Determining the optimal capital structure

Determining the "optimal" capital structure (the ideal mix of debt and equity financing) is a complex process that requires understanding different theories and considering the specific circumstances of a company. There's no one-size-fits-all solution, but by considering various factors and applying different models, a company can arrive at a financing mix that maximizes its value and minimizes its cost of capital. Here's a breakdown of the key considerations and a synthesis of how the theories inform the decision-making process:

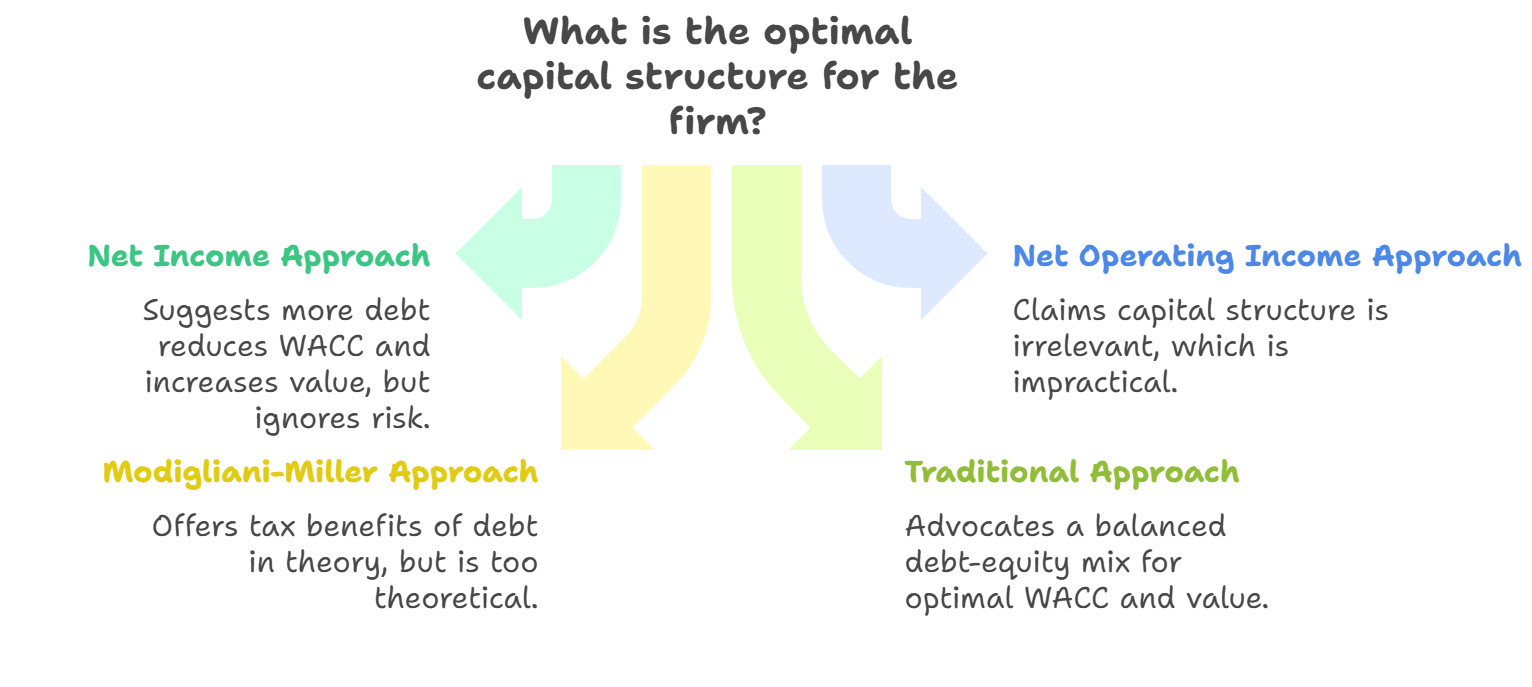

1. Understanding the Theoretical Landscape

Before diving into the practicalities, it's important to understand the different perspectives on capital structure:

- Net Income (NI) Approach: This approach suggests more debt is always better. It sees that increased debt decreases the WACC (Weighted Average Cost of Capital) and increases the overall value. This is too simplistic, as it ignores the increased risks associated with higher levels of debt.

- Net Operating Income (NOI) Approach: This states that capital structure is irrelevant. The WACC and the firm value are unaffected by changes in the debt-equity ratio. This approach is not practical either since capital structure in most cases affects the firm value.

- Modigliani-Miller (MM) Approach: MM starts with the same irrelevance premise (in a perfect market). But they add that in a world with corporate taxes, debt financing becomes preferable due to the interest tax shield. This offers a starting point but is too theoretical and doesn't account for other real-world considerations.

- Traditional Approach: This is the most pragmatic approach. There is a range of debt-equity mix that will decrease the WACC and increase the firm value to a certain point. Using debt more than this point will increase the WACC and decrease the value of the firm.

- Trade-Off Theory: Builds upon MM with taxes by introducing the costs of financial distress (including bankruptcy costs). It acknowledges the tax advantages of debt but recognizes that excessive debt increases the probability of financial distress. The optimal capital structure is found where the tax benefits of debt are balanced against the potential costs of financial distress.

- Signalling Theory: This looks at the impact of information asymmetry. Management with insider information can signal future prospects through financing choices. Issuing debt signals confidence in the company's ability to meet obligations, while issuing equity might signal that the company sees the current share price as overvalued.

- Pecking Order Theory: This proposes a hierarchy of financing preferences: (1) Internal financing (retained earnings), (2) Debt, and (3) Equity. Firms prefer internal financing due to lower costs and a lack of information asymmetry problems. Debt is preferred over equity to avoid diluting ownership and the negative signals associated with equity issuance.

2. Key Factors to Consider in Determining the Optimal Capital Structure

Here are factors that all the theories address, that will help to determine the optimal capital structure:

- Tax Rate: Higher tax rates make debt more attractive due to the tax shield.

- Business Risk: Businesses with stable cash flows and revenues can handle more debt than those with volatile earnings. Business risk is affected by cyclicality of demand, product characteristics, competition, regulation, and operating leverage.

- Financial Flexibility: Maintaining financial flexibility is important to be able to seize good opportunities without being limited by debt obligations.

- Industry Norms: A debt-equity ratio that is optimal may not be the same when compared to other industries.

- Credit Rating and Access to Capital Markets: A company's credit rating determines the interest rate at which they can borrow, and determines how much debt they can take on.

- Company Size: Larger companies can usually handle a larger amount of debt more easily than smaller companies.

- Market conditions: A good rule of thumb for an optimal debt to asset ratio would be somewhere between 40% and 60%.

3. Practical Steps to Determine the Optimal Capital Structure

Here's a systematic approach to find a good approximation of the optimal capital structure:

-

Assess Business Risk:

- Analyze the stability of the company's revenue, earnings, and cash flows.

- Evaluate the industry in which the company operates and the company's competitive position.

- Quantify business risk using metrics such as sales volatility, operating leverage, and earnings variability.

-

Evaluate Financing Needs and Flexibility:

- Determine the amount of financing required for current and future projects.

- Assess the need for financial flexibility to pursue growth opportunities or weather unexpected downturns.

- Consider any restrictive covenants of existing debt agreements.

-

Estimate the Cost of Capital at Different Leverage Levels:

- Project the cost of debt (ki) at various debt levels, considering the impact on credit ratings and interest rates.

- Estimate the cost of equity (ke) at different debt levels, taking into account the increased financial risk for equity holders (using the Capital Asset Pricing Model (CAPM) or other risk models).

- Calculate the weighted average cost of capital (WACC) for a range of debt-equity ratios.

-

Analyze the Tax Benefits of Debt:

- Calculate the tax shield provided by interest expense at various debt levels.

- Consider the impact of the tax shield on the company's overall cash flows and profitability.

-

Estimate the Costs of Financial Distress:

- Assess the probability of financial distress at different debt levels, considering the company's business risk and leverage.

- Estimate the direct and indirect costs associated with bankruptcy proceedings or financial reorganization.

-

Identify the Optimal Capital Structure:

- Find the debt-equity ratio that minimizes the WACC and maximizes the company's value.

- Consider the impact on key financial ratios, such as debt-to-equity, interest coverage, and debt service coverage.

4. Applying the Theories: A Combined Approach

- MM with Taxes as a Starting Point: This provides a baseline to understand the positive impacts of debt by looking at the tax shield.

- Trade-Off Theory: Refine the Baseline: Incorporate the cost of financial distress to see to what degree the increased debt increases financial risk and to find a "sweet spot".

- Signalling Theory: Check for Market Perceptions: Keep this theory in mind, since financial choices can have some effect on how the market perceives the firm's prospects.

- Pecking Order Theory: Be Pragmatic: There is little harm done using the Pecking Order to decide the order in which the firm gets the finances, it's not that important, but has some benefits when combined with other theories.

5. Cautions and Considerations

- Dynamic Nature of Capital Structure: A company's optimal capital structure can change over time due to changes in its business environment, financial performance, and market conditions.

- Qualitative Factors: Quantifiable analysis should be supplemented by qualitative considerations, such as management's risk tolerance, strategic goals, and the company's long-term vision.

- No Single "Perfect" Solution: Capital structure decisions often involve trade-offs, and there may not be a single "perfect" solution. The goal is to find a financing mix that provides a reasonable balance between value creation, risk management, and financial flexibility.

Conclusion

Determining the optimal capital structure is a complex balancing act. By understanding the different theories, considering a variety of factors, and applying a systematic approach, companies can make informed decisions that enhance their value and achieve their financial goals.

No Comments