Endorsements and Riders

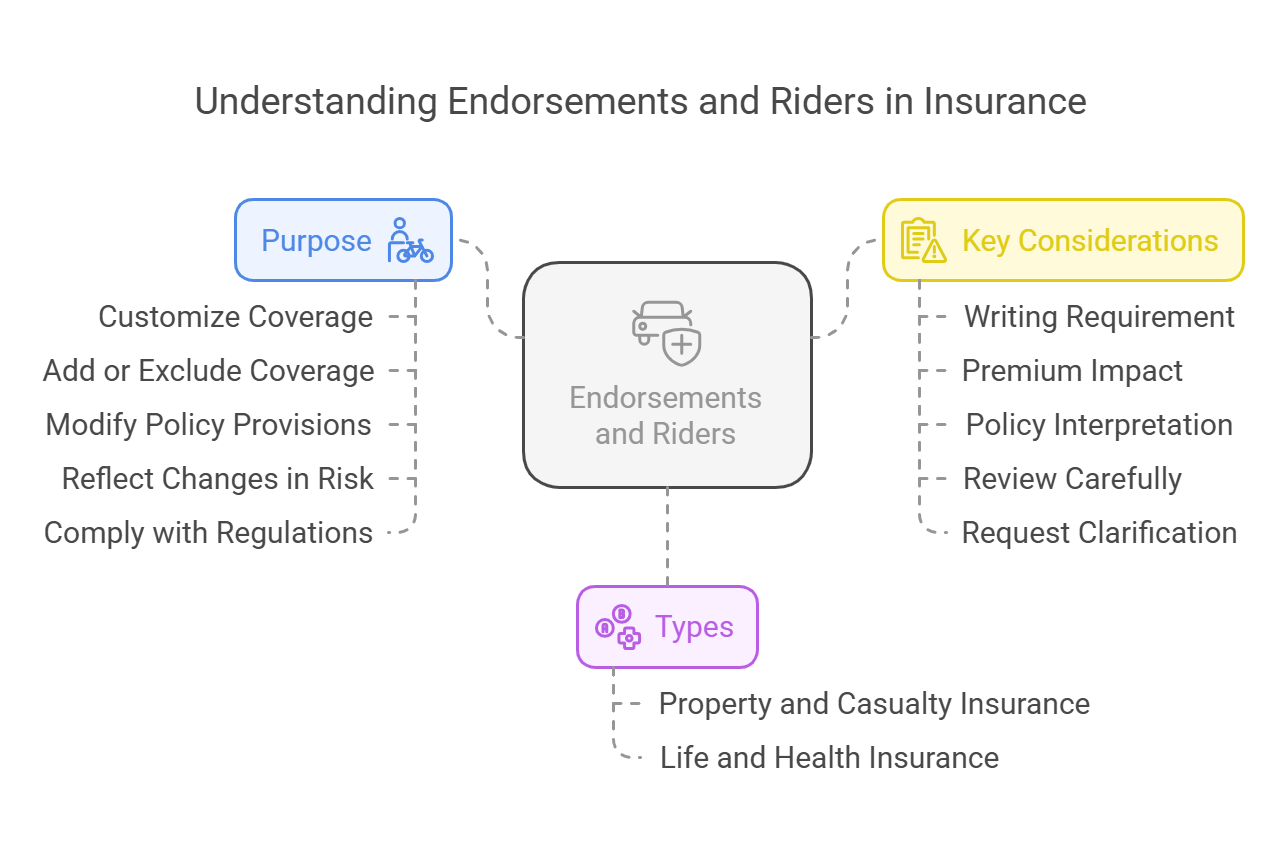

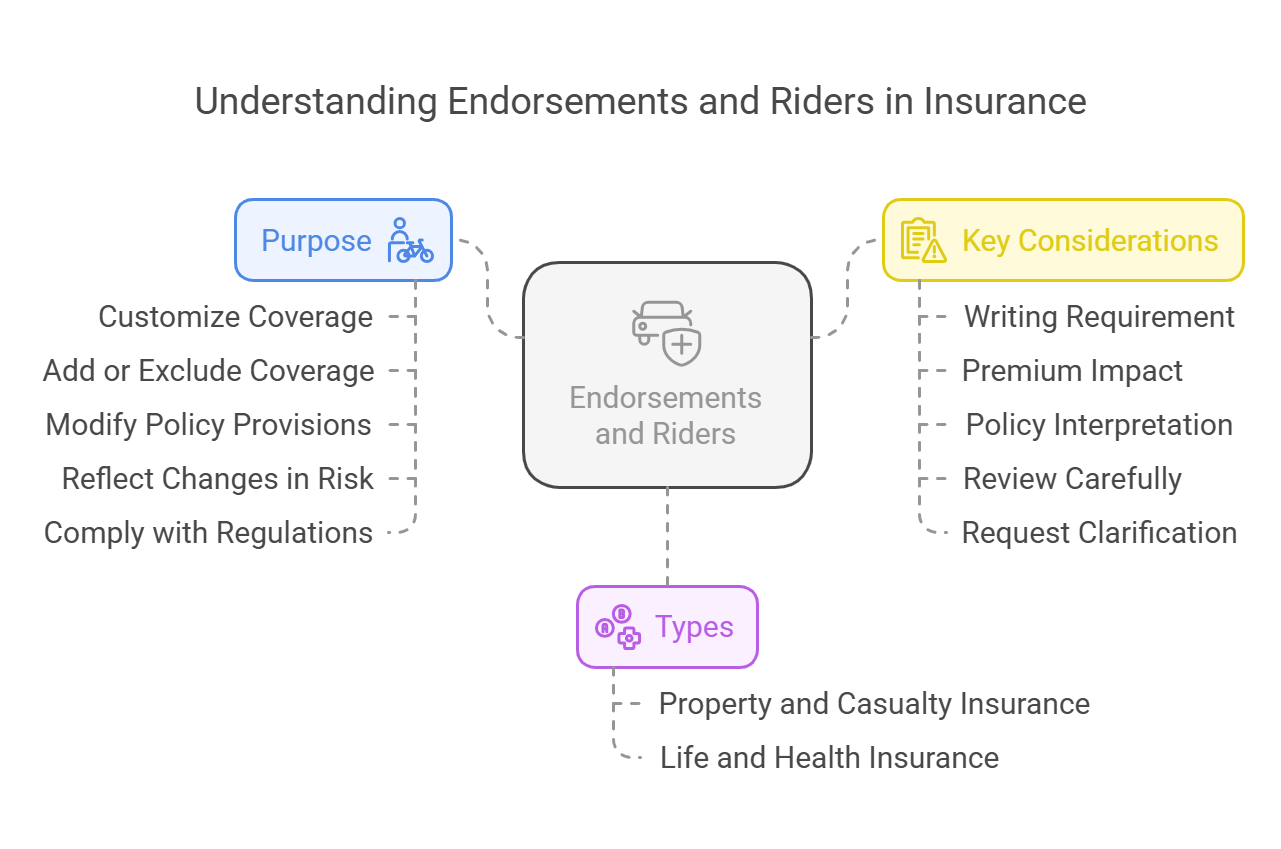

Endorsements and riders are written provisions that add to, modify, or delete provisions in the original insurance policy. They are used to customize the policy to meet the specific needs of the insured or to address changes in the risk being insured. The terms "endorsement" and "rider" are often used interchangeably, although "endorsement" is more common in property and casualty insurance, while "rider" is more common in life and health insurance.

- Definition: An endorsement or rider is a written amendment to an insurance policy that changes the original terms, conditions, or coverage of the policy.

I. Purpose of Endorsements and Riders:

-

A. Customize Coverage: To tailor the policy to the specific needs of the insured.

- Example: Adding coverage for specific types of property or perils that are not covered by the standard policy.

-

B. Add or Exclude Coverage: To add or exclude certain types of coverage.

- Example: Adding coverage for flood damage or excluding coverage for certain types of activities.

-

C. Modify Policy Provisions: To change the terms or conditions of the policy.

- Example: Changing the deductible or the policy limits.

-

D. Reflect Changes in Risk: To reflect changes in the risk being insured, such as a change in the insured's address or the type of business they operate.

-

E. Comply with Regulations: To comply with changes in insurance laws or regulations.

II. Types of Endorsements and Riders:

-

A. Property and Casualty Insurance:

-

Examples:

- Scheduled Personal Property Endorsement: Adds coverage for specific items of personal property, such as jewelry, artwork, or collectibles, that are not adequately covered by the standard policy.

- Earthquake Endorsement: Adds coverage for earthquake damage, which is typically excluded from standard homeowners policies.

- Flood Endorsement: Adds coverage for flood damage, which is typically excluded from standard homeowners policies (often purchased as a separate policy through the National Flood Insurance Program).

- Business Interruption Endorsement: Adds coverage for lost profits and expenses due to a temporary shutdown of a business caused by a covered peril.

- Hired and Non-Owned Auto Liability Endorsement: Provides liability coverage for vehicles that are hired or borrowed by a business.

-

Examples:

-

B. Life and Health Insurance:

-

Examples:

- Accidental Death and Dismemberment (AD&D) Rider: Pays an additional benefit if the insured dies or loses a limb due to an accident.

- Waiver of Premium Rider: Waives the premium payments if the insured becomes disabled.

- Guaranteed Insurability Rider: Allows the insured to purchase additional life insurance coverage at specified intervals without providing evidence of insurability.

- Long-Term Care Rider: Provides benefits to cover the costs of long-term care services.

- Accelerated Death Benefit Rider: Allows the insured to access a portion of the death benefit if they are diagnosed with a terminal illness.

-

Examples:

III. Key Considerations:

- A. Writing Requirement: Endorsements and riders must be in writing and attached to the original policy.

- B. Premium Impact: Endorsements and riders may increase or decrease the premium, depending on the nature of the change.

- C. Policy Interpretation: Endorsements and riders take precedence over the original policy provisions. If there is a conflict between the endorsement or rider and the original policy, the endorsement or rider will control.

- D. Review Carefully: It is important to review endorsements and riders carefully to ensure that they accurately reflect the intended changes to the policy.

-

E. Request Clarification: If you have any questions about an endorsement or rider, ask the insurer for clarification.

Endorsements and riders are a valuable tool for customizing insurance policies to meet individual needs. By understanding how they work, you can ensure that your insurance coverage provides the protection you need.

Endorsements and riders are a valuable tool for customizing insurance policies to meet individual needs. By understanding how they work, you can ensure that your insurance coverage provides the protection you need.

No Comments