Time Work and Business Income

- Some retirees prefer to continue working part-time or start small businesses to supplement income.

- Consulting, freelancing, or teaching are popular options.

Conclusion

Retirement planning is not just about saving money but also about investing wisely to ensure financial security. A well-structured plan should:

- Start early to take advantage of compounding.

- Account for inflation and rising expenses.

- Diversify investments across multiple asset classes.

- Consider various income sources like EPF, PPF, pension plans, real estate, and equities.

By preparing for retirement systematically, individuals can enjoy a comfortable and financially independent post-retirement life.

No Comments