Market Model

Concept of Beta, Systematic and Unsystematic Risk

Core Concept: The Market Model is a simplified version of the Capital Asset Pricing Model (CAPM) that relates the return of an individual asset or portfolio to the return of the overall market. It provides a framework for understanding and quantifying systematic and unsystematic risk, and for estimating an asset's beta.

Formula:

Formula:

Ri = αi + βi * Rm + εi

- Where:

-

Ri= Return of asset i -

αi= Alpha of asset i (the asset's expected excess return when the market return is zero) -

βi= Beta of asset i (a measure of the asset's systematic risk or sensitivity to market movements) -

Rm= Return of the market -

εi= Error term (unsystematic risk)

-

1. Concept of Beta (β)

- Definition: Beta (β) is a measure of an asset's systematic risk, also known as market risk or non-diversifiable risk. It quantifies how much an asset's return is expected to move in response to changes in the market return.

-

Interpretation:

-

β = 1: The asset's return is expected to move in the same direction and magnitude as the market return. -

β > 1: The asset is more volatile than the market. Its return is expected to amplify market movements (higher systematic risk). -

β < 1: The asset is less volatile than the market. Its return is expected to dampen market movements (lower systematic risk). -

β = 0: The asset's return is uncorrelated with the market return. -

β < 0: The asset's return tends to move in the opposite direction of the market return (rare).

-

-

Calculation:

- Beta can be estimated using historical data by regressing the asset's returns against the market returns.

- Formula:

-

βi = Cov(Ri, Rm) / Var(Rm)- Where:

-

Cov(Ri, Rm)= Covariance between the asset's return and the market return -

Var(Rm)= Variance of the market return

-

- Where:

-

-

Example:

- If a stock has a beta of 1.5, it is expected to increase by 15% if the market increases by 10%. Conversely, it is expected to decrease by 15% if the market decreases by 10%.

-

Usefulness:

- Beta helps investors assess the systematic risk of an asset or portfolio.

- It is a key input in the Capital Asset Pricing Model (CAPM), which is used to estimate the required rate of return on an investment.

2. Systematic Risk

- Definition: Systematic risk (also known as market risk or non-diversifiable risk) is the risk that is inherent to the entire market or a large segment of it. It cannot be eliminated through diversification.

-

Sources of Systematic Risk:

- Economic Factors: Changes in interest rates, inflation, economic growth, and unemployment.

- Political Factors: Changes in government policies, regulations, and political stability.

- Global Events: International conflicts, natural disasters, and global economic trends.

-

Examples of Systematic Risk:

- A recession that leads to lower corporate earnings and reduced stock prices across the board.

- An increase in interest rates that reduces the value of bonds and increases borrowing costs for companies.

-

Measurement of Systematic Risk:

- Beta is the primary measure of systematic risk.

-

Management of Systematic Risk:

- Systematic risk cannot be eliminated through diversification, but it can be managed by:

- Hedging: Using financial instruments (e.g., options, futures) to offset potential losses.

- Asset Allocation: Adjusting the portfolio's asset allocation to reduce exposure to certain types of assets.

- Strategic Portfolio Positioning: Making adjustments based on macroeconomic forecasts.

- Systematic risk cannot be eliminated through diversification, but it can be managed by:

3. Unsystematic Risk

- Definition: Unsystematic risk (also known as company-specific risk, diversifiable risk, or idiosyncratic risk) is the risk that is specific to a particular company or industry. It can be reduced or eliminated through diversification.

-

Sources of Unsystematic Risk:

- Management Decisions: Poor management, ineffective strategies, and operational inefficiencies.

- Product Failures: Failure of a new product or service to gain market acceptance.

- Labor Disputes: Strikes or other labor-related issues.

- Regulatory Changes: Changes in regulations that negatively impact a specific company or industry.

- Litigation: Lawsuits and legal challenges.

-

Examples of Unsystematic Risk:

- A product recall that damages a company's reputation and reduces sales.

- A strike that disrupts a company's operations.

- A lawsuit that results in significant financial losses for a company.

-

Measurement of Unsystematic Risk:

- The error term (εi) in the Market Model represents the unsystematic risk of an asset. It is the portion of the asset's return that is not explained by the market return.

- The standard deviation of the error term is a measure of unsystematic risk.

-

Management of Unsystematic Risk:

- Diversification: The most effective way to manage unsystematic risk is to diversify the portfolio by investing in a variety of assets across different sectors and industries.

- Due Diligence: Conducting thorough research and analysis of individual companies before investing.

4. Relationship Between Beta, Systematic Risk, and Unsystematic Risk

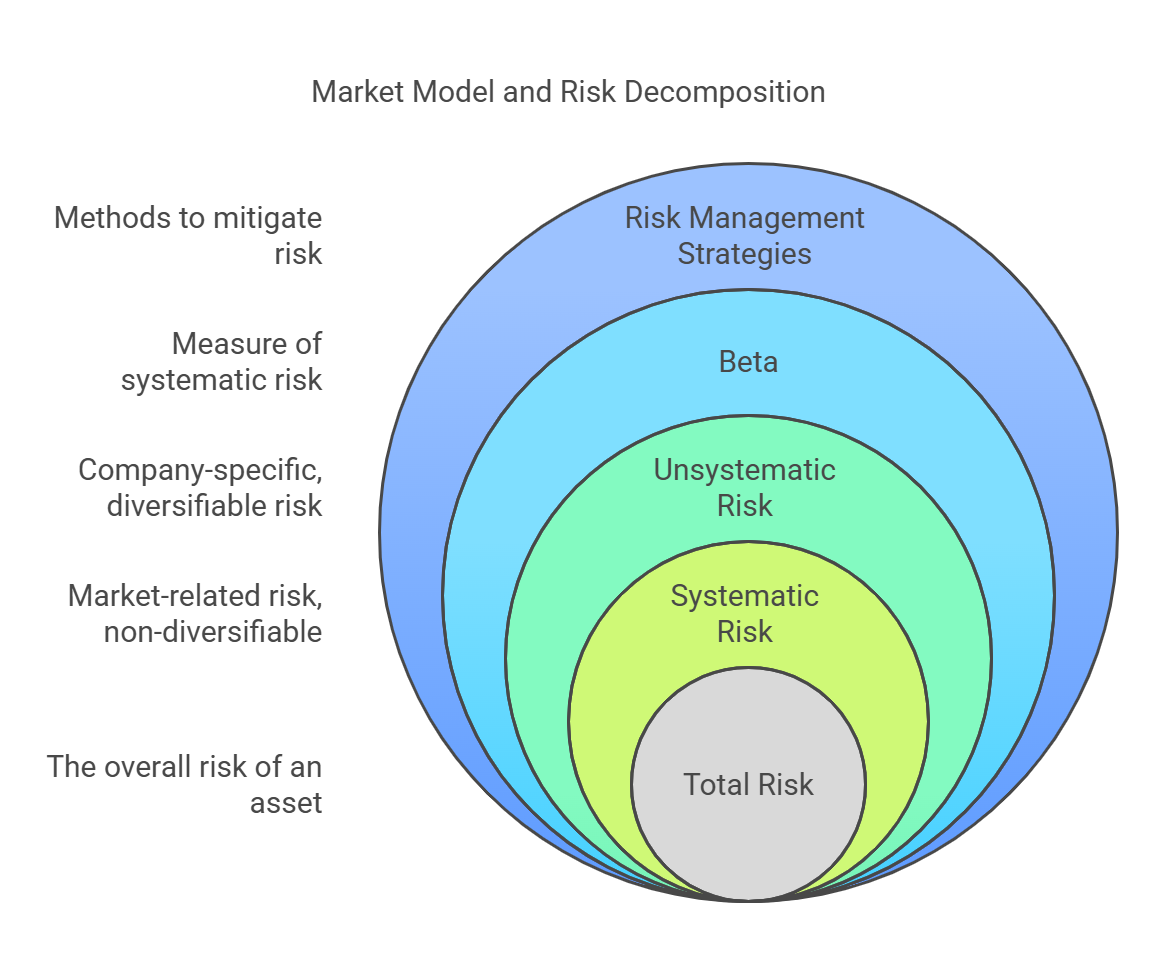

- The Market Model decomposes the total risk of an asset into two components: systematic risk (measured by beta) and unsystematic risk (represented by the error term).

-

Total Risk = Systematic Risk + Unsystematic Risk - By diversifying the portfolio, investors can reduce or eliminate unsystematic risk, leaving only systematic risk. This is why beta is considered a measure of non-diversifiable risk.

Conclusion:

The Market Model provides a valuable framework for understanding and quantifying the relationship between an asset's return and the market return. By understanding the concepts of beta, systematic risk, and unsystematic risk, investors can make more informed decisions about portfolio construction and risk management. While diversification can effectively reduce unsystematic risk, investors must also be aware of systematic risk and manage it through asset allocation and hedging strategies.

No Comments