Time Value of Money- Present value and Future Value

1. Introduction

The time value of money (TVM) is a core concept in finance. It essentially means that the value of a sum of money is different at different points in time. Specifically, money received today is worth more than the same amount received in the future. This principle is grounded in the idea that money has the potential to earn more money when invested.

2. Key Principles

- Present Value Higher: A sum of money received today is more valuable than the same amount received in the future.

- Future Value Lower: Conversely, a sum of money received in the future is less valuable than the same amount today.

- Rational Preference: Because of this, rational investors prefer current receipts to future receipts.

- Time Preference for Money: The time value of money can also be referred to as time preference for money, reflecting the preference for earlier receipt.

3. Why Time Value of Money Exists

- Reinvestment Opportunities: The main reason for time preference is the availability of reinvestment opportunities for funds received earlier.

- Earning Returns: Money received earlier can be invested to earn a rate of return. Funds received later will not have the same opportunity to grow.

- Discount Rate: The time preference for money is often expressed as a rate of return or a discount rate.

4. Illustration

Let's consider a simple example:

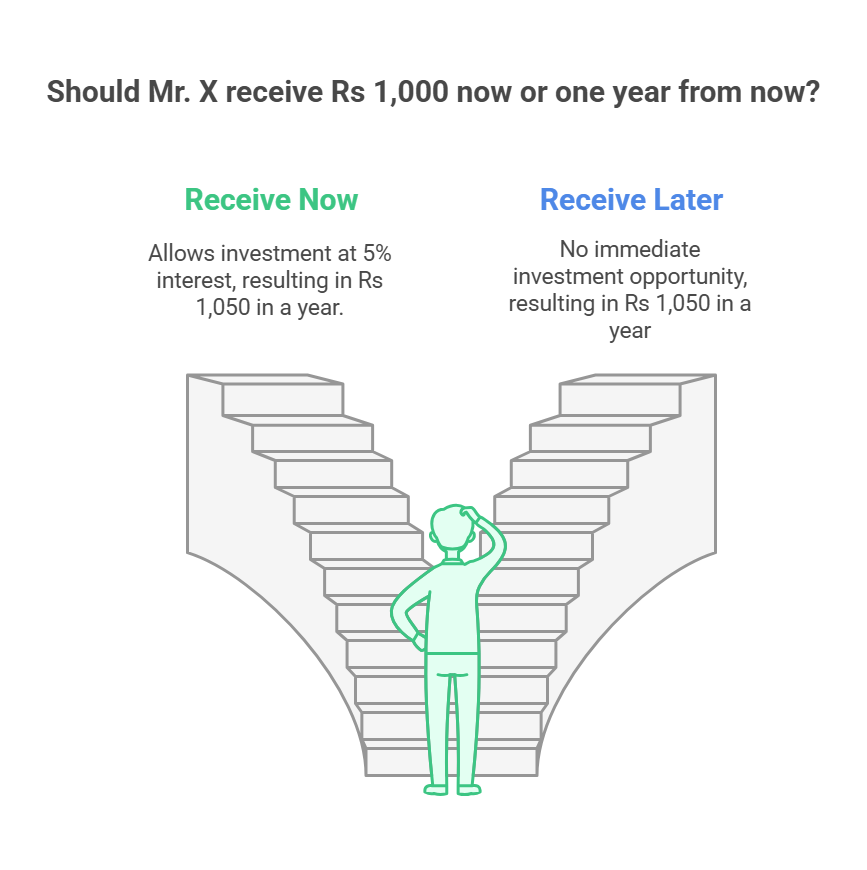

- Scenario: Mr. X can choose to receive Rs 1,000 now or one year from now.

-

Preference: He will choose to receive the money now. If he invests it in a savings account earning 5% interest, he will have Rs 1,050 by the end of the year, so receiving Rs 1,000 today is the same as receiving Rs 1,050 in a year.

- Conclusion: Future cash flows are less valuable due to the investment opportunities associated with present cash flows.

5. Importance for Business

- Decisions with Future Ramifications: Businesses make decisions (such as capital budgeting) that have financial implications extending into the future.

-

Capital Budgeting: Decisions involving current cash outflows (investment in a machine or project) and future cash inflows (revenue generated by the machine/project)

- Example: if a project costs Rs 10,00,000 today, but only has an estimated inflow of Rs 10,80,000 in 1 year, and the interest rate is 10%, the project is not acceptable, because the investment could have made Rs 11,00,000 in one year without the project.

- Loan Management: When raising funds from lenders or issuing debentures, a company must consider the time value of money when making interest payments and repaying loans.

6. Converting Cash Flows Across Time

To make meaningful comparisons between cash flows in different time periods, it's necessary to convert them to a common point in time using two main techniques:

-

Compounding:

- Purpose: To calculate the future value of a present sum of money.

- Definition: Calculating the future value of an investment by adding the interest earned back into the principal so that it also earns interest, or interest on interest.

- Application: Taking present value to calculate future value

-

Discounting:

- Purpose: To calculate the present value of a future sum of money.

- Definition: Determining the present value of a future amount or cash flow, based on a discount rate.

- Application: Taking future value and bringing it back to present value

7. Compounding: Calculating Future Value

- Definition: The process of determining the future value of an investment by accumulating interest, including interest on previously earned interest.

- Formula: In its simplest form, the formula can be represented as: FV = PV (1 + r)^n

Where:

-

PV is the present value

-

FV is the future value

-

r is the rate of interest or discount rate

-

n is the number of periods

-

Example: Suppose you will receive $110.25 in two years, what is the present value if the rate of interest is 5%

PV = 110.25 / (1+0.05)^2 = 100

8. Discounting: Calculating Present Value

Definition

Discounting is the process of determining the present value (PV) of a future amount by applying a discount rate. This process accounts for the time value of money, which recognizes that money available today is worth more than the same amount in the future due to its potential earning capacity.

Formula

The basic formula for discounting can be represented as:

PV = FV / (1 + r)^n

Where:

- PV = Present Value

- FV = Future Value

- r = Rate of Interest or Discount Rate

- n = Number of Periods

Explanation of Terms

- Present Value (PV): The current worth of a future sum of money. It's the amount you would need to invest today at a specific rate of return to reach a future target amount.

- Future Value (FV): The value of an asset or sum of money at a specified future date, assuming a certain rate of return.

- Rate of Interest or Discount Rate (r): The rate used to discount the future value back to its present value. It represents the opportunity cost of capital or the required rate of return.

- Number of Periods (n): The number of time periods (usually years) between the present and the future.

Example

Suppose you are scheduled to receive $110.25 in two years. If the rate of interest (or discount rate) is 5%, what is the present value of this future amount?

Applying the formula:

PV = 110.25 / (1 + 0.05)^2

PV = 110.25 / (1.05)^2

PV = 110.25 / 1.1025

PV = 100

Therefore, the present value of receiving $110.25 in two years, discounted at a 5% interest rate, is $100.

9. Conclusion

The concept of the time value of money is fundamental to financial decision-making. It emphasizes that a sum of money's value is directly tied to the timing of its receipt or disbursement. By using the techniques of compounding and discounting, we can effectively compare cash flows across different periods, making informed financial decisions regarding investments, loans, and other financial transactions. This concept is essential for all business, investors, and those managing personal finances.

No Comments