Profitably Index Method

1. Introduction

The Profitability Index (PI) is a discounted cash flow (DCF) technique that measures the present value of returns per rupee invested. It's similar to the NPV approach but provides a relative measure of profitability, which is particularly useful when comparing projects with different initial investment sizes.

2. Definition

The Profitability Index (PI) is defined as the ratio of the present value of future cash inflows to the present value of cash outflows. It is also known as the benefit-cost ratio as the numerator measures benefits and the denominator measures costs. A better description would be the present value index.

3. Formula

The formula for the Profitability Index is:

PI = Present Value of Cash Inflows / Present Value of Cash Outflows

Where:

- Present Value of Cash Inflows = The sum of the present values of all future cash inflows.

- Present Value of Cash Outflows = The initial investment (or present value of all future cash outflows).

4. Accept-Reject Rule

- Accept if PI > 1: A project is acceptable if its PI is greater than one. This indicates that the project's benefits exceed its costs.

- Indifferent if PI = 1: The firm is indifferent to the project if the PI equals one, as the benefits are exactly equal to the costs.

- Reject if PI < 1: A project should be rejected if its PI is less than one as the costs exceed the benefits.

It's important to note the following relationship:

- When PI > 1, NPV is positive.

- When PI = 1, NPV is zero.

- When PI < 1, NPV is negative.

The NPV and PI approaches generally give the same results regarding investment proposals.

5. Ranking Projects

The PI can be used to rank projects based on their PI values, with projects with higher PIs being ranked higher.

6. Alternative PI Measurement

While the PI is commonly defined as the ratio of the PV of cash inflows divided by the PV of cash outflows, it can also be measured on the basis of the net benefits of a project against its current cash outlay. This is very useful in capital rationing situations. In this scenario, the decision rule is:

- Accept the project if the PI is positive.

- Reject the project if the PI is negative.

7. Illustration

Let us assume machines A and B with the following present values.

- Present Value of Cash Inflows for Machine A = Rs 68,645

- Present Value of Cash Inflows for Machine B = Rs 71,521

- Present Value of Cash Outflows for Both Machines = Rs 56,125

PI (Machine A) = 68,645 / 56,125 = 1.22

PI (Machine B) = 71,521 / 56,125 = 1.27

Since the PI for both machines is greater than 1, both machines are acceptable. Also, machine B would be preferred over machine A due to higher PI.

8. Evaluation

8.1. Advantages

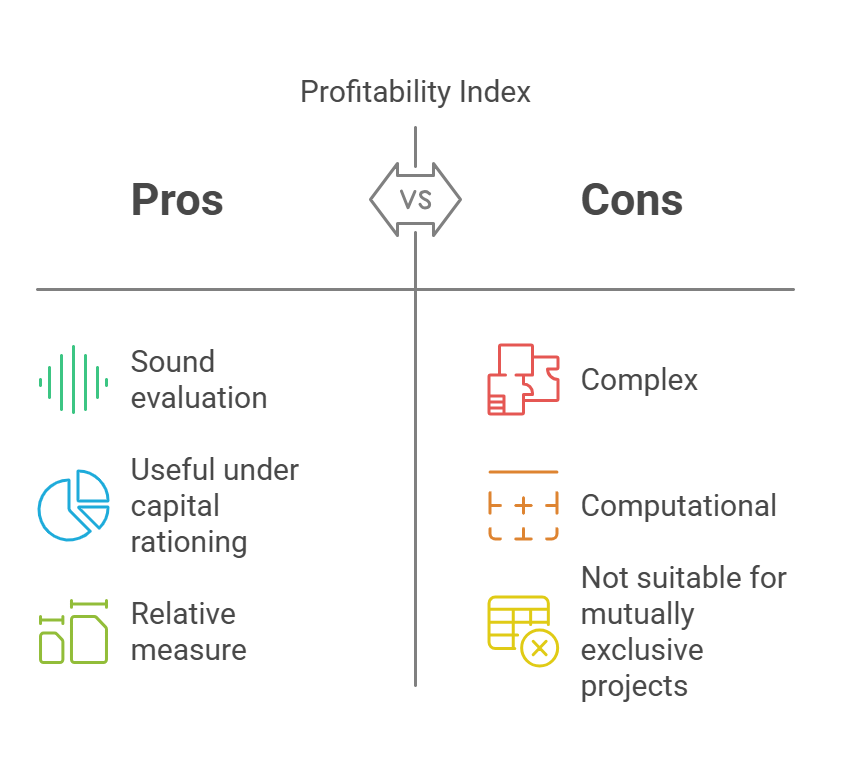

- Sound Evaluation: Like other discounted cash flow techniques, PI meets all the criteria of a sound investment criterion, including the time value of money and the totality of benefits.

- Useful Under Capital Rationing: It's a superior technique to NPV in situations of capital rationing as it evaluates projects based on relative magnitudes.

- Provides Relative Measure: PI provides a relative measure unlike NPV which is absolute.

8.2. Limitations

- Complex: It is more difficult to understand compared to the simpler traditional methods.

- Computational: PI involves more computations than traditional methods although less than the Internal Rate of Return (IRR).

- Mutually Exclusive Projects: The NPV method is superior to the PI method in certain mutually exclusive investment situations.

9. Comparison with NPV

- NPV: Measures the absolute value created by an investment (present value of inflows - present value of outflows).

- PI: Measures the relative value created by an investment, or the present value of benefits per rupee invested.

- Ranking: PI is particularly useful in capital rationing, where the firm must choose from among the most profitable projects given limited investment capital. Although, in some mutually exclusive scenarios, the NPV method is superior.

10. Conclusion

The Profitability Index (PI) is a powerful time-adjusted capital budgeting technique that is particularly useful for comparing projects that involve different investment sizes. It provides a relative measure of profitability, which makes it a better measure to compare competing projects that require different levels of investment. While it is based on NPV, it offers a unique perspective. However, when dealing with mutually exclusive projects, other techniques like NPV should be preferred.

No Comments