Types of Medical Expense Coverage

Medical expense coverage refers to the various types of health insurance policies designed to cover medical costs arising from illnesses, accidents, and hospitalizations. These plans provide financial protection against high healthcare costs and ensure access to quality medical treatment.

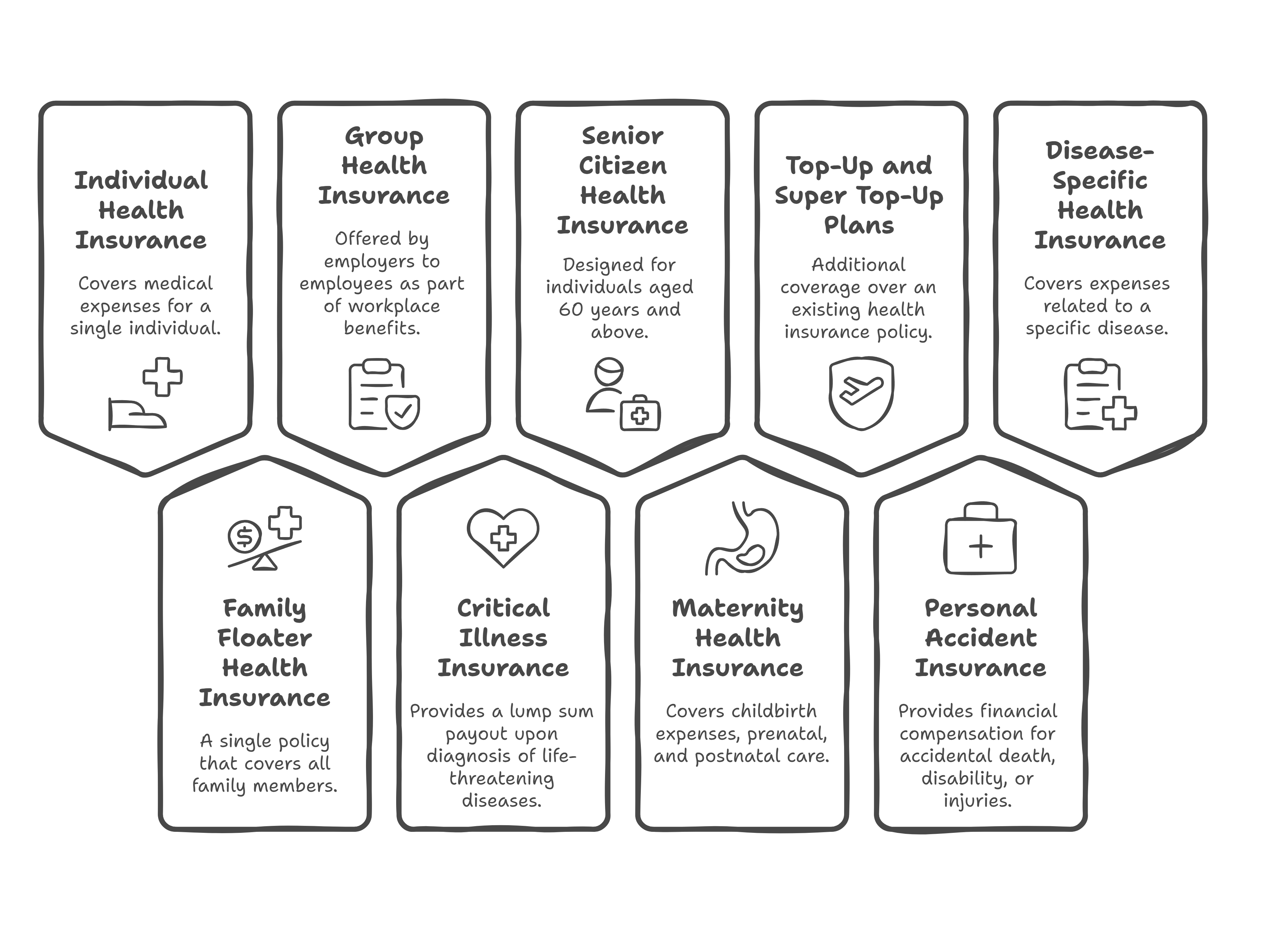

1. Individual Health Insurance

Definition

- Covers medical expenses for a single individual.

- Provides financial security against hospitalization, surgeries, and treatments.

Features

- The policyholder pays premiums based on age, medical history, and sum insured.

- Covers hospitalization, pre- and post-hospitalization expenses, and diagnostics.

- Ideal for self-employed individuals or those without employer-provided coverage.

Example

A 30-year-old buys a ₹10 lakh individual health insurance policy. If they are hospitalized for appendicitis surgery costing ₹3 lakh, the insurer covers the bill as per policy terms.

2. Family Floater Health Insurance

Definition

- A single policy that covers all family members.

- The sum insured is shared among the insured individuals.

Features

- Cost-effective as it provides coverage for multiple members under one plan.

- Covers spouse, children, and sometimes dependent parents.

- The premium is based on the age of the eldest family member.

Example

A couple buys a ₹20 lakh family floater policy. If the wife undergoes surgery costing ₹5 lakh, the remaining ₹15 lakh is available for other family members within the policy year.

3. Group Health Insurance

Definition

- Offered by employers to employees as part of workplace benefits.

- Provides basic coverage at lower premiums due to risk distribution across employees.

Features

- Covers hospitalization, surgeries, and doctor consultations.

- Some plans cover maternity benefits and pre-existing diseases.

- Ends when employment is terminated.

Example

An IT company provides a ₹5 lakh group health policy to its employees. If an employee is hospitalized due to dengue fever, the insurance covers medical bills up to the insured amount.

4. Critical Illness Insurance

Definition

- Provides a lump sum payout upon diagnosis of life-threatening diseases.

- Covers illnesses such as cancer, stroke, kidney failure, and heart diseases.

Features

- The payout can be used for medical treatment or household expenses.

- Covers costly treatments that regular health insurance may not fully cover.

- No restrictions on hospitalization expenses.

Example

Mr. Sharma is diagnosed with lung cancer. His critical illness policy of ₹25 lakh provides a lump sum amount to cover treatment, medicines, and loss of income.

5. Senior Citizen Health Insurance

Definition

- Designed for individuals aged 60 years and above.

- Covers age-related ailments, surgeries, and pre-existing diseases.

Features

- Higher sum insured due to increased medical risks.

- Covers dental care, vision care, and alternative treatments like Ayurveda and Homeopathy.

- Some policies have higher premiums and co-payment clauses.

Example

A 65-year-old retiree buys a ₹10 lakh senior citizen policy. After a knee replacement surgery costing ₹8 lakh, the insurance covers 80% of the bill, and the remaining amount is co-paid by the insured.

6. Maternity Health Insurance

Definition

- Covers childbirth expenses, prenatal, and postnatal care.

- Includes newborn baby coverage for a specific period.

Features

- Covers normal and C-section deliveries.

- Includes expenses for vaccinations and neonatal care.

- Has a waiting period of 2–4 years before benefits can be claimed.

Example

A couple buys a maternity policy with ₹3 lakh coverage. After a C-section delivery costing ₹2.5 lakh, the insurance covers the expense.

7. Top-Up and Super Top-Up Plans

Definition

- Additional coverage over an existing health insurance policy.

- Top-up plan: Kicks in when the claim amount exceeds the deductible.

- Super top-up plan: Covers multiple claims over a policy year.

Features

- Cost-effective way to increase coverage.

- Requires an existing base policy.

- Ideal for those with high medical expenses.

Example

An individual has a ₹5 lakh base policy and a ₹10 lakh top-up plan with a ₹5 lakh deductible. If hospitalized with a bill of ₹8 lakh, the base policy covers ₹5 lakh, and the top-up covers ₹3 lakh.

8. Personal Accident Insurance

Definition

- Provides financial compensation for accidental death, disability, or injuries.

Features

- Covers permanent and partial disability.

- Pays lump sum benefits based on the severity of the injury.

- Some policies include hospitalization and income loss compensation.

Example

A construction worker loses a limb in an accident. His accident policy provides a ₹10 lakh payout for financial support.

9. Disease-Specific Health Insurance

Definition

- Covers expenses related to a specific disease, such as diabetes, heart conditions, or cancer.

Features

- Designed for individuals with high-risk medical conditions.

- Covers doctor consultations, medications, and hospitalization.

- Has a waiting period for pre-existing conditions.

Example

A diabetic patient buys a disease-specific policy covering insulin, tests, and hospitalization for diabetes-related complications.

Conclusion

Understanding the different types of medical expense coverage helps individuals choose the right health plan based on their age, health risks, and financial needs. Selecting comprehensive coverage ensures financial security during medical emergencies.

No Comments