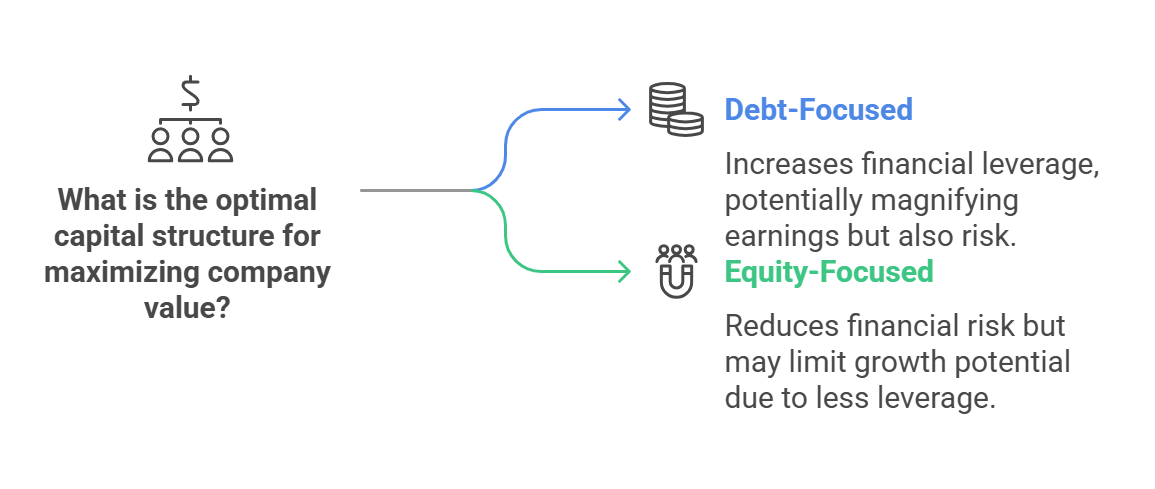

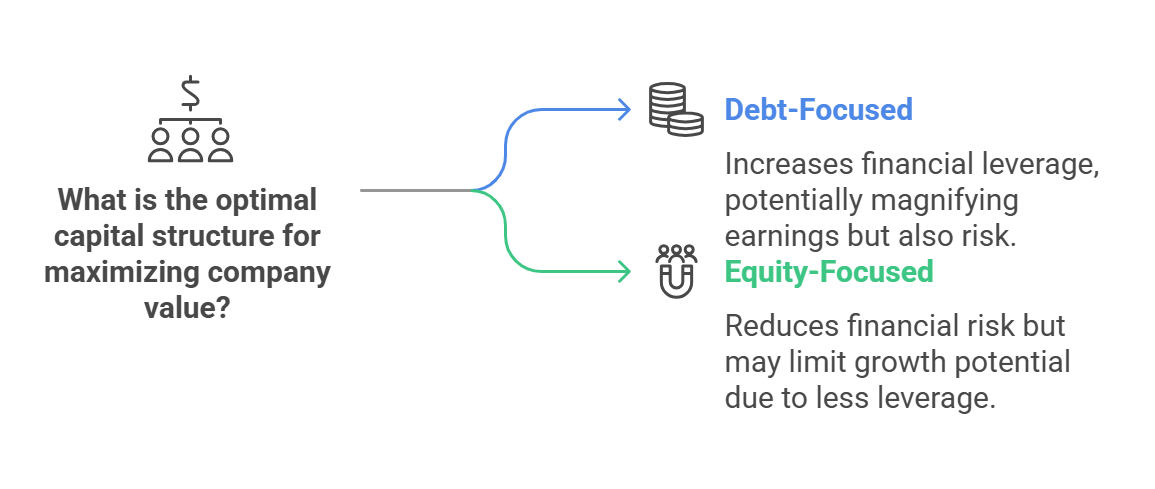

Capital Structure, Theories and Value of the firm

What is Capital Structure?

-

Capital structure refers to how a company finances its assets, specifically the proportions of:

- Debt: Money borrowed (e.g., loans, bonds).

- Equity: Money from owners (e.g., common shares, retained earnings).

- Optimum Capital Structure: The ideal mix of debt and equity that results in the lowest cost of capital and highest value for the company.

Why is Capital Structure Important?

- Leverage Impact: Using debt (financial leverage) can magnify earnings per share (EPS). If a company's profits (EBIT) increase, the increase in EPS will be greater if the company has debt. But also a decrease in EBIT will be magnified.

- Risk: Financial leverage also increases a company's risk of not being able to meet its debt obligations (insolvency), and can make earnings available to shareholders more volatile.

- Value Maximization: A company wants to choose a capital structure that maximizes the value of the shareholders' investments (the stock price).

Key Question: Does Capital Structure Matter?

There are two main opposing views:

- Yes, it matters: This view suggests that a company can influence its overall value by choosing a specific mix of debt and equity. Finding the right balance is important.

- No, it doesn't matter: This view suggests that the specific mix of debt and equity doesn't affect the total value of the company or shareholder wealth. In this view, there is no "optimum" capital structure.

How does Capital Structure Impact Value?

Capital structure can influence a company's value by affecting:

- Earnings Available to Shareholders: Although financing decisions don't influence total earnings (EBIT), they do affect how much of that earning is left for the equity holders.

- Cost of Capital: A company's overall cost of capital (the required return on investment) is impacted by capital structure. The lower cost of capital, the greater the company's value.

1. Capital Structure Theories: Assumptions and Definitions

Assumptions

These are simplifying assumptions used when studying capital structure theories:

- Two Sources of Funds: Companies only use debt and common stock to finance themselves.

- No Corporate Taxes: For simplicity, income taxes are ignored (we will introduce them later).

- 100% Dividend Payout: All earnings are distributed to shareholders, with no retained earnings.

- Constant Total Assets: The company's investment decisions are fixed. This means the overall size or assets of the company are not changing.

- Constant Total Financing: The total amount of funding remains constant, but the company can change the ratio of debt to equity by either issuing more debt and repurchasing shares or vise versa.

- Constant Operating Profits (EBIT): The company's operating profits are not expected to change in the future.

- Homogenous Investor Expectations: All investors share the same expectations about the company's future earnings.

- Constant Business Risk: The company's inherent business risk is assumed to be consistent over time and not influenced by its financing decisions.

- Perpetual Life: The company is assumed to continue operating indefinitely.

Definitions and Symbols

These symbols and equations will be used:

- S = Total market value of equity (value of all outstanding common shares)

- B = Total market value of debt (value of all the company's debt)

- I = Total interest payments on debt

- V = Total market value of the firm (V = S + B)

- NI = Net income available to equity holders (Earnings after interest expense.)

Cost of Capital Equations:

-

Cost of Debt (ki):

kᵢ = I / B(Interest expense / Value of Debt) -

Value of Debt (B):

B = I / kᵢ -

Cost of Equity Capital (ke): (Assuming no growth in dividends or earnings)

kₑ = E₁ / P₀orkₑ = NI / S- Where:

E₁= Earnings per share andP₀= current market price per share

- Where:

-

Value of Equity per share(P0):

P₀ = E₁ / kₑ -

Total Value of Equity (S):

S = NI / kₑorS = (EBIT - I) / kₑ -

Weighted Average Cost of Capital (k0): (The average cost of all a company's financing)

-

k₀ = (B/V)kᵢ + (S/V)kₑ -

k₀ = (I + NI) / V = EBIT / V

-

-

Total Value of the Firm (V):

V = EBIT / k₀ -

Alternatively:

V = (EBIT - I) / kₑ + I / kᵢ -

Relationship of ke and k0:

-

kₑ = k₀ + (k₀ – kᵢ) * B / S

-

Key Takeaways

- Financial Leverage Matters: Changes in capital structure (debt/equity mix) affect a company's risk, cost of capital, and ultimately its value.

- Optimum Goal: Companies strive to find the perfect balance of debt and equity that minimizes their overall cost of capital and maximizes their market value (shareholder wealth).

-

Cost of Capital is Crucial: Understanding the cost of debt, cost of equity, and weighted average cost of capital (k0) is essential for evaluating capital structure decisions.

No Comments