Traditional Portfolio Management for Individuals

Objectives, Constraints, and Considerations

Core Concept: Traditional portfolio management for individuals involves a structured process of setting investment objectives, identifying constraints, and developing a strategy to achieve those objectives while considering the individual's unique circumstances. This process aims to create a portfolio that balances risk and return and aligns with the investor's needs, preferences, and financial situation.

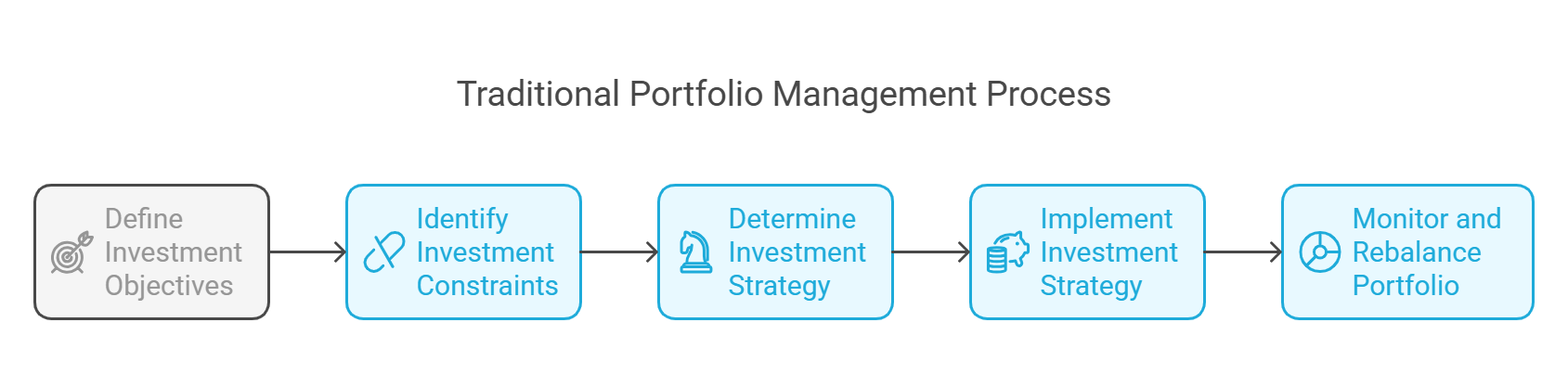

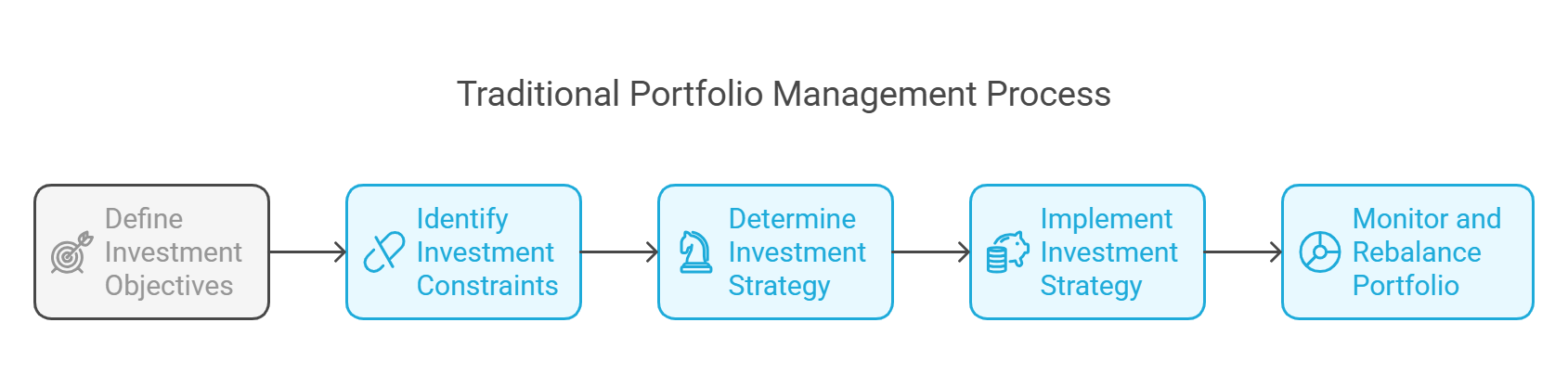

Key Steps in Traditional Portfolio Management:

- Define Investment Objectives:

- Identify Investment Constraints:

- Determine Investment Strategy:

- Implement the Investment Strategy:

- Monitor and Rebalance the Portfolio:

Factors to Consider:

1. Objectives

- Definition: Investment objectives are the specific financial goals that the investor is trying to achieve. They should be clearly defined, measurable, achievable, relevant, and time-bound (SMART).

-

Common Investment Objectives:

- Capital Preservation: Protecting the principal investment from loss. Suitable for risk-averse investors or those with a short time horizon.

- Income Generation: Generating a steady stream of income from the portfolio. Suitable for retirees or those seeking current income.

- Capital Appreciation: Growing the portfolio's value over time. Suitable for younger investors with a long time horizon.

- Specific Goals: Saving for retirement, education, a down payment on a home, or other specific life goals.

-

Example:

- A retiree may have an objective of generating ₹50,000 per month in income from their portfolio while preserving their capital.

- A young professional may have an objective of growing their portfolio by 8% per year to save for retirement.

2. Constraints

- Definition: Investment constraints are the limitations or restrictions that affect the investor's ability to achieve their objectives.

-

Common Investment Constraints:

-

a) Time Horizon:

- The length of time the investor has to achieve their investment objectives.

- Long Time Horizon: Allows for greater risk-taking and investment in growth-oriented assets.

- Short Time Horizon: Requires a more conservative approach with a focus on capital preservation and liquidity.

- Example: A 25-year-old saving for retirement has a long time horizon, while a 60-year-old approaching retirement has a shorter time horizon.

-

b) Current Wealth:

- The amount of assets the investor currently has available to invest.

- Limited Wealth: Requires a more conservative approach with a focus on generating income and preserving capital.

- Significant Wealth: Allows for greater flexibility and diversification across a wider range of asset classes.

- Example: An investor with ₹10 lakh to invest will have different portfolio options than an investor with ₹1 crore.

-

c) Tax Considerations:

- The impact of taxes on investment returns.

- Tax-Advantaged Accounts: Utilize tax-deferred or tax-exempt accounts (e.g., retirement accounts) to minimize the impact of taxes.

- Tax-Efficient Investing: Employ strategies to minimize taxes on investment gains (e.g., tax-loss harvesting, holding investments for the long term).

- Example: An investor in a high tax bracket may prefer to invest in municipal bonds, which are exempt from federal income tax.

-

d) Liquidity Requirements:

- The need to access funds quickly and easily.

- High Liquidity Needs: Requires a portfolio with a significant allocation to liquid assets (e.g., cash, money market funds, short-term bonds).

- Low Liquidity Needs: Allows for a greater allocation to less liquid assets (e.g., real estate, private equity).

- Example: An investor who anticipates needing to access funds for unexpected expenses should maintain a higher level of liquidity.

-

e) Legal and Regulatory Factors:

- Legal and regulatory requirements that may affect investment decisions.

- Example: Restrictions on certain types of investments or limits on the amount that can be invested in certain accounts.

-

f) Unique Circumstances:

- Any other factors that may affect the investor's ability to achieve their objectives.

- Example: Ethical considerations, religious beliefs, or specific investment preferences.

-

g) Anticipated Inflation:

- The expected rate of increase in prices over time.

- High Inflation: Requires a portfolio with a higher allocation to assets that are likely to outpace inflation (e.g., stocks, real estate, commodities).

- Low Inflation: Allows for a more conservative approach with a greater allocation to fixed-income assets.

- Example: If inflation is expected to be 5% per year, the portfolio should generate a return of at least 5% to maintain its purchasing power.

-

a) Time Horizon:

3. Determining Investment Strategy

-

Asset Allocation: The process of dividing the portfolio among different asset classes (e.g., stocks, bonds, real estate, commodities).

- Strategic Asset Allocation: Establishes a long-term asset allocation based on the investor's objectives and constraints.

- Tactical Asset Allocation: Makes short-term adjustments to the asset allocation based on market conditions.

-

Security Selection: The process of choosing specific securities within each asset class.

- Active Management: Involves actively selecting securities with the goal of outperforming the market.

- Passive Management: Involves investing in index funds or exchange-traded funds (ETFs) that track a specific market index.

- Risk Management: Employing strategies to manage the portfolio's risk, such as diversification, hedging, and stop-loss orders.

4. Implementing the Investment Strategy

- Opening Accounts: Setting up brokerage accounts or other investment accounts.

- Funding the Portfolio: Transferring funds into the investment accounts.

- Executing Trades: Buying and selling securities to implement the desired asset allocation and security selection.

5. Monitoring and Rebalancing the Portfolio

- Monitoring Performance: Regularly tracking the portfolio's performance and comparing it to the investor's objectives.

- Rebalancing: Periodically adjusting the portfolio to maintain the desired asset allocation. This involves selling assets that have increased in value and buying assets that have decreased in value.

-

Adjusting Strategy: Making adjustments to the investment strategy as needed based on changes in the investor's objectives, constraints, or market conditions.

Conclusion:

Conclusion:

Traditional portfolio management for individuals involves a comprehensive and structured process that considers the investor's unique circumstances and goals. By carefully defining objectives, identifying constraints, and developing a well-diversified and risk-managed portfolio, investors can increase their chances of achieving their financial objectives.

No Comments