Modigliani-Miller (MM) Approach

The Modigliani-Miller (MM) approach provides a fundamental framework for understanding how capital structure impacts firm value. It challenges conventional wisdom and offers insights into the trade-offs involved in financing decisions. It provides 3 propositions to explain the effect of capital structure on firm value.

Core Concepts of the MM Approach

- Perfect Market Assumption: The MM approach initially assumes a perfect market with no taxes, transaction costs, or information asymmetry. In this idealized world, capital structure is irrelevant.

- Arbitrage Argument: The core justification for capital structure irrelevance is the arbitrage process. Investors can replicate the effects of corporate leverage by borrowing or lending on their own accounts ("homemade leverage").

- Impact of Taxes: When corporate taxes are introduced, the MM approach recognizes that debt becomes advantageous due to the tax shield on interest payments. This leads to a higher firm value with more debt.

- Limitations in the Real World: The initial MM assumptions don't hold true in reality. Imperfections like taxes, bankruptcy costs, and information asymmetry affect the relationship between capital structure and firm value.

Basic Propositions of the MM Approach

The MM approach has three main propositions:

-

Proposition I (No Taxes): Capital structure is irrelevant.

- The overall cost of capital (k0) and the value of the firm (V) are independent of the capital structure. The total value is determined by capitalizing expected operating earnings at a rate appropriate for its risk class.

-

Proposition II (No Taxes): Cost of Equity Increases with Leverage

- The cost of equity (ke) is equal to the capitalization rate of a pure equity stream plus a premium for financial risk.

- ke = k0 + (k0 - ki) * (B/S)

- In essence, the cost of equity increases to exactly offset the benefit of cheaper debt, keeping the overall cost of capital constant.

- Investment Decisions: Investment decisions are completely separate from financing decisions.

Assumptions Underlying MM Propositions (Without Taxes)

These assumptions are crucial for the irrelevance propositions to hold:

-

Perfect Capital Markets:

- Securities are infinitely divisible.

- Investors can freely buy/sell securities.

- Investors can borrow on the same terms as firms.

- No transaction costs.

- Perfect information: all investors have the same information.

- Investors are rational.

- Equal Expectations: All investors have the same expectations about a firm's net operating income.

- Equivalent Risk Class: Firms can be categorized into "equivalent risk classes" with similar operating environments.

- 100% Dividend Payout: All earnings are paid out as dividends.

- No Taxes: This is the most critical assumption for the initial propositions.

The Arbitrage Process: Justification for Irrelevance (Proposition 1)

The MM hypothesis hinges on the arbitrage process. This is the mechanism that ensures that two identical firms, except for their capital structure, will have the same total value. The key is that arbitrageurs can take advantage of pricing differences by using personal leverage ("homemade leverage").

How Arbitrage Works: Example

Let's say there are two identical firms:

- Firm L: Levered (has debt)

- Firm U: Unlevered (no debt)

If Firm L is trading at a higher total value than Firm U, arbitrageurs will:

This arbitrage activity will:

- Decrease the demand for Firm L's shares, causing its price to fall.

- Increase the demand for Firm U's shares, causing its price to rise.

This process continues until the total values of Firm L and Firm U are equal.

Reverse Arbitrage

The arbitrage process also works in reverse. If the unlevered firm (Firm U) is overvalued compared to the levered firm (Firm L), investors would sell their shares in Firm U and use the proceeds to buy a proportional share in the levered firm (debt and equity). This will also lead to convergence of the total value of both firms

Limitations of the Arbitrage Process

The arbitrage process is not realistic and the exercise based upon it is purely theoretical and has no practical relevance. Several factors can hinder the arbitrage process, undermining the perfect substitutability of personal leverage for corporate leverage:

- Risk Perception: Individual investors may perceive personal leverage as riskier than corporate leverage due to unlimited liability.

- Convenience: Corporate borrowing is more convenient for investors than arranging personal loans.

- Cost of Borrowing: Individual investors typically face higher borrowing costs than corporations.

- Institutional Restrictions: Some institutional investors are restricted from engaging in personal leverage.

- Transaction Costs: Brokerage fees and other costs reduce the arbitrageur's potential profit.

Because of these imperfections, the arbitrage process is not fully effective, and the MM proposition of capital structure irrelevance may not hold in the real world.

Incorporating Corporate Taxes (MM with Taxes)

MM recognized that the introduction of corporate taxes changes the game. Since interest payments are tax-deductible, debt creates a "tax shield" that lowers a company's tax burden.

Proposition I (With Taxes): Debt Increases Firm Value

The value of a levered firm (VL) is equal to the value of an unlevered firm (VU) plus the present value of the tax shield:

VL = VU + Bt Where:

- B = Amount of Debt

- t = Corporate Tax Rate

This implies that a firm's value is maximized when its capital structure contains only debt.

Limitations to MM with Taxes:

- Bankruptcy Costs: Firms can incur heavy dismantling and removal costs when selling assets.

- Indirect Bankruptcy Costs: Valuable employees leave, suppliers do not grant credit, customers seek more reliable suppliers and lenders demand higher interest rates

- Agency Costs: Agency costs rise when debt is excessive.

Trade-off Theory

The trade-off theory recognizes that companies face a trade-off between the benefits of debt financing (interest tax shields) and the costs of financial distress (including bankruptcy costs). Firms will choose a capital structure that balances these two factors.

Signalling Theory

The management has superior information regarding business prospects as compared to the investors, which is called asymmetric information. In view of the management having asymmetric information, shareholders often interpret the announcement of a share issue as a negative signal that the firm’s prospects (as perceived by the management) are not bright and as a result share prices decline

Pecking Order Theory

In contrast to the Trade off theory, according to the pecking order theory , firms prefer internal financing, then debt, and then equity

Impact of Bankruptcy Costs on WACC

Direct Bankruptcy Costs

These are the legal and administrative costs associated with the bankruptcy proceedings of the firm

Indirect Bankruptcy Costs

These are the costs of avoiding a bankruptcy filing by a financially distressed firm

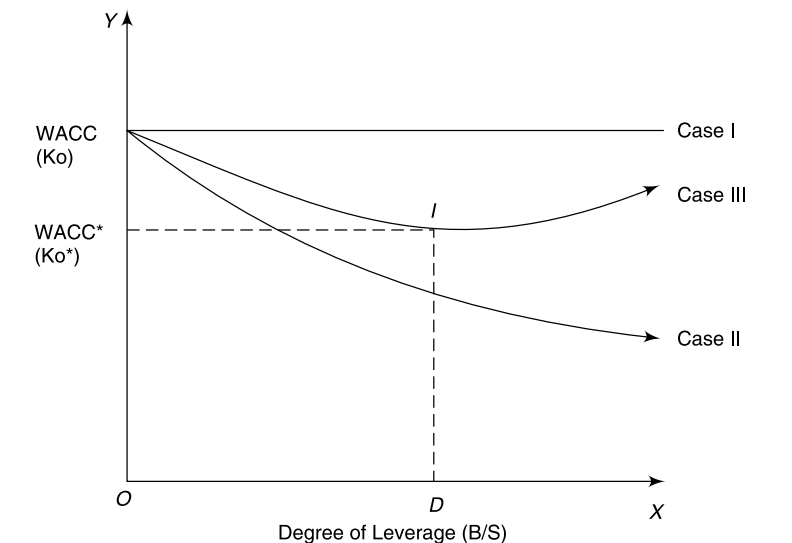

Three Scenarios to determine Firm's WACC

Case I (no taxes) : The overall cost of capital remains constant

Case II (Corporate Taxes) : Firms maximize the value by continuously increasing debt

Case III (Corporate Taxes and Bankruptcy costs ) The trade off theory advocates for an optimal capital structure at which the overall cost of capital is minimum

Key Takeaways

- MM Provides a Baseline: The MM approach provides a theoretical starting point for understanding capital structure decisions.

- Perfect Markets are Unrealistic: The perfect market assumptions are a simplification.

- Taxes Matter: Corporate taxes create an incentive to use debt.

- Real-World Factors are Crucial: Bankruptcy costs, agency costs, and information asymmetry significantly affect capital structure decisions.

- Trade-Off is Key: The trade-off between tax benefits and distress costs is a fundamental concept in capital structure theory.

This explanation of the Modigliani-Miller (MM) approach, along with its extensions, should give you a solid foundation for understanding capital structure theory.

No Comments