Making Plans to Achieve Your Financial Goals

Financial planning is a structured process that helps individuals define, prioritize, and achieve their financial goals efficiently. A well-crafted financial plan ensures stability, security, and wealth accumulation across different life stages.

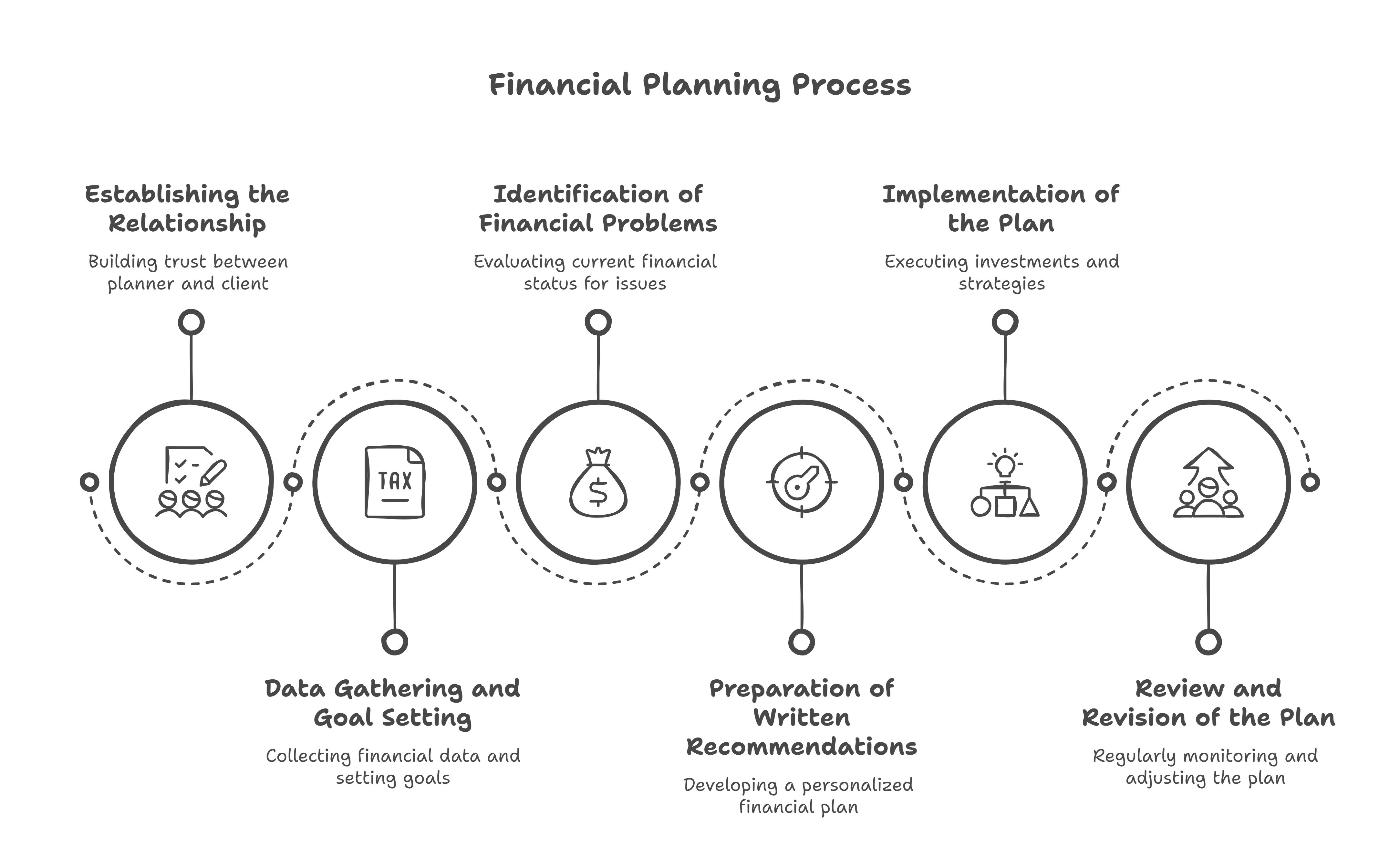

1. Steps in the Financial Planning Process

Step 1: Establishing the Relationship

The first step involves building a relationship of trust between the financial planner and the client. This ensures that the client openly shares their financial details and aspirations. A financial planner must demonstrate professionalism, honesty, and integrity.

Step 2: Data Gathering and Goal Setting

- Identifying financial objectives, categorized as:

- Short-term goals (e.g., buying a car).

- Medium-term goals (e.g., purchasing a house).

- Long-term goals (e.g., retirement planning).

- Gathering quantitative data such as assets, liabilities, income, expenses, and investment history.

- Understanding qualitative aspects such as risk tolerance, financial habits, and personal aspirations.

Step 3: Identification of Financial Problems

- Evaluating the client’s current financial status to identify weaknesses such as:

- Insufficient insurance coverage.

- Mismatch between asset allocation and risk appetite.

- Inadequate emergency funds or liquidity concerns.

- Tax inefficiencies and excessive liabilities.

Step 4: Preparation of Written Recommendations

- Developing a personalized financial plan based on data analysis.

- Incorporating strategic asset allocation based on age, risk profile, and financial objectives.

- Recommending a mix of investments in equity, debt, real estate, and tax-saving instruments.

Step 5: Implementation of the Plan

- The client approves and signs a Letter of Engagement before implementation.

- Execution of investments, insurance purchases, and asset reallocation.

- Debt management strategies, including loan restructuring if required.

Step 6: Review and Revision of the Plan

- Regular monitoring (at least annually) to reassess:

- Changes in income, expenses, or financial goals.

- Market fluctuations impacting investment returns.

- Taxation laws affecting financial planning.

- Portfolio rebalancing to shift underperforming assets and optimize returns.

2. Key Elements of a Financial Plan

A. Defining Clear Objectives

A financial plan should explicitly outline specific goals, including:

- Children’s education – Saving for higher education.

- Retirement planning – Ensuring a secure post-retirement income.

- Home purchase – Accumulating wealth for real estate investments.

- Insurance protection – Mitigating financial risks.

- Wealth transfer – Estate planning to ensure smooth inheritance.

B. Making Assumptions for Long-term Planning

A robust financial plan considers future economic conditions and uncertainties:

- Inflation rate – Impact on purchasing power.

- Expected salary growth – Estimating future earnings.

- Investment returns – Predicting stock, bond, and real estate performance.

- Taxation changes – Adapting to fiscal policy modifications.

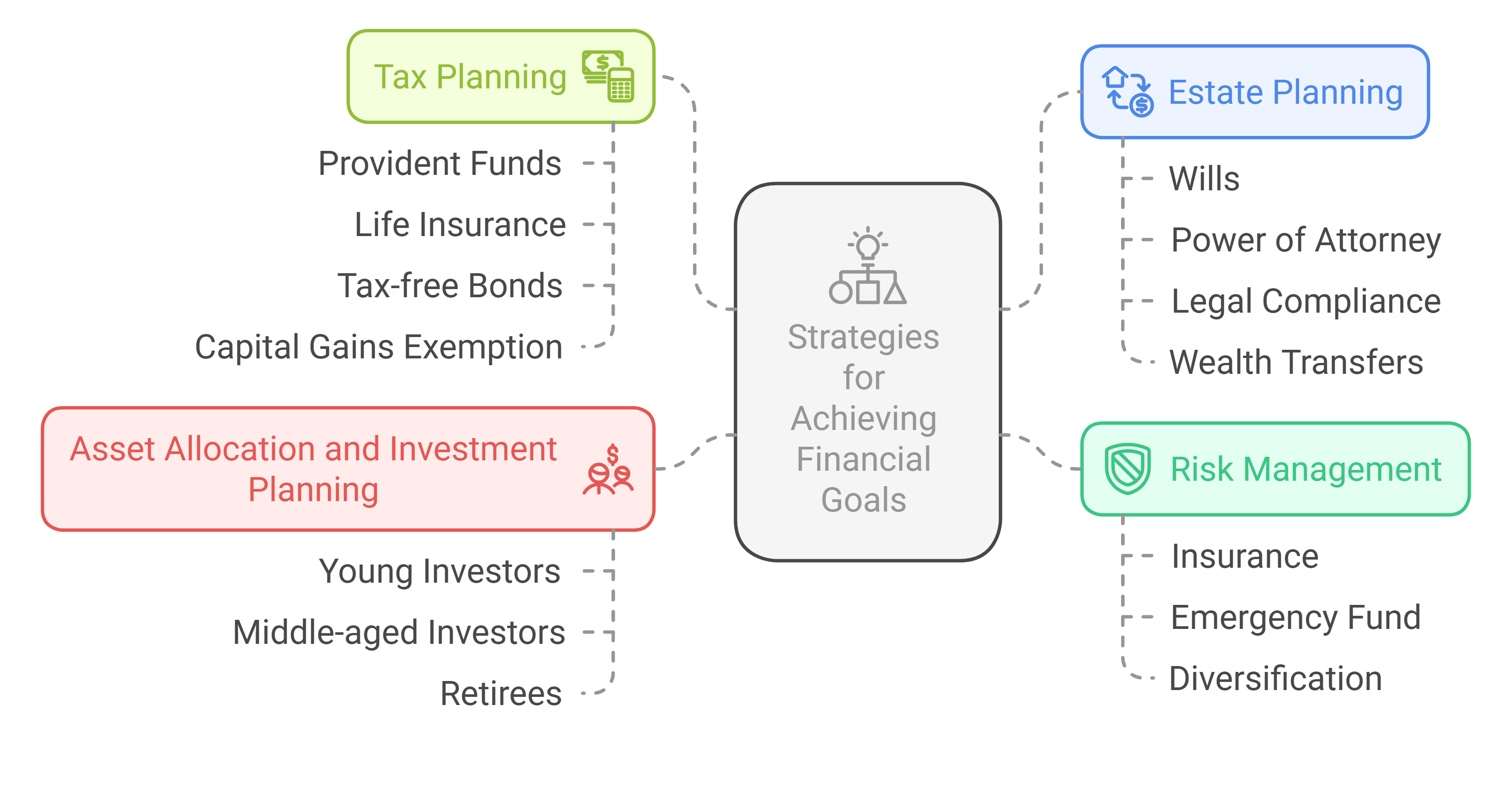

3. Strategies for Achieving Financial Goals

A. Risk Management

- Ensuring adequate life, health, and property insurance.

- Creating an emergency fund to cover unexpected expenses.

- Hedging investment risks through diversification.

B. Asset Allocation and Investment Planning

- Young investors (Aggressive strategy) – High exposure to equities for capital growth.

- Middle-aged investors (Balanced approach) – Diversified portfolio with a mix of equity and fixed-income instruments.

- Retirees (Conservative approach) – Preference for bonds, fixed deposits, and annuities.

C. Tax Planning

- Leveraging tax-saving investment options such as:

- Provident Funds.

- Life insurance.

- Tax-free bonds.

- Capital gains exemption schemes.

D. Estate Planning

- Drafting wills and setting up power of attorney.

- Ensuring legal compliance in asset distribution.

- Planning tax-efficient wealth transfers.

4. Implementation and Execution of the Plan

- Filling out necessary investment forms.

- Adjusting the insurance portfolio based on coverage requirements.

- Establishing periodic check-ins with a financial advisor.

- Ensuring proper documentation for tax and legal purposes.

5. Reviewing and Revising the Plan

- Regular financial check-ups (semi-annual or annual).

- Adjustments due to:

- Market fluctuations.

- Career advancements or salary hikes.

- Major life events (marriage, childbirth, inheritance).

- Rebalancing investments and modifying savings plans accordingly.

A comprehensive financial plan is crucial for achieving financial security and independence. It requires meticulous goal setting, strategic investment decisions, risk management, and ongoing reviews to adapt to economic and personal changes. With a well-structured plan, individuals can navigate their financial journey smoothly and meet their life goals effectively.

No Comments