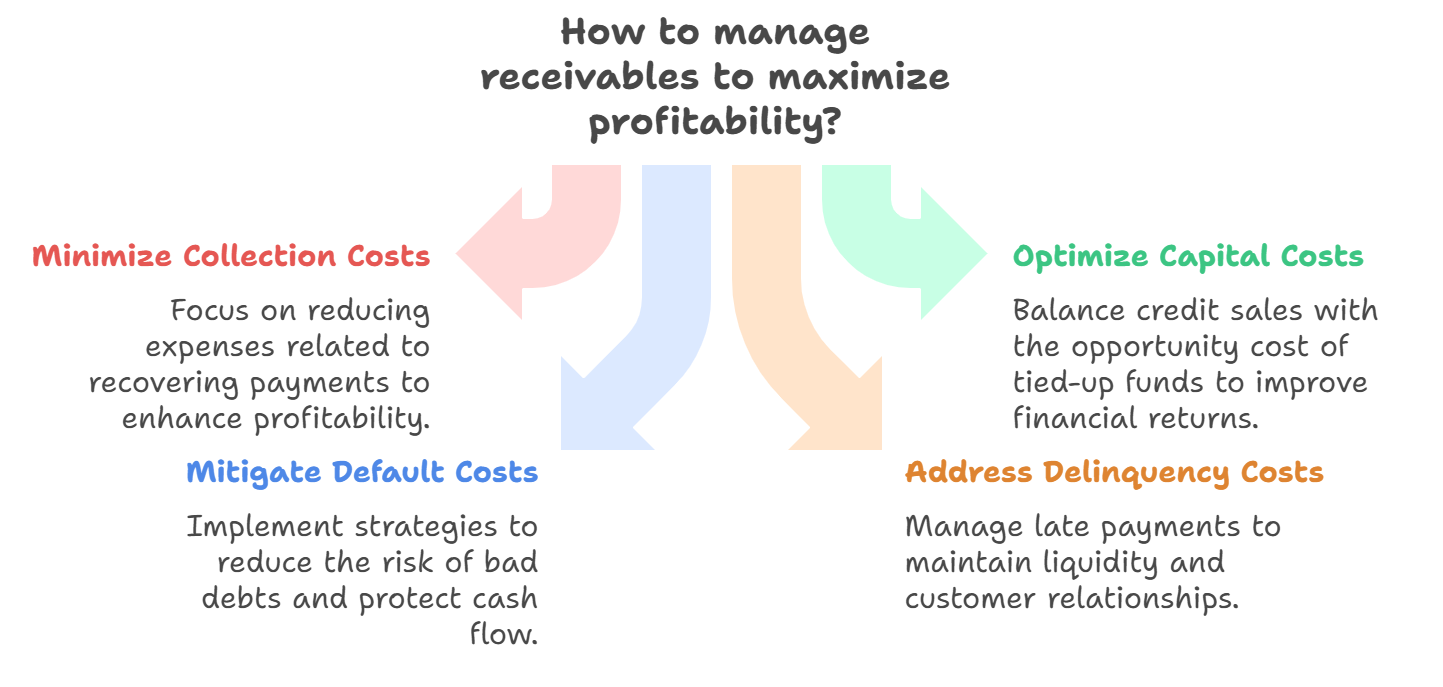

Costs Associated with Receivables Management

Efficient receivables management isn't just about maximizing collections; it's also about minimizing the costs associated with extending credit and maintaining accounts receivable. Balancing these costs is crucial for maximizing overall profitability.

Core Idea: Balancing Sales and Cost

The key to successful receivables management is striking a balance between:

- Generating sales through credit

- Minimizing the costs associated with managing that credit.

1. Collection Cost

- Definition: Expenses incurred in recovering outstanding payments from customers.

-

Examples:

- Salaries of collection staff (employees responsible for follow-ups)

- Cost of sending reminders (emails, letters, phone calls)

- Legal expenses (if legal action is required for overdue accounts)

- Third-party collection agency fees (if external agencies are hired)

- Impact: Higher collection costs can reduce profitability.

2. Capital Cost

- Definition: The opportunity cost of funds tied up in receivables. It's the return a company could have earned if the money wasn't locked in accounts receivable.

-

Explanation:

- When a company sells on credit, it doesn't receive cash immediately. This delay means the company loses the opportunity to invest those funds elsewhere.

- The capital cost represents the lost earnings from not being able to use those funds.

-

Formula:

Example: If a company has $100,000 in receivables and its cost of capital is 12% per annum:Capital Cost = Receivables * Cost of CapitalCapital Cost = $100,000 * 0.12 = $12,000 -

Impact:

- A higher credit period (longer time for customers to pay) increases the capital cost.

- Companies must balance the potential for increased sales through credit with the cost of tying up capital.

3. Default Cost (Bad Debt Cost)

- Definition: The loss incurred when customers fail to pay their dues (bad debts).

-

Causes:

- Customers go bankrupt or refuse to pay.

- Poor credit assessment leads to extending credit to high-risk customers.

- A weak collection policy fails to recover overdue payments.

-

Impact:

- Direct loss in cash flow and profitability.

- Increased risk and uncertainty in financial planning.

-

Mitigation:

- Perform thorough creditworthiness checks before granting credit.

- Set strict credit policies to reduce extending credit to high-risk customers.

- Maintain a proactive collection policy.

4. Delinquency Cost

- Definition: Costs incurred when payments are not received on time, even if customers eventually pay after a delay.

-

Components:

- Interest on late payments (opportunity cost of delayed funds)

- Administrative costs (sending reminders, tracking late payments)

- Loss of goodwill (strained customer relationships due to delayed payments)

- Example: A payment of $50,000 is due in 30 days but received after 60 days, the company incurs interest losses and additional tracking costs.

-

Impact:

- Reduces liquidity, affecting day-to-day operations.

- May lead to financial distress if large payments are significantly delayed.

-

Mitigation:

- Implement late payment penalties.

- Encourage early payments with cash discounts.

Conclusion

Managing receivables effectively requires a careful balancing act: boosting credit sales while minimizing costs. Companies must actively work to minimize collection, capital, default, and delinquency costs to ensure financial stability and profitability.

No Comments