The Risks and returns of Investing

Investing is essential for wealth creation and financial planning, but it comes with its own set of risks and returns. Understanding these concepts is crucial for making informed investment decisions. This guide covers:

- The Risks of Investing – Different types of risks investors face.

- The Returns from Investing – How investors earn from their investments.

- The Risk-Return Trade-off – The relationship between risk and return.

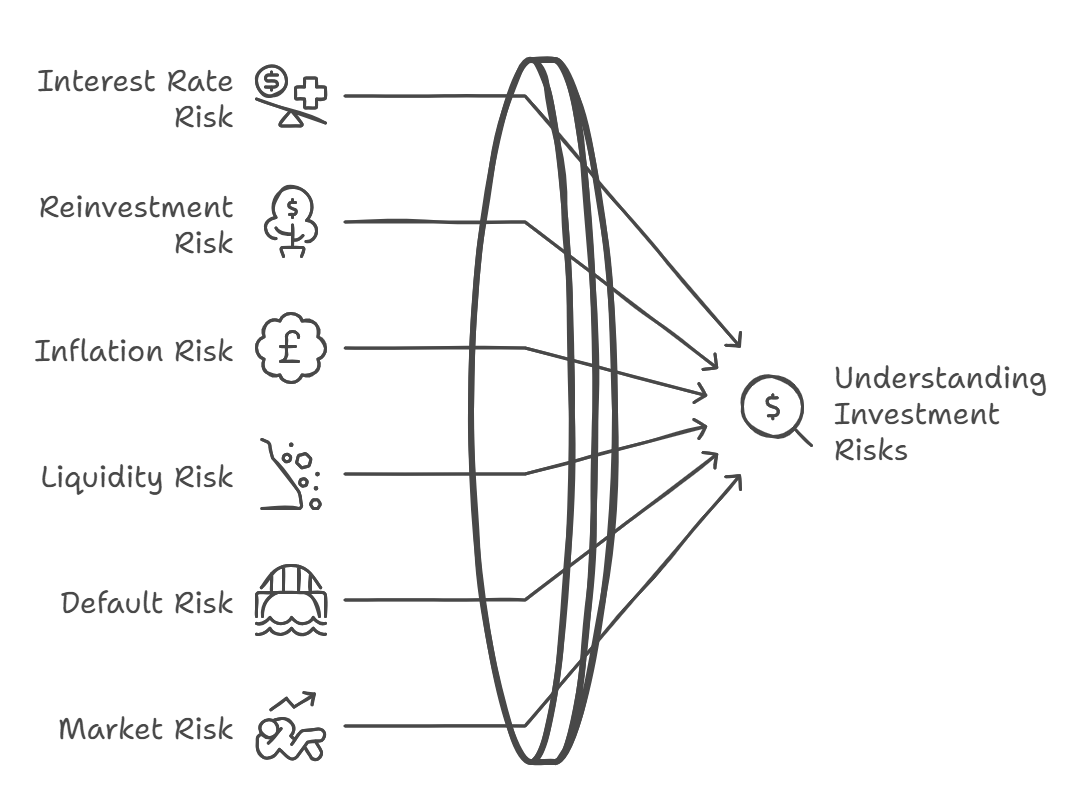

1. The Risks of Investing

All investments carry some degree of risk. Even government-backed securities, considered low-risk, are subject to certain financial risks. The main types of investment risks include:

1.1 Interest Rate Risk

- Interest rates fluctuate over time, affecting bond prices.

- If interest rates rise, existing bonds with lower rates lose value.

- If interest rates fall, older bonds with higher rates become more valuable.

1.2 Reinvestment Risk

- When interest rates fall, reinvested earnings may not yield the same returns.

- Affects bonds and fixed deposits where periodic interest earnings are reinvested at lower rates.

1.3 Inflation Risk (Purchasing Power Risk)

- The real value of money decreases due to inflation.

- Fixed-income investments like bonds and fixed deposits are most affected as they offer fixed returns.

- If inflation rises above the return rate, the investor suffers a negative real return.

1.4 Liquidity Risk

- Liquidity refers to how easily an asset can be converted into cash.

- Some investments (real estate, certain bonds) may be difficult to sell quickly without incurring losses.

1.5 Default Risk (Credit Risk)

- The risk that the borrower or issuer of a bond may fail to pay interest or return the principal.

- Corporate bonds and debt instruments carry this risk, unlike government securities.

1.6 Market Risk (Systematic Risk)

- The risk that investments will lose value due to overall market movements.

- Affects stocks, mutual funds, and equity-based investments.

- Cannot be eliminated but can be mitigated through diversification.

1.7 Call Risk

- If a bond issuer decides to redeem the bond before maturity, investors may need to reinvest at lower interest rates.

- This affects callable bonds where issuers take advantage of lower interest rates.

2. The Returns from Investing

Investment returns are the earnings investors make on their investments. These returns can come from:

2.1 Capital Gains

- Profit made from selling an asset at a higher price than its purchase price.

- Applies to stocks, mutual funds, real estate, and gold investments.

2.2 Interest Income

- Fixed-income securities like bonds, fixed deposits, and savings accounts provide regular interest earnings.

2.3 Dividend Income

- Companies distribute a portion of their profits to shareholders in the form of dividends.

- Dividend-paying stocks provide a passive income stream while allowing for capital appreciation.

2.4 Rental Income

- Real estate investments generate income through rent payments.

2.5 Return on Investment (ROI) Formula

-

ROI helps investors measure the profitability of an investment:

ROI = (Net Profit / Investment Cost) * 100

-

A higher ROI indicates a profitable investment.

2.6 Real Rate of Return (Inflation-Adjusted Returns)

-

The real return considers the impact of inflation.

-

Formula:

Real Return = Nominal Return - Inflation Rate

-

If inflation is higher than the nominal return, the investor loses purchasing power.

3. The Risk-Return Trade-off

The risk-return trade-off states that higher returns come with higher risks. Investors must balance their risk tolerance with expected returns.

3.1 Low-Risk, Low-Return Investments

- Savings accounts, government bonds, fixed deposits.

- Offer stability but may provide lower real returns due to inflation.

3.2 Moderate-Risk, Moderate-Return Investments

- Mutual funds, balanced funds, corporate bonds.

- Provide better returns than fixed deposits but involve some level of risk.

3.3 High-Risk, High-Return Investments

- Stocks, hedge funds, cryptocurrencies, venture capital.

- Can offer substantial gains but also pose significant risks, including market volatility and potential loss of capital.

3.4 How to Manage the Risk-Return Trade-off?

Investors can balance risk and return through:

a) Diversification

- Spreading investments across different asset classes to reduce exposure to any single investment risk.

- Example: A portfolio with 60% stocks, 30% bonds, and 10% real estate is more balanced than an all-equity portfolio.

b) Asset Allocation

- Adjusting the mix of investments based on age, risk appetite, and financial goals.

- Younger investors can take higher risks by allocating more to stocks.

- Older investors should shift towards low-risk fixed-income securities.

c) Systematic Investment Plan (SIP)

- Investing small amounts regularly instead of lump sums to reduce market timing risk.

d) Monitoring & Rebalancing Portfolio

- Periodic reviews ensure that asset allocation remains aligned with financial goals.

Conclusion

Understanding investment risks, expected returns, and the risk-return trade-off is crucial for making smart investment decisions. Key takeaways include:

✔ Risk is inherent in all investments, but it can be managed through diversification and proper asset allocation.

✔ Returns vary based on investment type, market conditions, and risk exposure.

✔ The risk-return trade-off requires investors to find the right balance between high returns and acceptable risk levels.

By implementing risk management strategies and making informed investment choices, investors can optimize returns while minimizing financial uncertainties.

No Comments