Net Operating Income approach

The Net Operating Income (NOI) Approach, also suggested by Durand, presents a contrasting view to the NI Approach. It argues that a company's capital structure is irrelevant to its overall value. In simpler terms, changing the amount of debt a company uses will not affect its total value, share price, or overall cost of capital.

Key Ideas of the NOI Approach

- Capital Structure Irrelevance: A company's value is independent of its financing mix (debt vs. equity).

- Constant Overall Cost of Capital (k0): The company's overall cost of capital remains the same regardless of how much debt it uses.

- Value Determined by EBIT: The market values a company as a whole based on its earnings before interest and taxes (EBIT). How that capital is split between debt and equity is not significant.

- Equity Value as a Residual: The market value of equity is simply what remains after deducting the value of debt from the total value of the company (S = V - B).

- Rising Cost of Equity (ke): As a company takes on more debt, the cost of equity rises to compensate shareholders for the increased financial risk. This rise perfectly offsets any benefits from cheaper debt.

- No Optimum Capital Structure: Any mix of debt and equity is equally optimal according to this approach.

Propositions of the NOI Approach

Here are the core ideas behind the NOI approach:

-

Constant Overall Capitalization Rate (k0):

- The overall cost of capital for the firm (

k₀) remains constant, no matter the degree of leverage. The total value of the firm (V) is determined by dividing the EBIT byk₀. -

V = EBIT / k₀ - The market values the total company, not the individual components of debt or equity.

- The overall cost of capital for the firm (

-

Residual Value of Equity:

- The value of equity (S) is what's left after subtracting the total value of debt (B) from the total value of the company (V).

-

S = V - B

-

Changes in Cost of Equity Capital (ke):

- The cost of equity increases as the company uses more debt.

- Shareholders demand a higher return to compensate for increased financial risk from leverage. The increase in

kₑis calculated as: -

kₑ = k₀ + (k₀ - kᵢ) * (B / S)

-

Cost of Debt (ki):

-

Explicit Cost: The actual rate of interest on the debt. The company can borrow at a fixed rate, regardless of leverage.

-

Implicit or Hidden Cost: The increase in the cost of equity caused by increased leverage. This offsets the advantage of cheaper debt.

-

Essentially, the increased cost of equity from taking on more debt completely cancels out the benefits of cheaper debt. The real cost of debt and equity, according to this approach, is equal to

k₀.

-

Implications of the NOI Approach

- No Impact on Value: Changes in debt don't change the total company value.

- No Impact on Share Price: The market price of shares remains constant regardless of the debt-to-equity ratio.

- No Optimum Structure: There is no magic combination of debt and equity; any capital structure is considered optimal.

Example: Impact of Leverage on Company Value (NOI Approach)

Let's revisit the example numbers:

Initial Situation

- EBIT: Rs 50,000

- Cost of Debt (ki): 10%

- Outstanding Debt: Rs 200,000

- Overall Cost of Capital (k0): 12.5%

| Item | Amount |

|---|---|

| Net Operating Income (EBIT) | Rs 50,000 |

| Overall Capitalization Rate (k0) | 0.125 |

| Total Market Value of Firm (V) = EBIT/k0 | Rs 400,000 |

| Total Value of Debt (B) | Rs 200,000 |

| Total Market Value of Equity (S) = V - B | Rs 200,000 |

| Equity Capitalization Rate (ke) | 15% |

Calculation of kₑ = (EBIT - I)/ S

= (50,000 - 20,000) / 200,000

= 0.15 or 15%`

Alternative Calculation using formula

kₑ = k₀ + (k₀ - kᵢ)(B/S)

= 0.125 + (0.125 -0.10) * (200,000 / 200,000)

= 0.15` or 15%

Verification of WACC

`k₀ = kᵢ(B/V) + kₑ(S/V)

= 0.10*(200,000/400,000)+0.15*(200,000/400,000)

= 0.125 or 12.5%`

Increase in Debt

The company increases debt to Rs 300,000 and buys back shares.

- Debt (B): Now Rs 300,000

- k0: Remains 12.5%

| Item | Amount |

|---|---|

| Net Operating Income (EBIT) | Rs 50,000 |

| Overall Capitalization Rate (k0) | 0.125 |

| Total Market Value of Firm (V) = EBIT/k0 | Rs 400,000 |

| Total Value of Debt (B) | Rs 300,000 |

| Total Market Value of Equity (S) = V - B | Rs 100,000 |

| Equity Capitalization Rate (ke) | 20% |

Calculation of `kₑ = (EBIT - I)/ S

= (50,000 - 30,000) / 100,000

= 0.20 or 20%

Alternative Calculation using formula

kₑ = k₀ + (k₀ - kᵢ)(B/S)

= 0.125 + (0.125 -0.10) * (300,000 / 100,000)

= 0.20 or 20%

Verification of WACC

k₀ = kᵢ(B/V) + kₑ(S/V)

= 0.10*(300,000/400,000)+0.20*(100,000/400,000)

= 0.125 or 12.5%`

Decrease in Debt

The company reduces debt to Rs 100,000 by issuing new shares.

- Debt (B): Now Rs 100,000

- k0: Remains 12.5%

| Item | Amount |

|---|---|

| Net Operating Income (EBIT) | Rs 50,000 |

| Overall Capitalization Rate (k0) | 0.125 |

| Total Market Value of Firm (V) = EBIT/k0 | Rs 400,000 |

| Total Value of Debt (B) | Rs 100,000 |

| Total Market Value of Equity (S) = V - B | Rs 300,000 |

| Equity Capitalization Rate (ke) | 13.33% |

Calculation of kₑ = (EBIT - I)/ S

= (50,000 - 10,000) / 300,000

= 0.1333 or 13.33%

Alternative Calculation using formula

kₑ = k₀ + (k₀ - kᵢ)(B/S)

= 0.125 + (0.125 -0.10) * (100,000 / 300,000)

= 0.1333` or 13.33%

Verification of WACC

k₀ = kᵢ(B/V) + kₑ(S/V)

= 0.10*(100,000/400,000)+0.1333*(300,000/400,000)

= 0.125 or 12.5%

Impact on Share Price

- The market price of shares will remain the same, no matter the change in leverage (using the same approach as before where the market value of equity is divided by the number of shares outstanding).

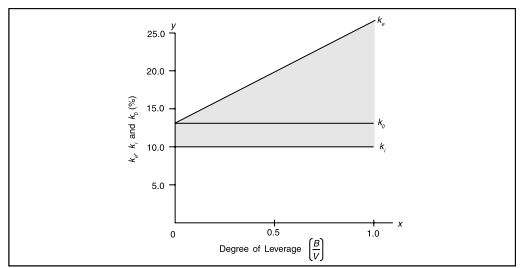

Graphical Representation

-

X-axis: Degree of leverage (B/V)

-

Y-axis: Cost of capital percentages (ki, ke, k0)

-

k₀andkᵢare horizontal lines, as they remain constant with changes in leverage. -

kₑis an upward-sloping line, continuously increasing as leverage rises.

Conclusion of the NOI Approach

The NOI Approach suggests that a company's capital structure is irrelevant to its value. Any change in leverage will be offset by a corresponding change in the cost of equity, thus keeping the total value of the firm constant. There is, therefore, no optimal capital structure.

In contrast to the NI Approach (where increased leverage is beneficial), the NOI approach states that leverage does not create or destroy value.

No Comments