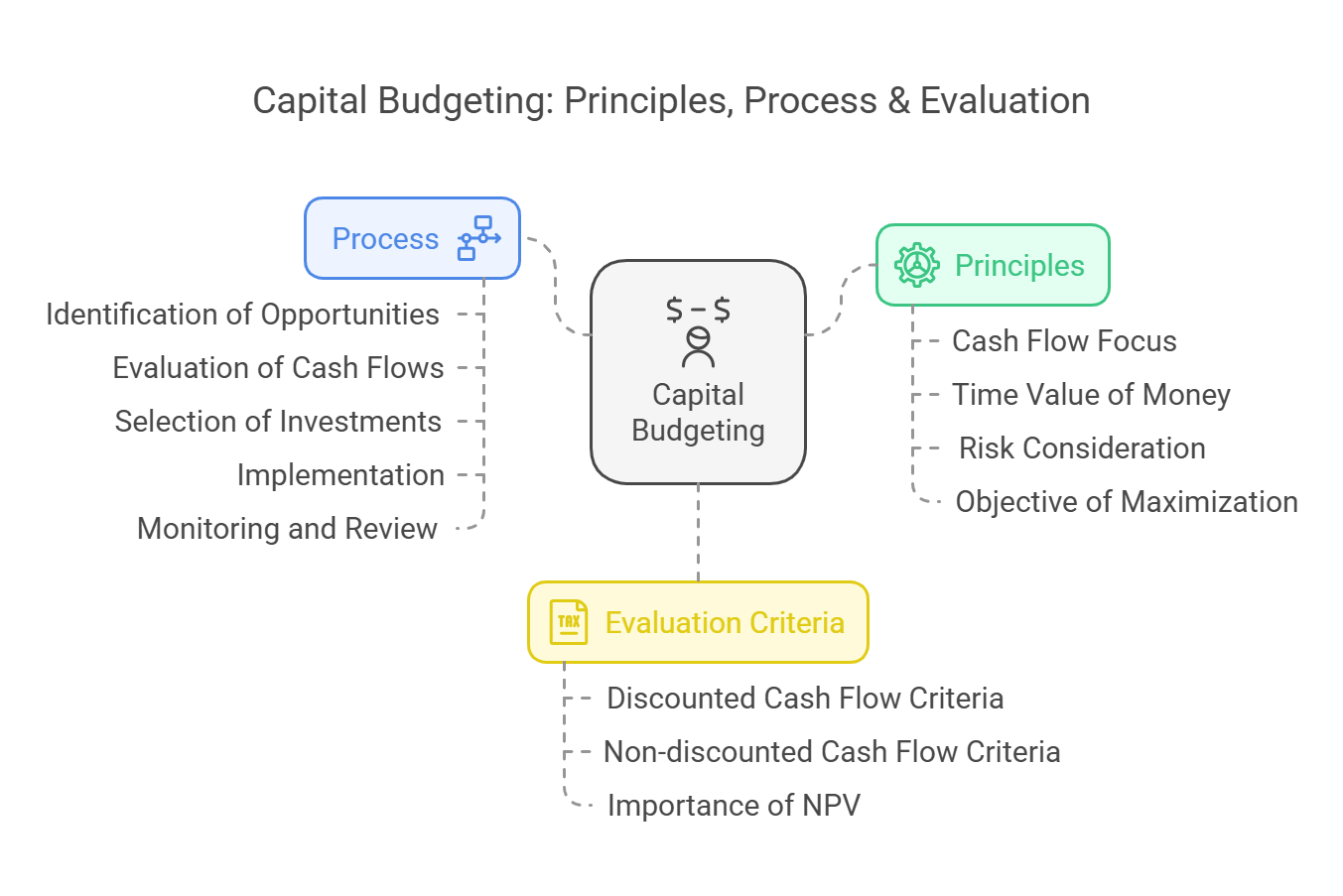

Principles and Process

1. Principles of Capital Budgeting

Capital budgeting decisions are guided by several core principles:

Capital budgeting decisions are guided by several core principles:

-

Cash Flow Focus:

- Decisions should be based on cash flows rather than accounting profits. Cash flows represent the actual movement of money, which is critical for investment analysis.

-

Time Value of Money:

- Future cash flows should be discounted to their present value. A dollar today is worth more than a dollar in the future due to its earning potential.

-

Risk Consideration:

- Future cash flows are inherently uncertain, and this risk must be considered in the evaluation. Risk adjustment is necessary to account for uncertainty.

-

Objective of Maximization:

- The ultimate goal of capital budgeting is to maximize shareholder wealth. Investment decisions should be consistent with this objective.

2. Capital Budgeting Process

The capital budgeting process typically involves the following steps:

-

Identification of Investment Opportunities:

- This involves generating new investment ideas and identifying projects that align with the firm's goals.

-

Evaluation of Relevant Cash Flows & Terminal Value:

- This step requires estimating the cash inflows and outflows associated with each investment opportunity. It is important to focus on incremental, after-tax cash flows and consider the terminal value of the investment.

-

Selection of an Investment Based on Evaluation Techniques:

- This step utilizes a variety of techniques, including both discounted and non-discounted cash flow methods, to evaluate the viability of potential investments and make informed choices.

-

Implementation of the Investment:

- Once a project has been selected, this involves taking the necessary steps to implement the project.

-

Monitoring and Review of Performance:

- This involves tracking the performance of a project against the original projections, and making any necessary adjustments.

3. Investment Evaluation Criteria

3.1. Three Steps of Investment Evaluation

The evaluation of an investment involves three crucial steps:

-

Estimation of Cash Flows:

- Calculating the relevant cash flows, including both inflows and outflows.

-

Estimation of the Required Rate of Return:

- Determining the opportunity cost of capital, which is the minimum rate of return an investment must achieve to be considered worthwhile.

-

Application of a Decision Rule:

- Using a specific decision rule or technique to analyze the estimated cash flows and make a choice.

3.2. Essential Properties of a Sound Evaluation Technique

A sound appraisal technique for investment projects should:

3.3. Categories of Evaluation Criteria

Investment criteria are typically grouped into two main categories:

-

Discounted Cash Flow (DCF) Criteria:

- Net Present Value (NPV): Calculates the present value of all cash flows associated with a project.

- Internal Rate of Return (IRR): Calculates the discount rate at which the net present value of a project equals zero.

- Profitability Index (PI): Measures the ratio of the present value of future cash flows to the initial investment.

-

Non-discounted Cash Flow Criteria:

- Payback Period (PB): Determines how long it takes for an investment to generate enough cash to recover its initial cost.

- Discounted Payback Period: Similar to the payback period but considers the time value of money by using discounted cash flows.

- Accounting Rate of Return (ARR): Calculates the average accounting profit relative to the initial investment.

3.4. Importance of Net Present Value (NPV)

The document mentions that the net present value (NPV) criterion is considered the most valid technique for evaluating an investment project because it is consistent with the objective of maximizing shareholder wealth.

4. Conclusion

Capital budgeting is a vital process for making strategic investment decisions. By adhering to sound principles, following a structured process, and using effective evaluation criteria, organizations can allocate resources efficiently, manage risk, and increase shareholder value. While a variety of methods exist, the NPV criterion is considered to be one of the most valid because it aligns directly with the objective of maximizing shareholder wealth.

No Comments