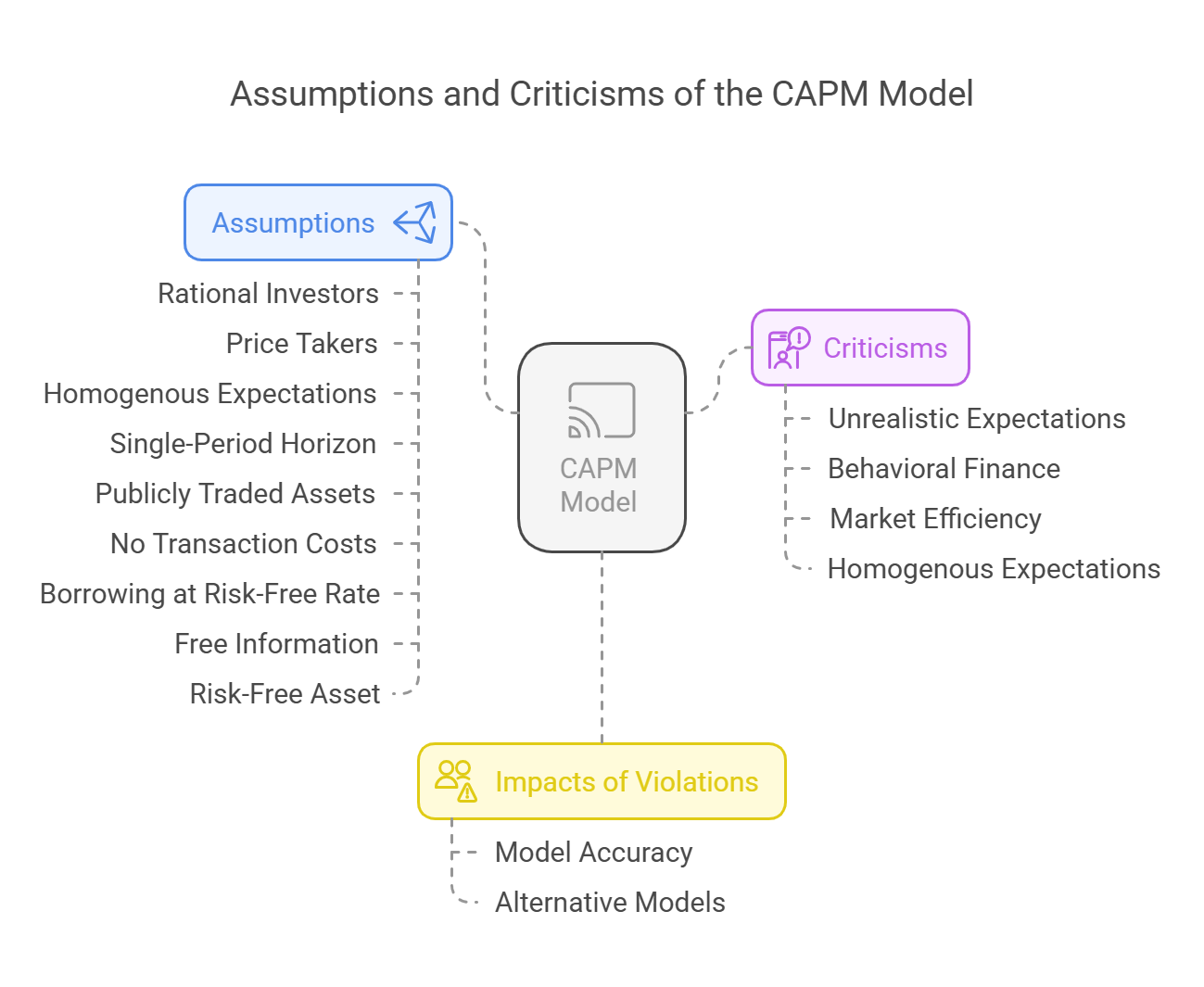

Assumptions of the Single-Period Classical CAPM Model

Core Concept: The Capital Asset Pricing Model (CAPM) is a theoretical model that relies on a set of simplifying assumptions to establish a relationship between systematic risk and expected return. Understanding these assumptions is crucial for evaluating the model's validity and limitations.

Key Assumptions of the Single-Period Classical CAPM Model:

Key Assumptions of the Single-Period Classical CAPM Model:

-

1. Investors are Rational and Risk-Averse:

- Explanation: Investors are assumed to be rational, meaning they make decisions that are consistent with maximizing their expected utility. They are also assumed to be risk-averse, meaning they prefer lower risk for a given level of expected return.

- Implication: Investors will only take on additional risk if they are compensated with a higher expected return.

-

2. Investors are Price Takers:

- Explanation: Individual investors are assumed to be small relative to the overall market and cannot influence market prices through their trading activity.

- Implication: Investors accept market prices as given and make investment decisions based on their own analysis and preferences.

-

3. Investors Have Homogenous Expectations:

- Explanation: All investors are assumed to have the same expectations about future asset returns, standard deviations, and correlation coefficients. They all analyze the same information and arrive at the same conclusions.

- Implication: All investors will perceive the same efficient frontier and the same tangency portfolio.

-

4. Single-Period Investment Horizon:

- Explanation: All investors are assumed to have the same single-period investment horizon (e.g., one year).

- Implication: Investors make investment decisions based on expected returns and risks over that single period.

-

5. All Assets are Publicly Traded and Perfectly Divisible:

- Explanation: All assets are assumed to be publicly traded, meaning they can be easily bought and sold in the market. They are also assumed to be perfectly divisible, meaning they can be bought and sold in any quantity.

- Implication: Investors can construct portfolios with any desired combination of assets.

-

6. There are No Transaction Costs or Taxes:

- Explanation: There are assumed to be no transaction costs associated with buying or selling assets, and there are no taxes on investment returns.

- Implication: Investors can trade freely without incurring any costs that would affect their investment decisions.

-

7. Borrowing and Lending at the Risk-Free Rate:

- Explanation: Investors can borrow and lend unlimited amounts of money at the risk-free rate.

- Implication: Investors can leverage their investments in the market portfolio by borrowing at the risk-free rate and investing the proceeds in the market portfolio.

-

8. Information is Freely and Simultaneously Available to All Investors:

- Explanation: All investors have access to the same information at the same time.

- Implication: No investor has an informational advantage over others.

-

9. There exists a Risk-Free Asset:

- Explanation: A risk-free asset is available, and investors can invest in it without the concern of default.

- Implication: Investors can construct portfolios with any desired level of risk by combining this asset with a risky portfolio.

Criticisms of the Assumptions:

- Unrealistic Expectations: Many of the CAPM's assumptions are unrealistic and do not hold true in the real world.

- Behavioral Finance: The assumption of rational investors is challenged by behavioral finance, which suggests that investors are often influenced by emotions and cognitive biases.

- Market Efficiency: The CAPM assumes that the market is efficient and that prices reflect all available information. However, there is evidence that markets are not always efficient and that opportunities for abnormal returns may exist.

- Homogenous Expectations: The assumption of homogenous expectations is also unrealistic, as investors often have different information and beliefs.

Impact of Violated Assumptions:

- When the assumptions of the CAPM are violated, the model may not accurately predict asset returns.

- Alternative asset pricing models, such as the Fama-French Three-Factor Model and Arbitrage Pricing Theory (APT), have been developed to address some of the limitations of the CAPM.

Conclusion:

The assumptions of the single-period classical CAPM model are highly restrictive and do not fully reflect the complexities of the real world. While the CAPM provides a valuable framework for understanding the relationship between risk and return, it is important to be aware of its limitations and to use it in conjunction with other investment tools and strategies.

No Comments