Claims Settlement

Claims settlement is a critical function of insurance companies, involving the process of investigating, evaluating, and paying claims submitted by policyholders who have experienced a covered loss. Efficient and fair claims settlement is essential for maintaining customer satisfaction and upholding the insurer's promise to provide financial protection.

I. Basic Objective of Claims Settlement:

-

A. Indemnification:

- Explanation: The primary objective of claims settlement is to indemnify the insured, meaning to restore them to the same financial position they were in before the loss occurred (up to the policy limits).

- Purpose: To provide the financial resources needed to repair or replace damaged property, cover medical expenses, or compensate for other covered losses.

-

B. Fairness and Equity:

- Explanation: The claims settlement process should be fair and equitable to all policyholders, regardless of their background or circumstances.

- Purpose: To ensure that all claims are evaluated and paid in a consistent and unbiased manner.

-

C. Efficiency and Timeliness:

- Explanation: Claims should be settled as quickly and efficiently as possible, minimizing the disruption and inconvenience to the policyholder.

- Purpose: To provide timely financial assistance to help policyholders recover from their losses.

-

D. Cost Control:

- Explanation: Claims should be settled at a reasonable cost, while still providing fair and adequate compensation to the policyholder.

- Purpose: To maintain the insurer's financial stability and keep premiums affordable.

-

E. Compliance:

- Explanation: The claims settlement process must comply with all applicable laws and regulations.

- Purpose: To avoid legal penalties and maintain the insurer's license to operate.

II. Parties Involved in the Claims Settlement Process:

-

A. Insured (Policyholder):

- Role: The insured is the individual or entity who purchased the insurance policy and is entitled to benefits if a covered loss occurs.

-

Responsibilities:

- Providing timely notice of the loss to the insurer.

- Providing accurate and complete information about the loss.

- Cooperating with the insurer's investigation of the claim.

- Protecting the damaged property from further loss.

-

B. Insurer (Claims Adjuster):

- Role: The insurer is the insurance company that issued the policy and is responsible for investigating, evaluating, and paying claims. The claims adjuster is the individual who handles the claim on behalf of the insurer.

-

Responsibilities:

- Investigating the claim to determine whether it is covered by the policy.

- Evaluating the amount of the loss.

- Negotiating a settlement with the insured.

- Paying the claim in a timely and efficient manner.

-

C. Independent Adjusters:

- Role: Independent adjusters are hired by the insurer on a contract basis to handle claims.

- Use: Often used for complex or large claims, or when the insurer does not have a claims adjuster in the area.

-

D. Public Adjusters:

- Role: Public adjusters are hired by the insured to represent them in the claims process.

- Use: Can be helpful for insureds who are unfamiliar with the claims process or who feel that the insurer is not treating them fairly.

-

E. Appraisers and Arbitrators:

- Role: Appraisers and arbitrators are independent experts who are hired to resolve disputes about the value of a loss or the terms of coverage.

- Use: Appraisers are used to determine the value of damaged property. Arbitrators are used to resolve other types of disputes.

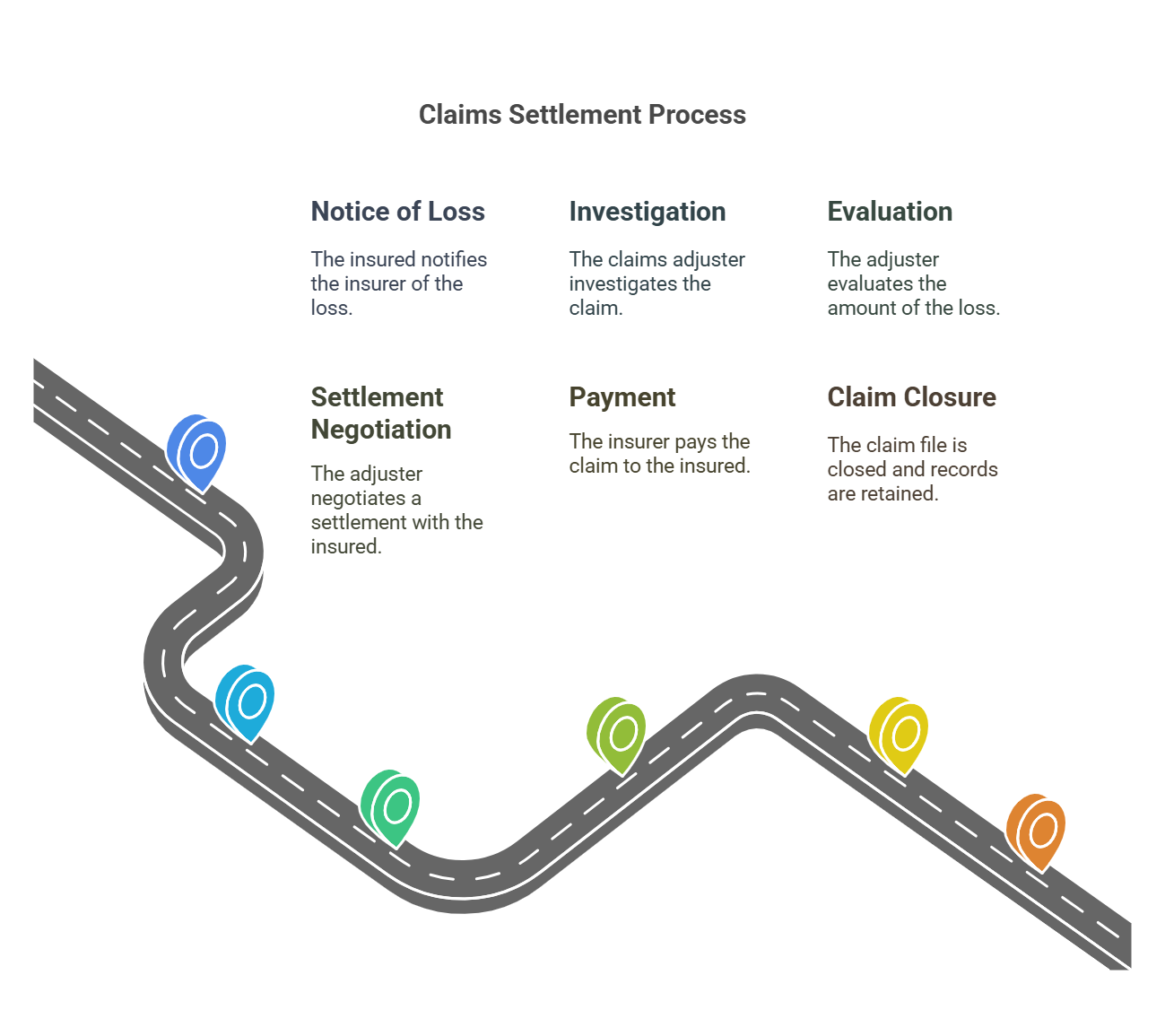

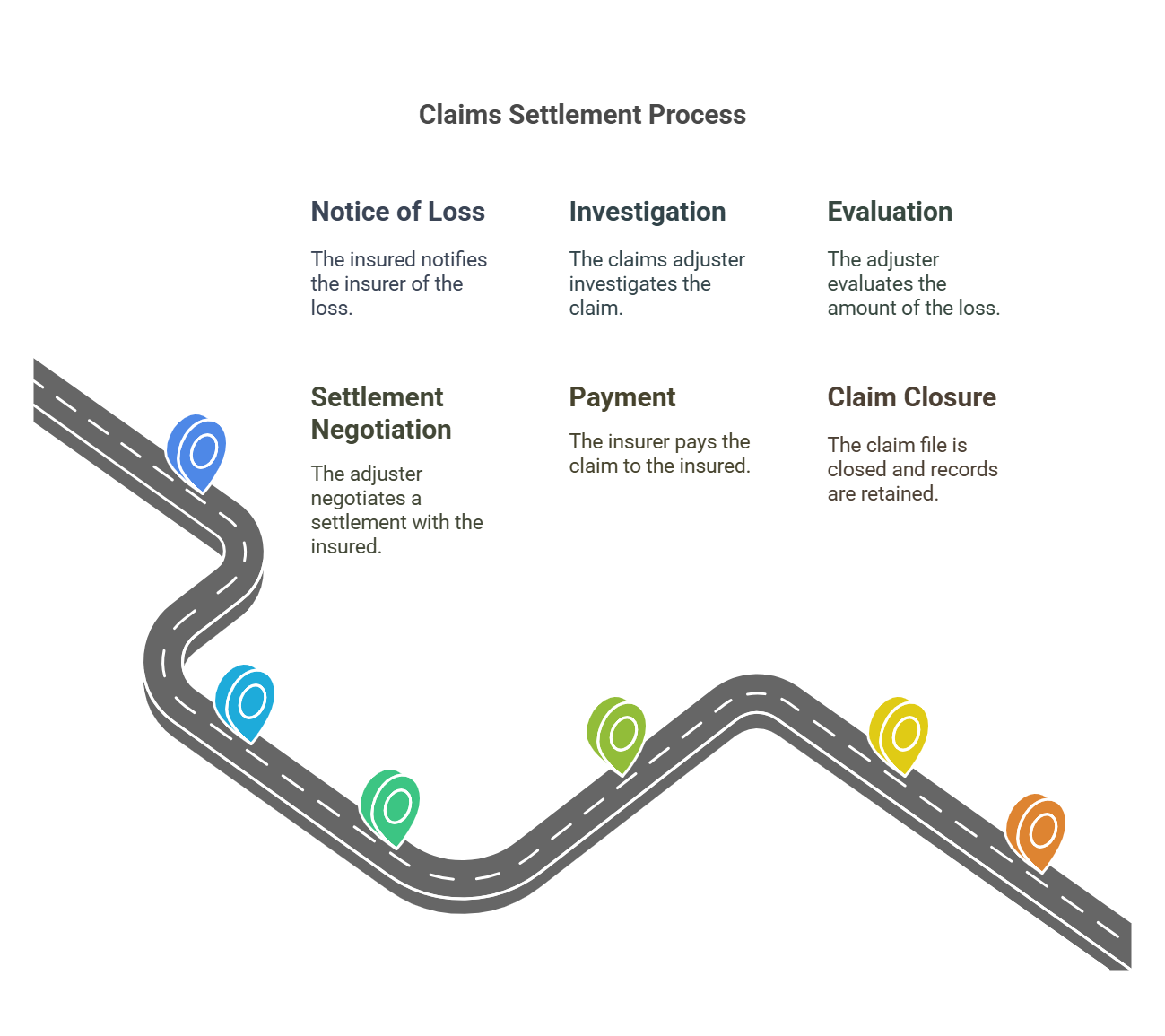

III. Steps in the Claims Settlement Process:

-

1. Notice of Loss:

- Description: The insured must notify the insurer of the loss as soon as reasonably possible.

- Action: The insurer acknowledges receipt of the notice and assigns a claims adjuster to the case.

-

2. Investigation:

- Description: The claims adjuster investigates the claim to determine whether it is covered by the policy.

-

Activities:

- Reviewing the policy

- Interviewing the insured and witnesses

- Inspecting the damaged property

- Obtaining police reports or other relevant documents

-

3. Evaluation:

- Description: The claims adjuster evaluates the amount of the loss.

-

Activities:

- Obtaining estimates for repairs or replacement

- Determining the actual cash value (ACV) of the damaged property

- Calculating the amount of coverage available under the policy

-

4. Settlement:

- Description: The claims adjuster negotiates a settlement with the insured.

-

Options:

- Agreement: The insured and the insurer agree on the amount of the loss and the terms of settlement.

- Disagreement: The insured and the insurer disagree on the amount of the loss or the terms of settlement. In this case, the dispute may be resolved through appraisal, arbitration, or litigation.

-

5. Payment:

- Description: Once a settlement is reached, the insurer pays the claim to the insured.

-

Methods:

- Check

- Electronic funds transfer (EFT)

-

6. Claim Closure:

- Description: Once the claim is paid, the claims file is closed.

-

Action: The insurer retains records of the claim for future reference.

The claims settlement process is a critical part of the insurance relationship. By handling claims fairly, efficiently, and in compliance with all applicable laws and regulations, insurers can build trust with their policyholders and maintain a positive reputation.

The claims settlement process is a critical part of the insurance relationship. By handling claims fairly, efficiently, and in compliance with all applicable laws and regulations, insurers can build trust with their policyholders and maintain a positive reputation.

No Comments