Cost of Capital: Meaning and concept

1. Introduction

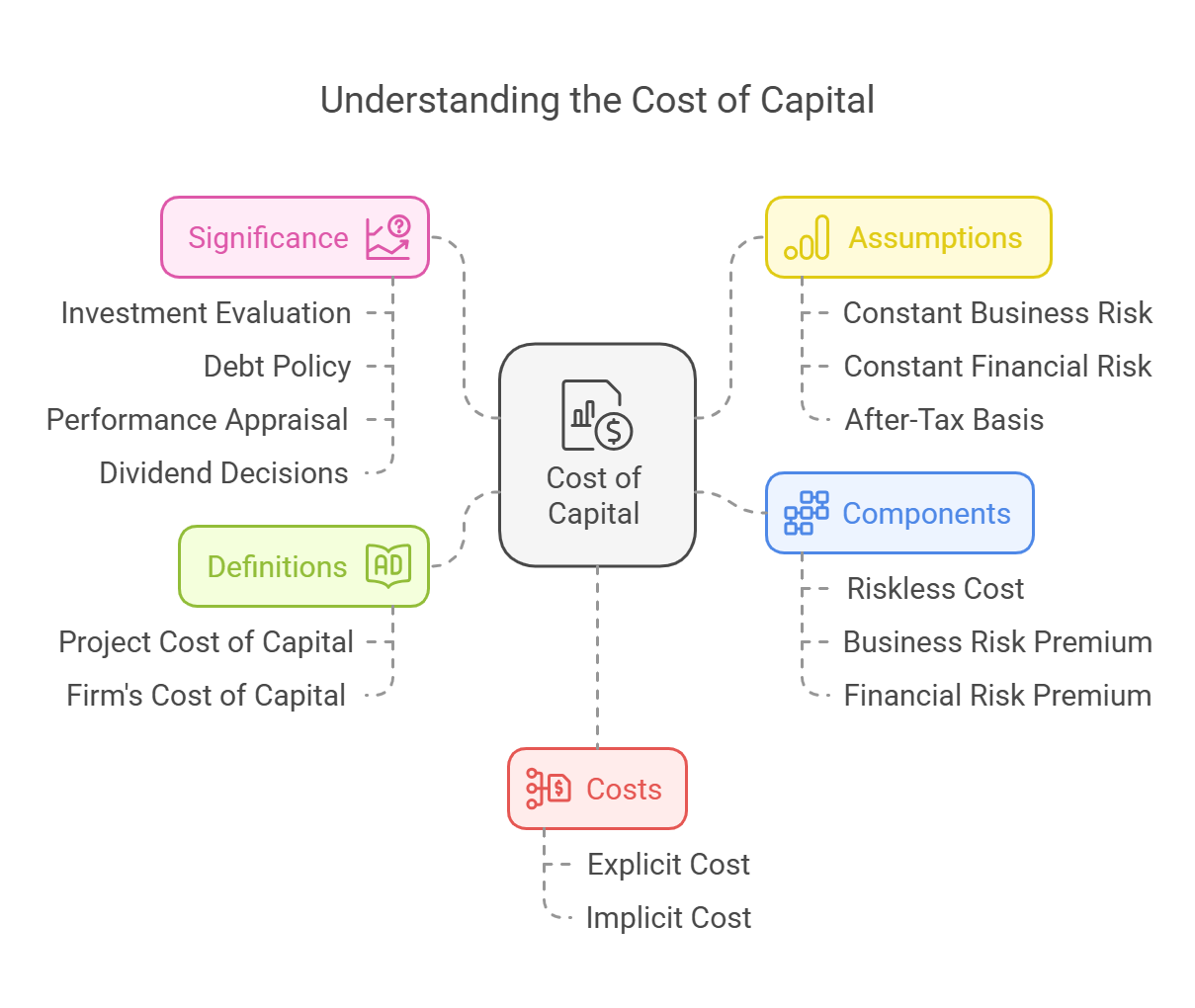

The cost of capital is a crucial concept in financial management, serving as a benchmark for investment decisions and a factor in determining a firm's financial policy. It is the minimum rate of return that a company must earn on its investments to maintain its market value and attract funds.

2. Meaning and Significance of Cost of Capital

2.1. Definition

- Project Cost of Capital: The discount rate used to discount a project's cash flows. It is the minimum required rate of return based on the riskiness of the project.

- Firm's Cost of Capital: The overall, or average, required rate of return on all of the company’s investment projects. It should only be used for projects with a risk profile similar to the average risk profile of the company.

- Risk Adjustment: The cost of capital for individual projects is usually adjusted by adding a risk premium or discount to the firm's cost of capital. This premium is based on whether the project's risk profile is higher or lower than the company's risk profile.

2.2. Importance of Cost of Capital

The cost of capital is important as a standard for:

-

Investment Evaluation:

- NPV Method: It is used as the discount rate to calculate Net Present Value (NPV).

- IRR Method: It acts as the minimum hurdle rate or required return that should be achieved on investment, and is compared to the Internal Rate of Return (IRR) of an investment project.

- Designing Debt Policy: Firms aim to maximize firm value by minimizing overall cost of capital, often using debt financing to reduce taxes as interest on debt is tax-deductible.

- Performance Appraisal: It is used as a benchmark to evaluate top management’s financial decisions by comparing actual profitability to the overall cost of capital.

- Dividend Decisions: It is also used when making dividend decisions and investments in current assets.

3. Practical Utility of Cost of Capital

- Accept-Reject Criterion: A firm accepts projects with a return higher than the cost of capital, enhancing shareholder wealth, and rejects projects with lower returns which erodes shareholder wealth.

- Optimum Investment Decisions: The cost of capital helps in making optimum investment decisions.

4. Definition of Cost of Capital

- Minimum Required Return: It's the discount rate that determines if a project is worth undertaking and the minimum rate a firm must earn to maintain its market value.

- Multiple components: It consists of several elements that represent the cost of each capital component (source of funds) such as debt, equity, preference shares, etc.

- Specific Cost of Capital: The cost of each individual source of funds (e.g., cost of debt, cost of equity).

- Weighted Cost of Capital: The combined cost of all capital sources, also called overall cost of capital, composite cost of capital, or combined cost of capital.

5. Assumptions Underlying Cost of Capital Theory

-

Constant Business Risk: Acceptance of a new project won't change the firm's business risk (variability in operating profits due to sales fluctuations).

- If a company accepts a project that has significantly higher risks than the average risk of the business, the cost of funds may increase, since the creditors would want higher compensation for the extra risks.

-

Constant Financial Risk: The firm's financial risk remains unaffected by financing decisions. This means that the proportion of debt and equity in the capital structure remains constant.

- As debt increases in the capital structure, financial risk increases, and investors would react by demanding a higher rate of return on investment to compensate for the higher risk.

-

After-Tax Basis: Benefits are evaluated on an after-tax basis. Only the cost of debt requires tax adjustment as interest is a tax-deductible expense, whereas dividends are not.

6. Components of the Cost of Capital

The cost of capital can be broken down into three key components:

- rj: The riskless cost of the particular type of financing.

- b: The business risk premium.

- f: The financial risk premium.

Therefore, the cost of capital is represented as: k = rj + b + f

Since the analysis assumes business and financial risks are constant, changes in cost of each type of capital are only due to changes in the supply of and demand for each type of funds.

7. Explicit and Implicit Costs

7.1. Explicit Cost

- Definition: The discount rate that equates the present value of the cash inflows (proceeds from financing) with the present value of cash outflows (payments to providers of funds).

- Cash Flows: A series of cash flows occur when funds are raised from different sources, with an initial inflow and subsequent outflows for interest, principal repayment, or dividends.

- Calculation: The calculation of explicit cost is similar to calculation of IRR but with initial inflow and subsequent outflows.

7.2. Implicit Cost (Opportunity Cost)

- Definition: The rate of return associated with the best investment opportunity foregone by the firm and its shareholders if the project under consideration is accepted. It is technically referred to as the opportunity cost of capital.

- Example: The cost of retained earnings, as they represent undistributed profits belonging to the shareholders.

7.3. Distinguishing Explicit and Implicit Costs

- Explicit costs arise when funds are raised.

- Implicit costs arise when funds are used.

8. Conclusion

The cost of capital is a fundamental concept in financial management, serving as a vital benchmark for investment decisions and financial policies. It is important to understand the different ways to assess the cost of capital, which includes explicit and implicit costs, as well as the assumptions that are inherent within the theory. By understanding the cost of capital, a company can allocate funds efficiently to maximize value for its stakeholders.

No Comments