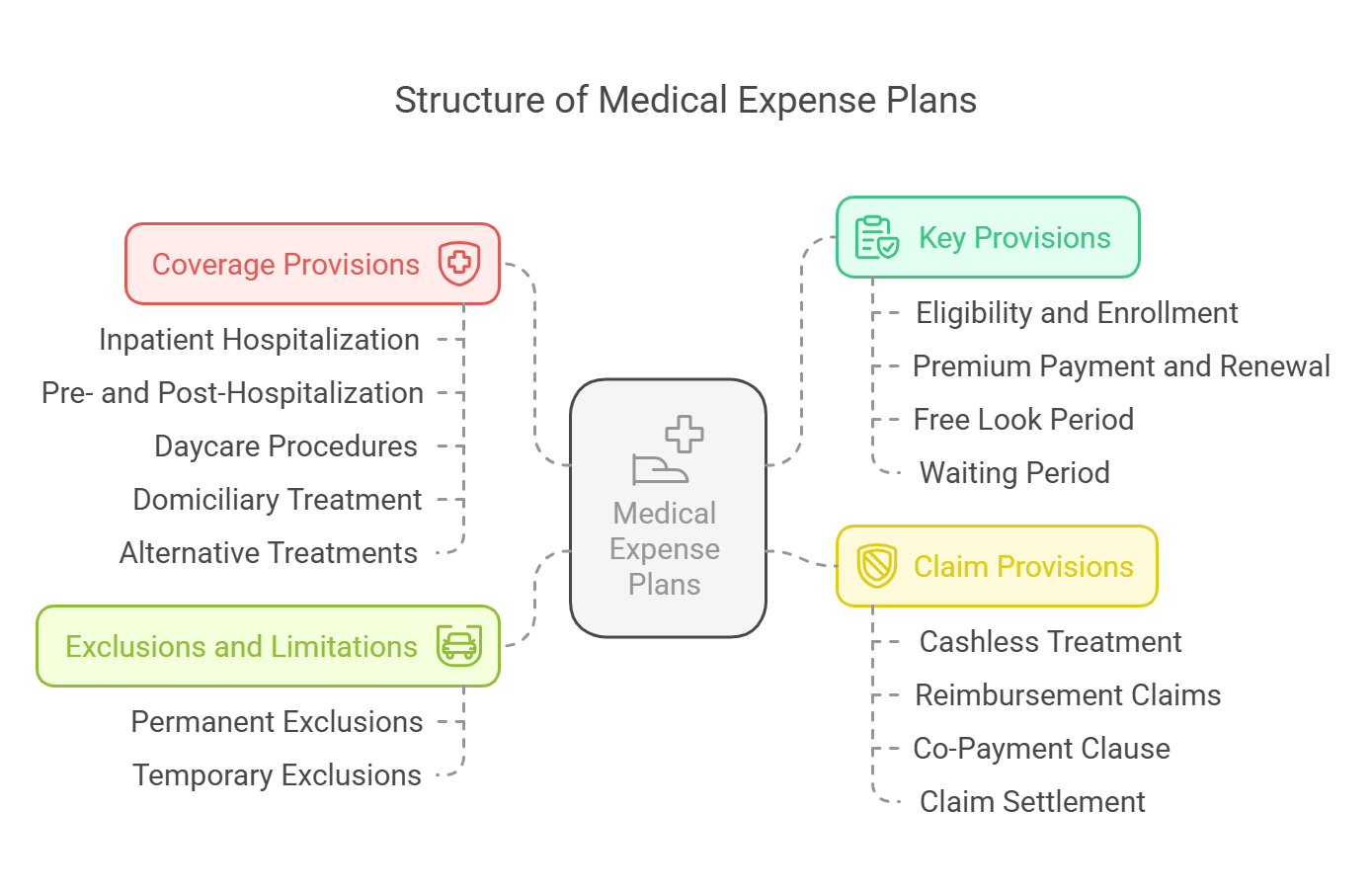

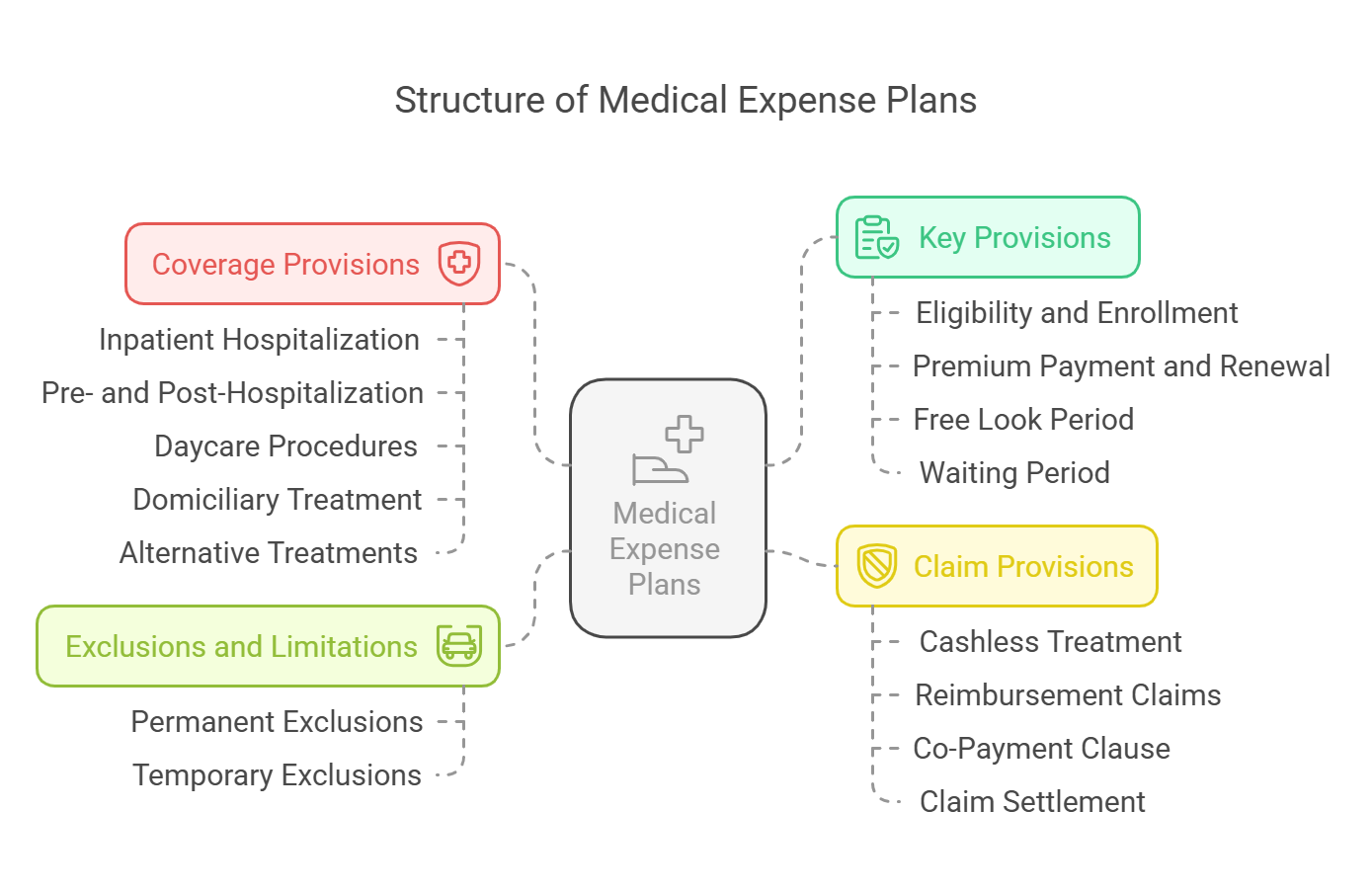

Policy Provisions of Medical Expense Plans

Medical expense plans contain several provisions that define the policyholder’s rights, coverage limits, claim procedures, and insurer obligations. Understanding these provisions helps in selecting the right health insurance plan and avoiding claim rejections.

1. Key Provisions in Medical Expense Plans

A. Eligibility and Enrollment

- Policies define the minimum and maximum age for enrollment.

- Some policies require medical check-ups based on age and pre-existing conditions.

- Coverage may be extended to spouse, children, and dependent parents.

B. Premium Payment and Renewal

- Policies are renewable annually, for a fixed term (5–10 years), or lifelong.

- Non-payment of premiums within the grace period (usually 15-30 days) results in policy lapse.

- Some insurers offer premium discounts for no-claim years.

C. Free Look Period

- New policyholders have a 15–30 day free look period to cancel the policy if unsatisfied.

- Full refunds are provided, minus administrative charges.

D. Waiting Period

- A waiting period applies to certain conditions:

- Pre-existing diseases: 2 to 4 years.

- Maternity benefits: 9 months to 4 years.

- Specific treatments (cataract, hernia, knee replacement, etc.): 1 to 2 years.

2. Coverage Provisions

A. Inpatient Hospitalization Coverage

- Covers room rent, ICU charges, doctor consultations, surgeries, and medicines.

- Some policies impose room rent sub-limits, which may lead to out-of-pocket expenses if exceeded.

B. Pre- and Post-Hospitalization Expenses

- Covers expenses before hospitalization (diagnostics, doctor consultations) and after discharge (medications, follow-ups).

- Typically, insurers cover 30–60 days before hospitalization and 60–90 days post-hospitalization.

C. Daycare Procedures

- Covers short-term treatments like cataract surgery, chemotherapy, and dialysis that don’t require 24-hour hospitalization.

D. Domiciliary Treatment

- Covers home-based treatments when hospitalization is not possible due to medical conditions or lack of hospital beds.

E. Alternative Treatments (AYUSH Coverage)

- Some policies cover Ayurveda, Homeopathy, and Naturopathy treatments under specific conditions.

3. Claim Provisions

A. Cashless Treatment vs. Reimbursement

- Cashless Claims: The insurer directly settles hospital bills with network hospitals.

- Reimbursement Claims: The policyholder pays first and submits bills for reimbursement.

B. Co-Payment Clause

- Requires policyholders to pay a percentage of the claim amount (e.g., 10-20%), reducing premiums but increasing out-of-pocket costs.

C. Claim Settlement and Documentation

- Essential documents include:

- Claim form

- Hospital bills

- Doctor’s reports

- Pharmacy receipts

- Insurers settle claims within 30 days after verification.

D. Sub-Limits on Coverage

- Some policies restrict payouts on specific treatments (e.g., ₹50,000 for cataract surgery).

- Important to check sub-limits to avoid unexpected expenses.

4. Exclusions and Limitations

A. Permanent Exclusions

Most policies do not cover:

- Cosmetic surgeries (except reconstructive procedures).

- Self-inflicted injuries or drug abuse-related illnesses.

- Treatments for HIV/AIDS and STDs (unless covered under specific policies).

B. Temporary Exclusions

- Some diseases are excluded for the first 1-4 years but covered later.

- Waiting periods apply to pre-existing conditions and maternity benefits.

Example: Understanding Policy Provisions in Real Life

Case Study: Mr. Ramesh’s Health Insurance Claim

- Policy Type: Family floater policy with ₹10 lakh sum insured.

- Hospitalization: Admitted for heart surgery costing ₹5 lakh.

-

Policy Provisions Applied:

- Pre-approval for cashless claim at network hospital.

- Room rent capped at ₹5,000/day (exceeded limit, so extra paid out-of-pocket).

- Post-hospitalization expenses covered for 60 days (₹30,000 reimbursed).

Total Claim Processed: ₹4.7 lakh (after deductions).

Conclusion

Understanding policy provisions of medical expense plans ensures better financial protection and hassle-free claim settlements. Choosing a policy with comprehensive coverage, minimal exclusions, and high claim settlement ratios is essential for long-term security.

No Comments