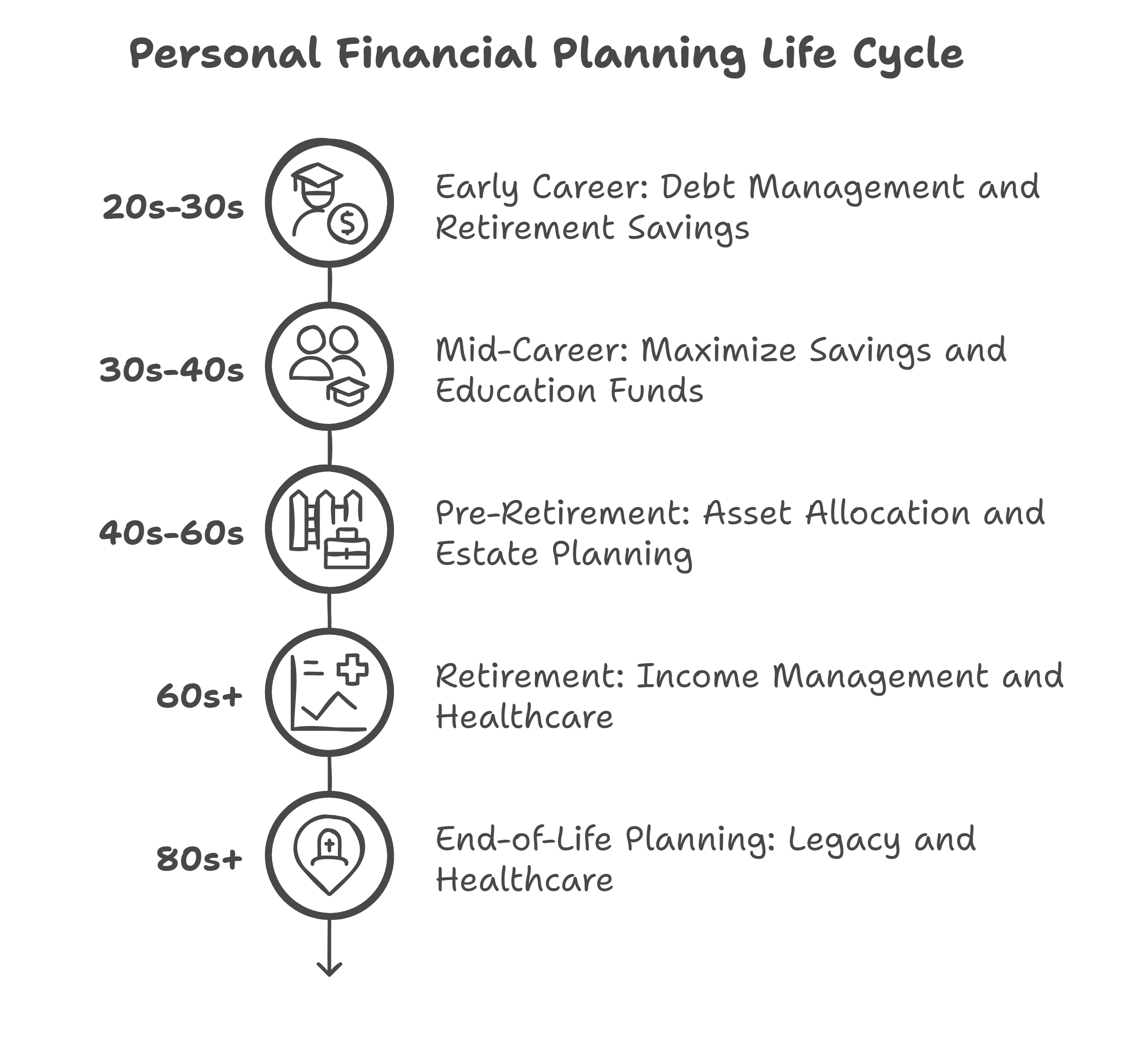

Personal Financial Planning Life Cycle

The Personal Financial Planning Life Cycle describes the various stages individuals typically go through in terms of their financial needs, priorities, and goals as they age. Understanding these stages is crucial for developing effective and relevant financial plans.

Here's a detailed breakdown:

I. Early Career (Accumulation Phase - Stage 1)

- Age: Typically 20s and early 30s

-

Characteristics:

- Starting careers, relatively lower incomes.

- Often burdened with student loan debt or early career debt (car loans, etc.).

- Focus on establishing financial independence.

-

Financial Priorities:

- Debt Management: Prioritize paying off high-interest debt like student loans or credit card balances.

- Budgeting: Develop and stick to a budget to track income and expenses. Learn financial discipline.

- Emergency Fund: Build a small emergency fund (at least 1 month of essential expenses).

- Retirement Savings (Start Early!): Begin contributing to employer-sponsored retirement plans (401k, etc.) to capture matching contributions, even if it's a small amount. The power of compounding starts now!

- Insurance: Get basic health and disability insurance. Consider renters insurance.

-

Financial Goals:

- Pay off debt.

- Establish an emergency fund.

- Start saving for retirement.

- Possibly save for a down payment on a first home (longer-term).

- Investment Strategy: Generally higher risk tolerance. Invest in growth-oriented assets like stocks or stock mutual funds (within appropriate risk tolerance).

II. Mid-Career (Accumulation Phase - Stage 2)

- Age: Typically mid-30s to late 40s

-

Characteristics:

- Income increases, career advancement.

- Financial responsibilities often increase (marriage, children, mortgage).

- Time-crunched, balancing career and family.

-

Financial Priorities:

- Increase Retirement Savings: Maximize contributions to retirement plans (401k, IRA, etc.).

- Save for Education: Begin saving for children's future education expenses (529 plans, etc.).

- Mortgage Management: Optimize mortgage terms (refinance if beneficial).

- Insurance Review: Review and update life, health, and disability insurance coverage to reflect family needs.

- Tax Planning: Implement tax-efficient savings and investment strategies.

-

Financial Goals:

- Maximize retirement savings.

- Save for children's education.

- Pay down mortgage.

- Upgrade home or purchase additional properties (if desired).

- Investment Strategy: Maintain a growth-oriented strategy, but potentially moderate risk slightly as retirement nears. Diversify across a wider range of asset classes.

III. Pre-Retirement (Consolidation Phase)

- Age: Typically late 40s to mid-60s

-

Characteristics:

- Peak earning years, potentially less debt (mortgage nearing payoff, children nearing independence).

- Refocus on retirement readiness.

-

Financial Priorities:

- Maximize Savings (Final Push): Make aggressive efforts to maximize savings and investments for retirement. "Catch-up" contributions to retirement plans (if available) are important.

- Retirement Projections: Develop detailed retirement income projections, including potential Social Security benefits and pension income.

- Asset Allocation Adjustment: Shift asset allocation towards more conservative investments (bonds, etc.) to reduce risk and protect accumulated wealth.

- Debt Minimization: Pay off remaining high-interest debt.

- Long-Term Care Planning: Consider long-term care insurance or other strategies to address potential long-term care expenses.

- Estate Planning: Create or update wills, trusts, and other estate planning documents.

-

Financial Goals:

- Ensure adequate retirement funding.

- Minimize debt.

- Refine estate plan.

- Plan for healthcare costs in retirement.

- Investment Strategy: Lower risk profile, with a higher allocation to bonds and other income-generating assets. Focus on capital preservation and income generation.

IV. Retirement (Distribution Phase)

- Age: Typically mid-60s onwards

-

Characteristics:

- No longer earning a salary; living off savings, investments, and retirement income.

- Focus on maintaining a comfortable lifestyle and managing healthcare expenses.

-

Financial Priorities:

- Income Management: Carefully manage retirement income to cover living expenses, healthcare costs, and other needs.

- Withdrawal Strategy: Develop a sustainable withdrawal strategy from retirement accounts to avoid running out of money.

- Healthcare Coverage: Ensure adequate healthcare coverage (Medicare, supplemental insurance, etc.).

- Tax Management: Optimize tax strategies to minimize tax liabilities on retirement income and distributions.

- Estate Preservation: Continue to manage estate planning documents and update them as needed.

-

Financial Goals:

- Maintain a comfortable lifestyle.

- Cover healthcare expenses.

- Preserve capital.

- Leave a legacy (if desired).

- Investment Strategy: Conservative, income-focused investments. Consider a very small allocation to growth assets to combat inflation. Focus on generating stable cash flow.

V. End-of-Life Planning (Legacy Phase)

- Age: Advanced age (often 80s and beyond)

-

Characteristics:

- Potential for declining health and increased healthcare needs.

- Focus shifts to managing healthcare, ensuring care is available, and leaving a lasting legacy.

-

Financial Priorities:

- Healthcare Management: Optimize healthcare resources and manage costs.

- Long-Term Care: Address long-term care needs and expenses.

- Estate Planning Execution: Ensure estate planning documents are in order and easily accessible. Communicate wishes to family members.

- Legacy Planning: Finalize plans for charitable giving or other legacy goals.

-

Financial Goals:

- Ensure quality of life in later years.

- Cover healthcare and long-term care expenses.

- Transfer assets efficiently to heirs or charities.

- Leave a meaningful legacy.

- Investment Strategy: Very conservative, focused on maintaining liquidity to cover anticipated expenses.

Important Considerations:

- Individual Variations: This life cycle is a general framework. Individuals' experiences may vary significantly based on factors like income, career path, family situation, and lifestyle choices.

- Flexibility: Financial plans should be flexible and adaptable to changing circumstances.

- Professional Advice: Consulting with a qualified financial planner can provide personalized guidance and support throughout the financial planning life cycle.

- Continuous Monitoring: Regularly review and adjust financial plans to ensure they remain aligned with evolving goals and circumstances.

No Comments