Strategic Investment Decisions and Cost of Capital

1. Introduction

Capital budgeting, also known as investment appraisal, is a crucial process that organizations use to evaluate long-term investments. These investments may include purchasing new machinery, replacing old equipment, building new plants, developing new products, and undertaking research and development projects. The aim is to determine if these investments are worth the funding they require and if they will contribute to maximizing shareholder wealth.

2. Capital Budgeting

2.1. Definition

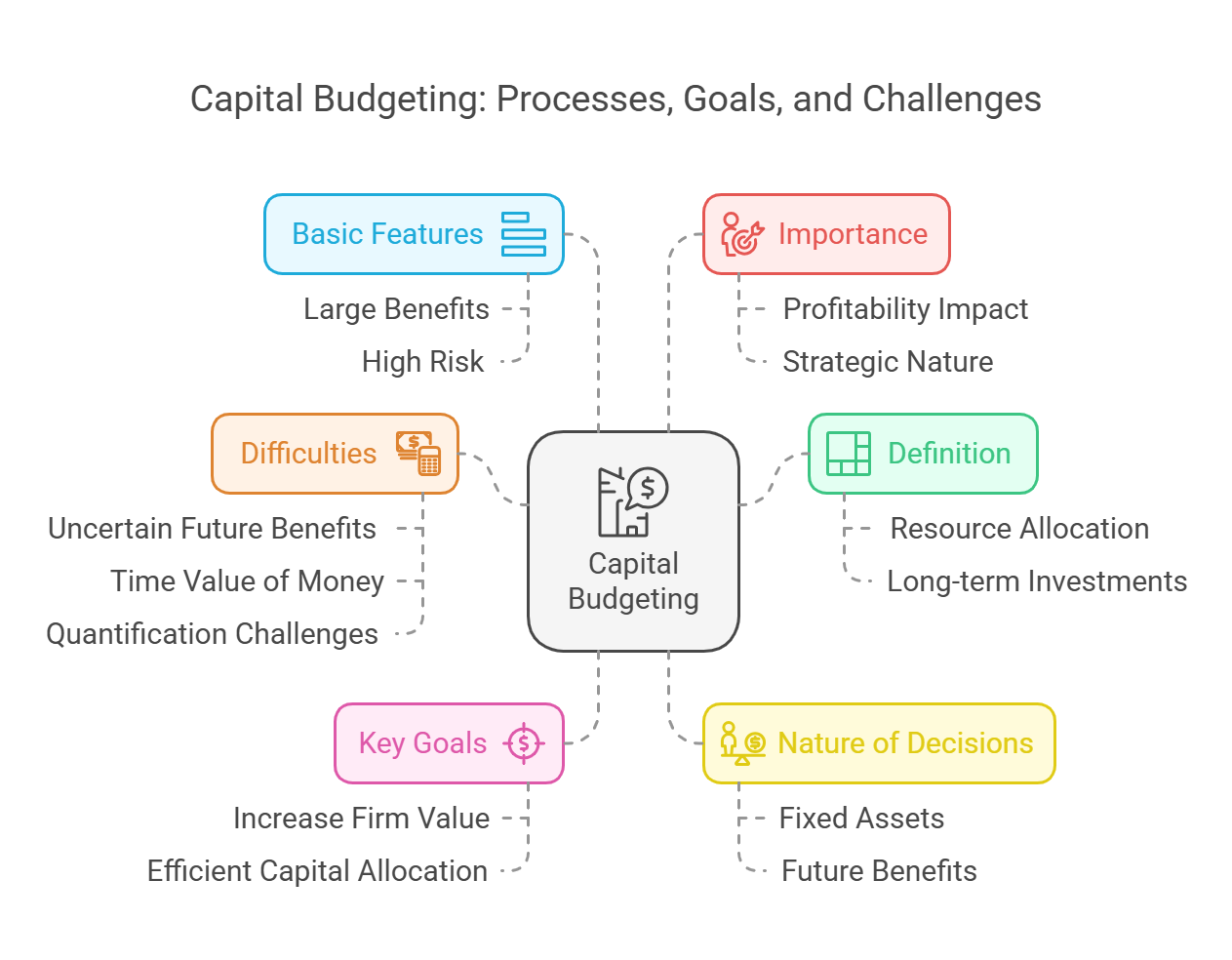

Capital budgeting is the process of allocating resources for major capital or investment expenditures. It involves evaluating and selecting long-term investments that are consistent with the goal of maximizing shareholders’ (owners’) wealth.

2.2. Key Goals

- Increase Firm Value: The primary objective of capital budgeting investments is to increase the value of the firm to the shareholders.

- Efficient Capital Allocation: It ensures the efficient commitment of a firm's funds to long-term assets.

2.3. Nature of Capital Budgeting Decisions

Capital budgeting decisions involve fixed or long-term assets that:

- Yield a return over a period exceeding one year.

- Require a current outlay of cash resources.

- Result in an anticipated flow of future benefits in the form of increased revenues or reduced costs.

- Include addition, disposition, modification, and replacement of fixed assets.

2.4. Basic Features

Capital budgeting is characterized by:

- Large Anticipated Benefits: Investments have potentially large benefits.

- High Degree of Risk: A relatively high degree of risk is involved.

- Long Time Period: A long time period exists between the initial outlay and the anticipated returns.

2.5. Importance of Capital Budgeting Decisions

Capital budgeting decisions are vital for a firm because:

- Impact on Profitability: Such decisions affect the profitability of a firm and its ability to generate revenue.

- Influence on Competitive Position: They have a bearing on a firm's competitive position in the market.

- Long-Term Consequences: These investments commit a company to a specific future cost structure.

- Strategic Nature: Unlike smaller tactical decisions, capital investment decisions have significant strategic impact, leading to changes in profits, risks, and stakeholder perceptions.

- Irreversibility: They are not easily reversible without significant financial loss, as resale markets may be limited, and the flexibility of asset use may be constrained.

- Resource Scarcity: Most firms have limited capital resources, which underlines the need for careful decisions. An incorrect decision could not only lead to losses but also hinder other more profitable investments due to a lack of funds.

2.6. Difficulties in Capital Budgeting

Capital expenditure decisions are essential but also come with several challenges:

- Uncertain Future Benefits: Benefits are received in the future, which is inherently uncertain and involves risk. Decisions require forecasting far into the future, with possible errors caused by a failure to predict changes in the market, consumer preferences, competitor actions, technology, and the economic or political environment.

- Time Value of Money: Costs and benefits occur in different time periods, making direct comparisons difficult due to the time value of money.

- Quantification Challenges: Not all benefits and costs can be easily quantified, and certain qualitative factors also play an important role.

3. Cost of Capital

The cost of capital is an essential element in capital budgeting. It is the minimum rate of return a firm must earn on its investments to satisfy its investors. In simple terms, it's the price a company pays for its funds.

4. Conclusion

Capital budgeting and investment appraisal are essential processes for determining which long-term investments are worth pursuing. These processes are used to select investments that aim to maximize shareholder wealth while taking into consideration different factors that affect profitability and risk. Decisions must take into account the time value of money and the uncertain nature of future benefits. In order to make informed decisions, firms must also take into account the cost of capital, as this sets a minimum benchmark for investment returns.

No Comments