Alternatives to Traditional Reinsurance

Securitization of Risk and Catastrophe Bonds

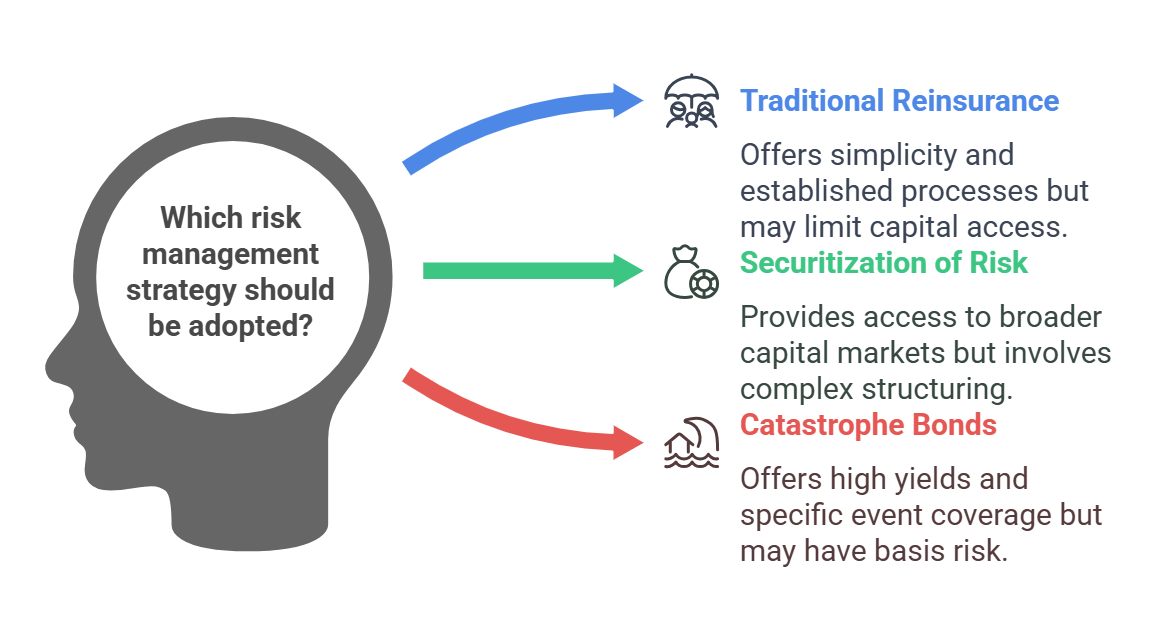

In addition to traditional reinsurance, insurance companies can use alternative risk transfer (ART) mechanisms to manage their risk exposure. Two prominent examples are securitization of risk and catastrophe bonds. These methods allow insurers to access capital markets to transfer risk, diversifying their risk management strategies.

I. Securitization of Risk:

-

A. Definition:

- Description: Securitization of risk involves packaging insurance risks into financial instruments that can be sold to investors in the capital markets. This allows insurers to transfer risk to a broader pool of investors beyond traditional reinsurers.

- Mechanism: An insurer creates a special purpose vehicle (SPV), which issues securities to investors. The proceeds from the sale of these securities are used to collateralize the insurer's risk. If a covered event occurs, the investors bear the loss; otherwise, they receive a return on their investment.

-

B. Key Characteristics:

- Access to Capital Markets: Allows insurers to access a wider range of capital than traditional reinsurance.

- Diversification of Risk: Transfers risk to investors who may not be directly involved in the insurance industry.

- Reduced Credit Risk: The risk is collateralized, reducing the credit risk for the ceding insurer.

- Complex Structure: Securitization transactions can be complex and require specialized expertise.

-

C. Process:

- Risk Assessment: Insurer identifies specific insurable risks.

- SPV Creation: A Special Purpose Vehicle (SPV) is created.

- Security Issuance: SPV issues securities (e.g., bonds) to investors.

- Collateralization: Funds from the security sales are collateralized.

- Risk Transfer: If a specified event occurs, funds are used to pay the insurer’s losses.

II. Catastrophe Bonds (Cat Bonds):

-

A. Definition:

- Description: Catastrophe bonds are a type of security specifically designed to transfer catastrophic risks, such as hurricanes, earthquakes, and other natural disasters, from insurers to investors.

- Mechanism: An insurer (or sponsor) issues a cat bond through an SPV. Investors purchase the bonds, providing the insurer with coverage for specified catastrophic events. If a covered event occurs and triggers the bond, the investors lose their principal, which is used to pay the insurer's claims. If no trigger event occurs during the bond's term, investors receive their principal back, plus a coupon payment.

-

B. Key Characteristics:

- Specific Trigger Events: Cat bonds are triggered by specific events, such as a hurricane of a certain intensity or an earthquake of a certain magnitude.

- Defined Coverage: The coverage provided by the bond is limited to the specified trigger events.

- Investor Risk: Investors bear the risk of loss if a trigger event occurs.

- High Yields: Cat bonds typically offer higher yields than other types of bonds to compensate investors for the risk they are taking.

-

C. Advantages of Cat Bonds:

- Access to Capital Markets: Provides access to a large pool of capital from investors.

- Multi-Year Coverage: Cat bonds typically provide coverage for multiple years.

- Reduced Credit Risk: The risk is collateralized, reducing the credit risk for the insurer.

- Diversification: Helps insurers diversify their risk management strategies.

-

D. Disadvantages of Cat Bonds:

- Complexity: Cat bond transactions can be complex and expensive to structure.

- Basis Risk: There may be a mismatch between the actual losses incurred by the insurer and the trigger event specified in the bond.

- Investor Sentiment: The market for cat bonds can be affected by investor sentiment and market conditions.

III. Comparison of Traditional Reinsurance, Securitization, and Cat Bonds:

| Feature | Traditional Reinsurance | Securitization of Risk | Catastrophe Bonds |

|---|---|---|---|

| Risk Transfer | Insurer to reinsurer | Insurer to capital markets | Insurer to capital markets |

| Capital Source | Reinsurers | Capital market investors | Capital market investors |

| Credit Risk | Reinsurer's solvency | Collateralized | Collateralized |

| Term | Typically 1 year | Varies | Typically 3-5 years |

| Complexity | Relatively simple | Complex | Complex |

| Cost | Varies based on risk | High structuring costs | High structuring costs |

| Trigger | Actual losses | Modeled losses | Pre-defined event |

Securitization of risk and catastrophe bonds provide insurers with valuable alternatives to traditional reinsurance, allowing them to access capital markets, diversify their risk management strategies, and protect themselves against catastrophic losses. However, these mechanisms are complex and require careful consideration of their costs and benefits.

Securitization of risk and catastrophe bonds provide insurers with valuable alternatives to traditional reinsurance, allowing them to access capital markets, diversify their risk management strategies, and protect themselves against catastrophic losses. However, these mechanisms are complex and require careful consideration of their costs and benefits.

No Comments