Insuring Health

Health insurance plays a vital role in financial planning, ensuring individuals and families receive adequate medical care without suffering from financial hardship. Rising healthcare costs, increased medical emergencies, and evolving lifestyles make health insurance an essential aspect of financial security.

What is Health Insurance?

Health insurance is a contract between an individual and an insurance provider where the insurer covers medical expenses in exchange for periodic premium payments. It includes hospitalization, outpatient treatment, critical illness coverage, and preventive healthcare benefits.

1. Why is Health Insurance Important?

A. Protection Against Rising Medical Costs

- Medical expenses have been increasing due to inflation, advancements in treatment, and increased demand for healthcare services.

- A single hospitalization can lead to substantial expenses, which health insurance can cover.

B. Financial Security for Families

- Covers hospitalization costs, doctor consultations, diagnostic tests, surgeries, and post-hospitalization expenses.

- Protects family savings and prevents financial stress during medical emergencies.

C. Access to Quality Healthcare

- Enables policyholders to receive treatment in reputed hospitals without worrying about costs.

- Includes coverage for cashless hospitalization and reimbursement for treatments.

D. Covers Pre- and Post-Hospitalization Expenses

- Many health insurance plans cover expenses incurred before hospitalization (diagnostic tests, check-ups) and after hospitalization (medicines, follow-up visits).

- Some plans also cover alternative treatments like Ayurveda, Homeopathy, and Naturopathy.

E. Critical Illness and Long-Term Care Benefits

- Special policies cover life-threatening diseases like cancer, stroke, and kidney failure.

- Provides a lump sum payout upon diagnosis of a critical illness, helping with medical and non-medical expenses.

F. Income Tax Benefits (Section 80D)

- Policyholders can claim tax deductions for health insurance premiums paid for self, spouse, children, and parents.

- Tax deduction limit:

- ₹25,000 for individuals (below 60 years)

- ₹50,000 for senior citizens.

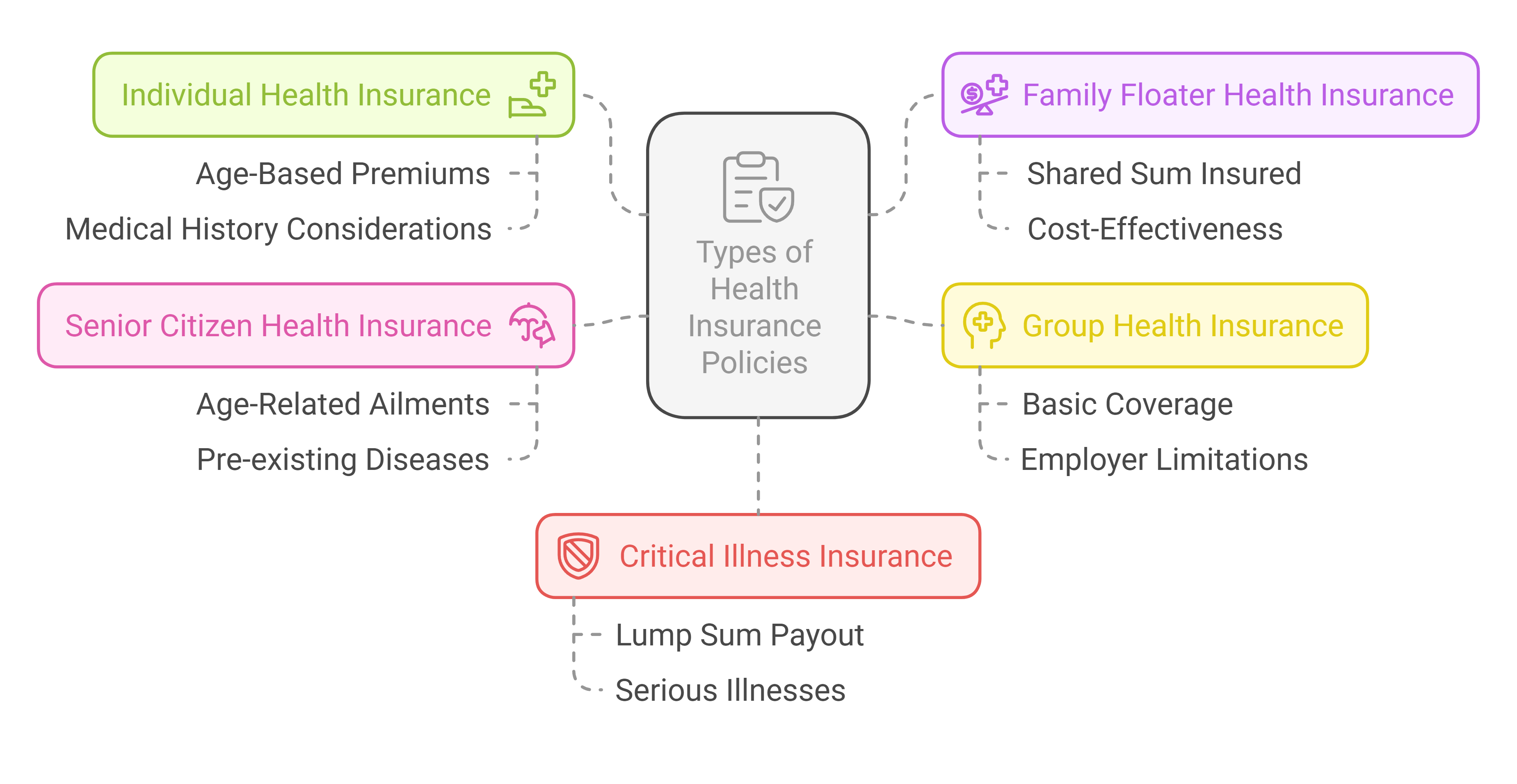

Types of Health Insurance Policies

A. Individual Health Insurance

- Covers medical expenses for a single person.

- Premiums are based on age, medical history, and sum insured.

B. Family Floater Health Insurance

- Covers all family members under a single policy.

- The sum insured is shared among family members, making it cost-effective.

C. Group Health Insurance

- Provided by employers for their employees.

- Offers basic coverage but may have limitations compared to individual policies.

D. Senior Citizen Health Insurance

- Designed for individuals aged 60 years and above.

- Covers age-related ailments, higher hospitalization costs, and pre-existing diseases.

E. Critical Illness Insurance

- Provides a lump sum payout upon diagnosis of serious illnesses like cancer, heart disease, or organ failure.

- Helps manage expenses not covered by standard health insurance.

Key Factors to Consider When Choosing a Health Insurance Policy

A. Sum Insured

- Choose an adequate sum insured to cover major medical expenses.

- Urban residents may need higher coverage due to expensive healthcare facilities.

B. Network Hospitals and Cashless Facility

- Select an insurer with a wide hospital network to avail cashless treatment.

- Ensures hassle-free hospitalization without out-of-pocket expenses.

C. Waiting Period for Pre-Existing Diseases

- Many policies impose a waiting period (2–4 years) for coverage of pre-existing conditions like diabetes or hypertension.

- Choose a policy with a shorter waiting period if you have existing health conditions.

D. Sub-Limits and Co-Payment Clause

- Sub-limits: Some policies have limits on room rent, ICU charges, or specific treatments.

- Co-payment: The insured may have to bear a percentage of the claim amount, reducing premium costs but increasing out-of-pocket expenses.

E. No-Claim Bonus (NCB)

- If no claim is made in a policy year, the sum insured may increase without additional premium costs.

- Encourages policyholders to maintain good health.

Example: Importance of Health Insurance in Real Life

Case Study: Mr. Ramesh’s Medical Emergency

- Scenario: Mr. Ramesh, a 45-year-old salaried employee, was diagnosed with a heart condition requiring bypass surgery costing ₹6 lakh.

- Without Health Insurance: He had to withdraw from savings and take a loan, affecting his financial stability.

- With Health Insurance: His family floater health policy covered 100% of hospitalization expenses, ensuring financial security.

Key Learning: Investing in adequate health insurance prevents financial stress during medical emergencies.

Conclusion

Health insurance is a critical aspect of financial planning, offering protection against rising medical costs, ensuring quality healthcare, and providing tax benefits. Choosing the right policy based on individual and family needs ensures long-term financial security.

No Comments