Life Insurance Contract Features

A life insurance contract is a legally binding agreement between the policyholder and the insurer, ensuring financial protection for the insured’s beneficiaries. Understanding its features helps policyholders make informed decisions regarding their coverage.

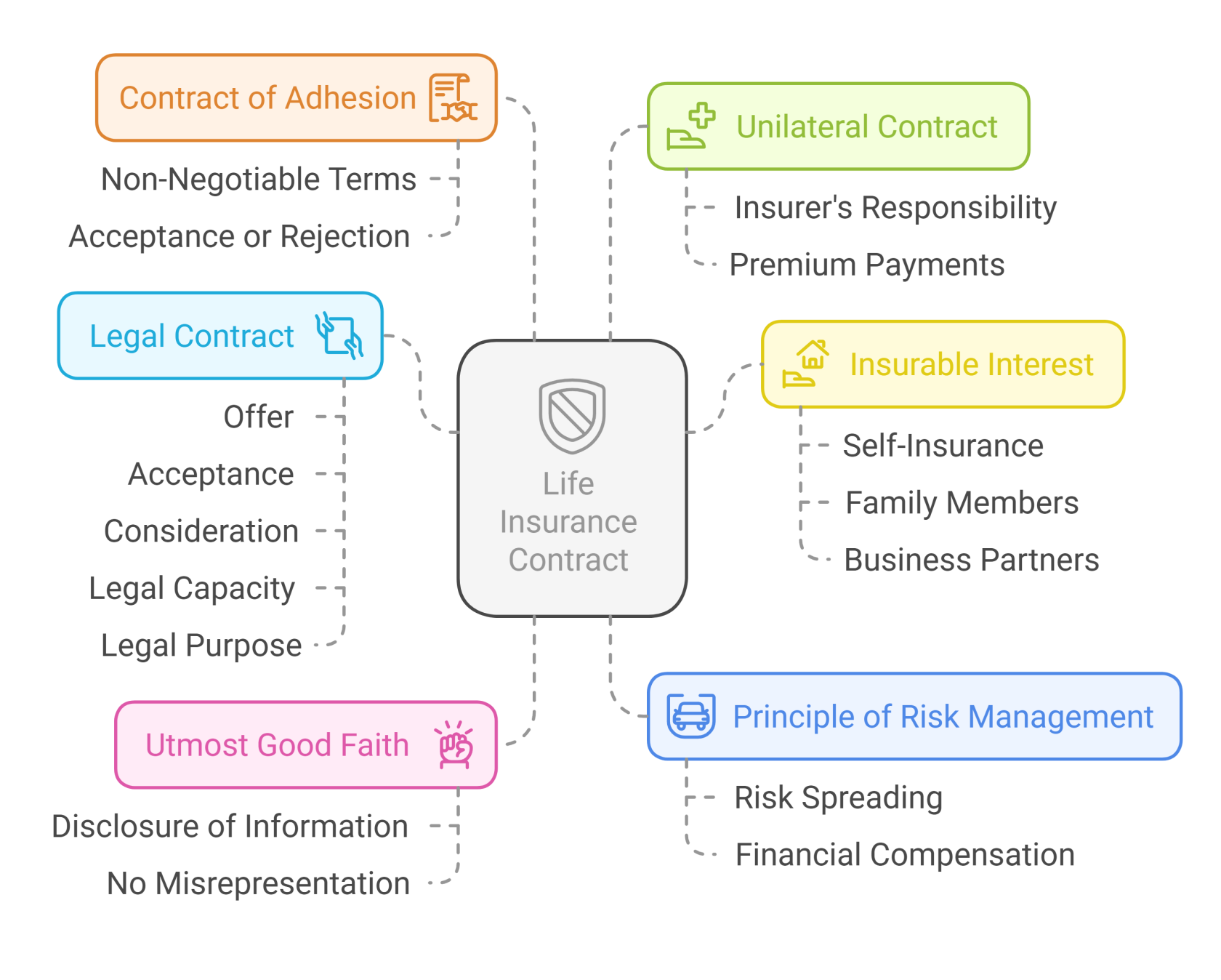

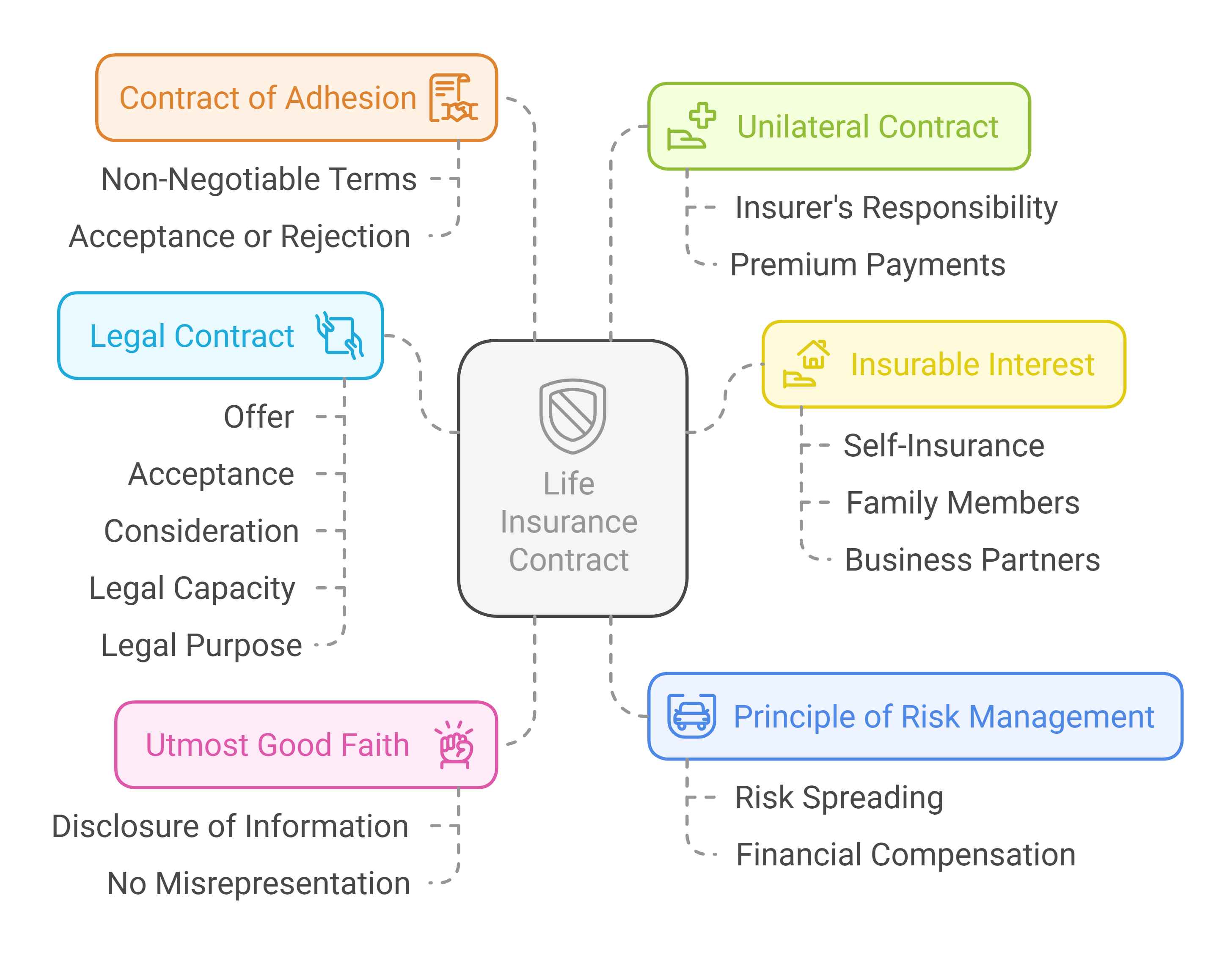

1. Essential Features of a Life Insurance Contract

A. Utmost Good Faith (Uberrimae Fidei)

- Both the policyholder and insurer must act in good faith, fully disclosing all relevant information.

- Any misrepresentation or non-disclosure of facts (e.g., pre-existing medical conditions) may result in claim rejection.

B. Legal Contract

- A life insurance policy is a legally enforceable agreement governed by contract law.

- It requires:

- Offer – The applicant submits a proposal form.

- Acceptance – The insurer accepts the proposal after evaluating risks.

- Consideration – Premiums paid by the insured.

- Legal Capacity – Both parties must be legally competent.

- Legal Purpose – The contract must not involve illegal activities.

C. Insurable Interest

- The policyholder must have a financial or emotional stake in the insured person’s life.

- Common relationships with insurable interest:

- Self-insurance

- Spouses, children, and parents

- Business partners in key-man insurance.

D. Principle of Risk Management

- Life insurance spreads the risk across multiple policyholders, ensuring financial compensation to the insured's beneficiaries upon an unfortunate event.

E. Contract of Adhesion

- The insurance company drafts the contract, and the policyholder can either accept or reject it but cannot negotiate terms.

F. Unilateral Contract

- Only the insurer has a legal obligation to honor the claim, provided the policyholder pays premiums as agreed.

2. Important Clauses in a Life Insurance Contract

A. Free Look Period

- Policyholders can cancel the policy within 15–30 days of purchase if dissatisfied, receiving a refund minus administrative charges.

B. Grace Period

- Insurers provide a 30-day grace period for premium payments (15 days for monthly mode policies).

- If the premium remains unpaid after this period, the policy may lapse.

C. Nomination and Assignment Clause

- Nomination: The policyholder appoints a beneficiary to receive the sum assured in case of their demise.

- Assignment: Rights of the policy can be transferred to another individual or entity (e.g., using life insurance as collateral for a loan).

D. Surrender and Paid-Up Value

- Surrender Value: If a policyholder terminates the policy early, they receive a reduced payout.

- Paid-Up Policy: If premiums are discontinued after a certain period, the policy remains active with a reduced sum assured.

E. Exclusions Clause

- Specifies situations where claims will not be honored, such as:

- Suicide within the first year of the policy.

- Death due to involvement in illegal activities.

- Pre-existing medical conditions not disclosed.

Claim Settlement Process

- Claim Intimation – The beneficiary informs the insurer of the insured’s death.

- Submission of Documents – Required documents include the policy document, death certificate, and hospital records.

- Claim Verification – The insurer verifies details and may conduct investigations.

- Claim Approval & Payout – If valid, the claim is settled within 30 days.

Example: Understanding a Life Insurance Contract

Scenario:

Mr. Sharma, a 40-year-old, buys a 20-year term insurance policy with a sum assured of ₹1 crore.

- He pays annual premiums of ₹10,000 and names his wife as the nominee.

- If he dies in the 5th year, his wife receives ₹1 crore as per the nomination clause.

- If he stops paying premiums after 3 years, the policy lapses unless converted to a paid-up policy.

- If he surrenders the policy, he gets a surrender value, which is significantly lower than the sum assured.

Conclusion

Understanding the features of a life insurance contract ensures policyholders choose the right coverage while being aware of their rights and obligations. Life insurance offers financial security, but policy terms must be carefully reviewed to maximize benefits.

No Comments