Coinsurance – Nature, Purpose, and Problems

Coinsurance is a provision commonly found in property insurance policies that encourages policyholders to insure their property to a specified percentage of its value. It involves a sharing of losses between the insurer and the insured if the insured fails to meet the coinsurance requirement.

I. Nature of Coinsurance:

-

A. Definition:

- Description: Coinsurance is a policy provision that requires the insured to carry insurance equal to a specified percentage of the property's value in order to receive full payment for a loss. If the insured fails to meet this requirement, they will be penalized at the time of a loss.

- Common Percentages: Common coinsurance percentages are 80%, 90%, and 100%.

-

B. Coinsurance Formula:

- Formula: (Amount of Insurance Carried / Amount of Insurance Required) * Loss = Amount of Recovery

- If: Amount of Insurance Carried >= Amount of Insurance Required, then the insured recovers the full loss, up to the policy limits.

- If: Amount of Insurance Carried < Amount of Insurance Required, then the insured recovers a proportion of the loss, as calculated by the formula.

II. Purpose of Coinsurance:

-

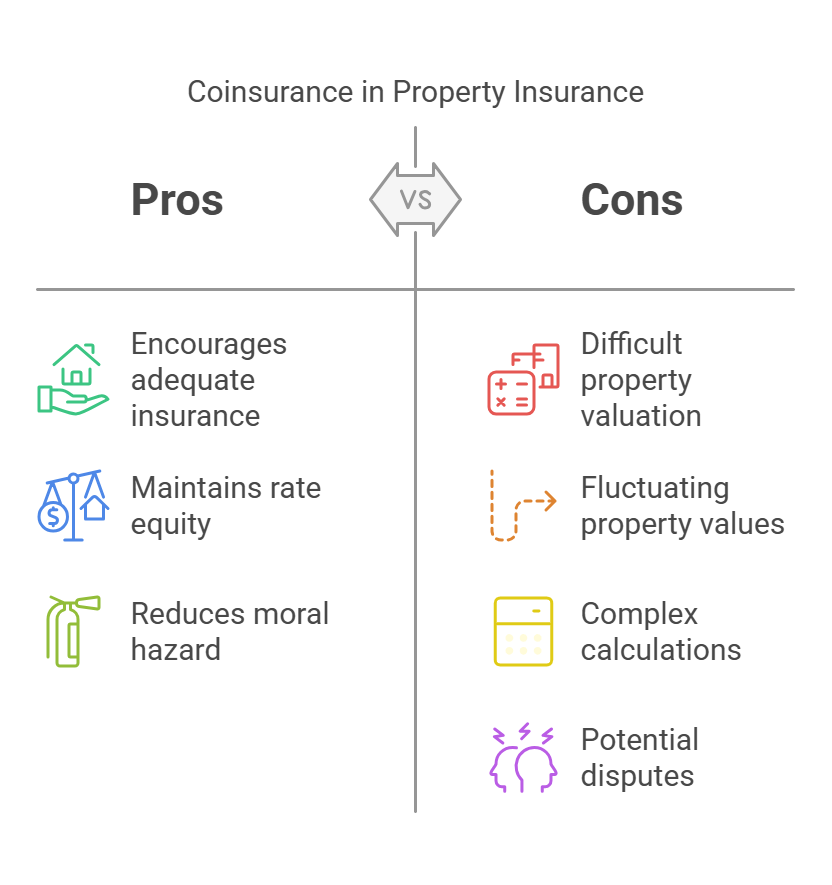

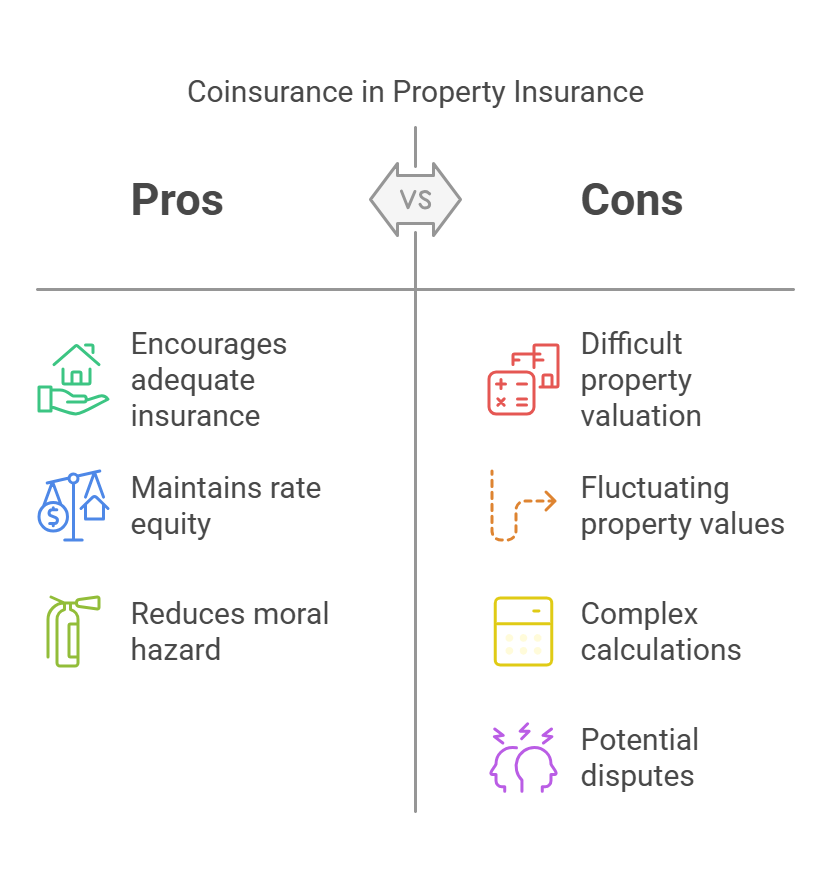

A. Encourage Adequate Insurance:

- Explanation: The primary purpose of coinsurance is to encourage policyholders to insure their property to its full value, or at least to a specified percentage of its value.

- Reasoning: Insurers want policyholders to carry adequate insurance to protect themselves against large losses and to ensure that the insurer has sufficient premium income to cover its potential liabilities.

-

B. Rate Equity:

- Explanation: Coinsurance helps to maintain rate equity among policyholders.

- Reasoning: Policyholders who insure their property to its full value are paying a premium that is commensurate with the risk they are transferring to the insurer. Policyholders who underinsure their property are not paying a fair premium.

-

C. Reduce Moral Hazard:

- Explanation: Coinsurance can help to reduce moral hazard by giving policyholders a financial stake in preventing losses.

- Reasoning: Policyholders who are adequately insured are more likely to take steps to protect their property from damage or loss because they will bear a portion of any loss that occurs.

III. Problems with Coinsurance:

-

A. Difficulty in Determining Property Value:

- Explanation: It can be difficult for policyholders to accurately determine the value of their property, particularly in times of fluctuating market conditions.

- Challenge: If the policyholder underestimates the value of their property, they may be subject to a coinsurance penalty even if they believe they are adequately insured.

-

B. Fluctuating Property Values:

- Explanation: Property values can fluctuate over time due to inflation, depreciation, or changes in market conditions.

- Challenge: Policyholders need to regularly review their insurance coverage and adjust it to reflect changes in property value.

-

C. Complex Calculations:

- Explanation: The coinsurance formula can be confusing for policyholders, particularly when dealing with partial losses.

- Challenge: Policyholders may not understand how the coinsurance provision will affect their claim settlement.

-

D. Potential for Disputes:

- Explanation: Disagreements can arise between the insurer and the insured regarding the value of the property, the amount of the loss, or the application of the coinsurance formula.

- Challenge: These disputes can lead to delays in claim settlement and can damage the relationship between the insurer and the insured.

IV. Example:

-

Scenario: A building is insured for $400,000 and has an actual cash value of $500,000. The policy contains an 80% coinsurance clause. A fire causes $100,000 in damage.

-

Coinsurance Requirement: 0.80 * $500,000 = $400,000

-

Analysis: The insured met the coinsurance requirement. Therefore, the full loss of $100,000 is covered, subject to any deductible.

-

Scenario: Same as above, but the building is insured for only $300,000.

-

Coinsurance Requirement: 0.80 * $500,000 = $400,000

-

Analysis: The insured did not meet the coinsurance requirement.

-

Calculation: ($300,000 / $400,000) * $100,000 = $75,000. The insurer will pay $75,000, and the insured will bear the remaining $25,000 of the loss.

To avoid coinsurance penalties, policyholders should carefully determine the value of their property and ensure that they carry insurance coverage equal to at least the specified coinsurance percentage. Regular review of coverage is also essential.

To avoid coinsurance penalties, policyholders should carefully determine the value of their property and ensure that they carry insurance coverage equal to at least the specified coinsurance percentage. Regular review of coverage is also essential.

No Comments