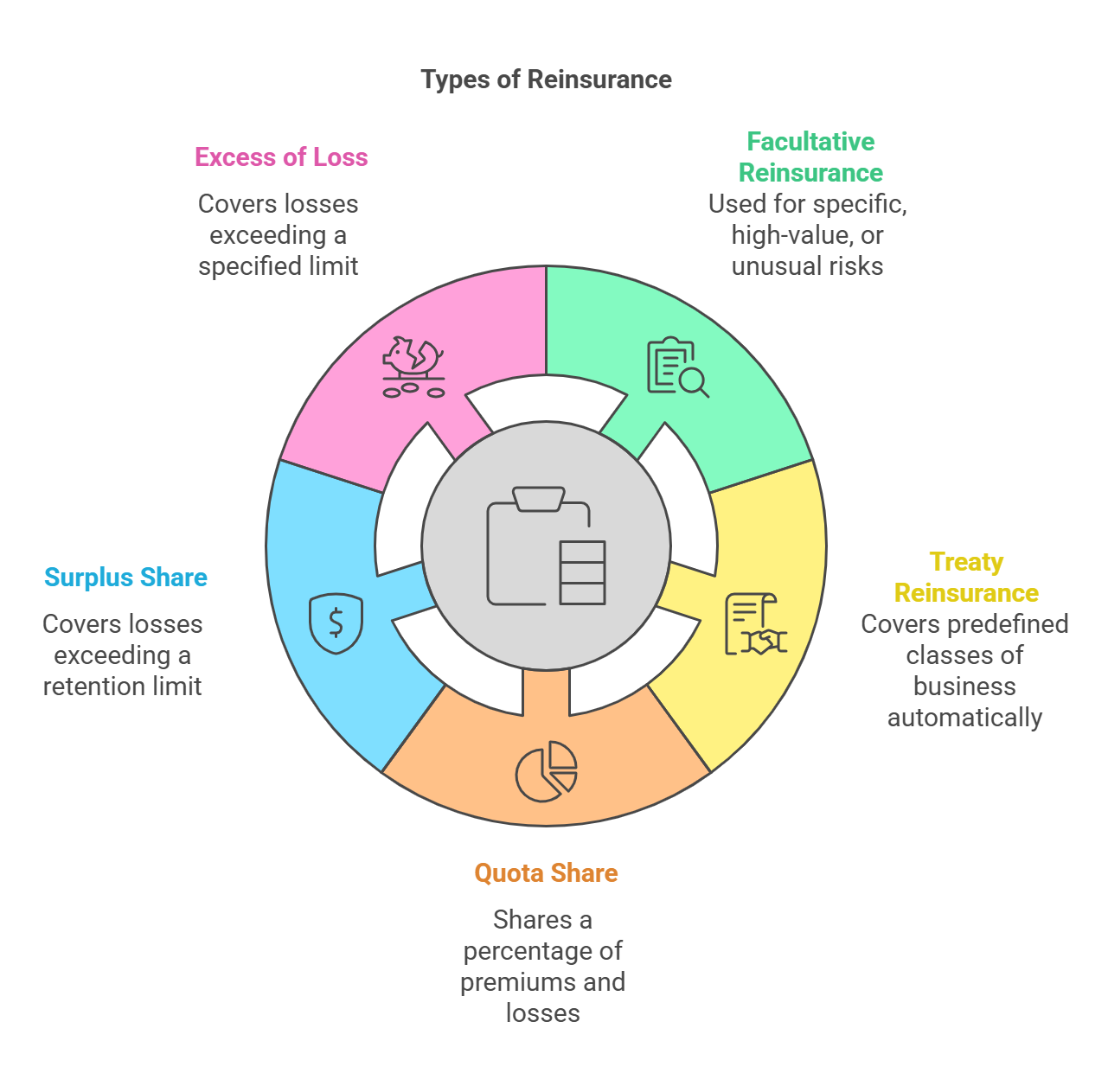

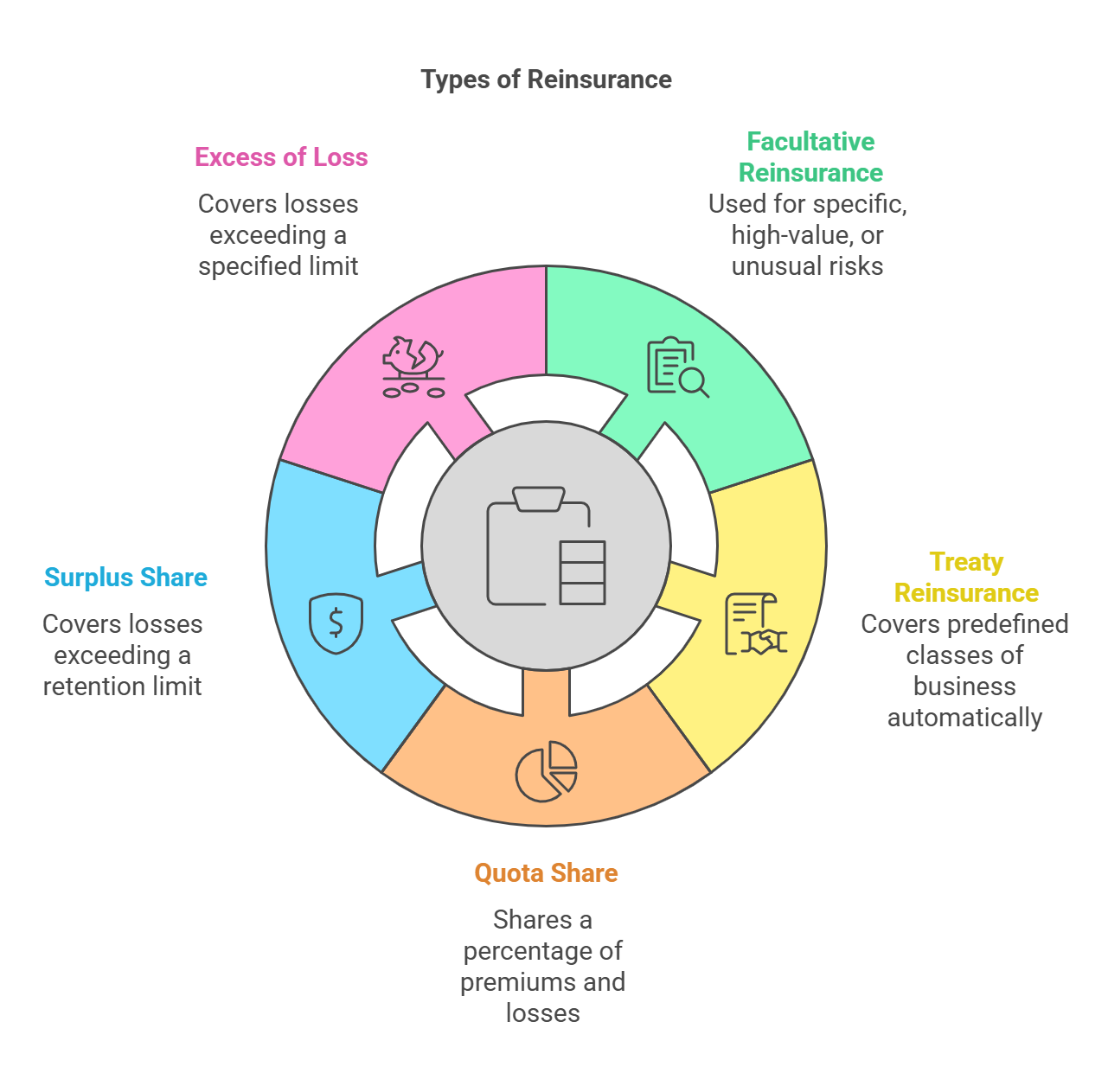

Types of Reinsurance

Reinsurance agreements can be broadly classified into two main types: facultative reinsurance and treaty reinsurance. These types differ in terms of the risk selection process and the scope of coverage.

I. Facultative Reinsurance:

-

A. Definition:

- Description: Facultative reinsurance is a type of reinsurance where each individual risk that the ceding company seeks to reinsure is offered to the reinsurer, and the reinsurer has the option (faculty) to accept or reject the risk.

- Nature: Risk-specific and negotiated on a case-by-case basis.

-

B. Key Characteristics:

- Individual Risk Assessment: Each risk is individually underwritten by the reinsurer.

- Optional: The ceding company is not obligated to cede the risk, and the reinsurer is not obligated to accept it.

- Specific Terms: The terms of the reinsurance agreement are specific to the individual risk.

- Time-Consuming: Facultative reinsurance is more time-consuming and expensive to administer than treaty reinsurance.

-

C. Use Cases:

- High-Value or Unusual Risks: Used for risks that are outside the ceding company's normal underwriting guidelines or that are particularly large or complex.

- Limited Capacity: Used when the ceding company has limited capacity to retain the risk itself.

- New Lines of Business: Used when the ceding company is entering a new line of business and wants to obtain reinsurance coverage for the initial risks.

II. Treaty Reinsurance:

-

A. Definition:

- Description: Treaty reinsurance is a type of reinsurance where the ceding company agrees to cede, and the reinsurer agrees to accept, all risks of a certain type that fall within the terms of the reinsurance agreement (the treaty).

- Nature: A pre-arranged agreement covering a defined class of business.

-

B. Key Characteristics:

- Automatic Coverage: All risks that fall within the treaty are automatically covered.

- Predetermined Terms: The terms of the reinsurance agreement are predetermined and apply to all risks covered by the treaty.

- Efficient: Treaty reinsurance is more efficient and less expensive to administer than facultative reinsurance.

-

C. Types of Treaty Reinsurance:

-

1. Proportional (Quota Share and Surplus):

- Description: The reinsurer shares a predetermined percentage of the ceding company's premiums and losses.

- Quota Share: The reinsurer covers an agreed-upon percentage of every policy that falls within the treaty.

- Surplus Share: The ceding company sets a retention limit, and the reinsurer covers the portion of any policy that exceeds that limit, up to a maximum amount.

-

2. Non-Proportional (Excess of Loss):

- Description: The reinsurer covers losses that exceed a specified retention limit.

- Excess of Loss: The reinsurer pays for losses that exceed the ceding company's retention, up to a maximum limit. This can be on a per-occurrence basis or an aggregate basis.

-

Methods of Sharing Losses (Numerical Examples)

Here are some numerical examples to illustrate how losses are shared under different types of reinsurance agreements.

Example 1: Quota Share Reinsurance

- Scenario: An insurance company has a quota share treaty with a reinsurer where the reinsurer covers 60% of all policies. The insurer issues a policy with a $1,000,000 limit and receives a $10,000 premium. A $400,000 loss occurs.

- Premium Sharing: Reinsurer receives 60% of $10,000 = $6,000. Ceding company retains $4,000.

- Loss Sharing: Reinsurer pays 60% of $400,000 = $240,000. Ceding company pays $160,000.

Example 2: Surplus Share Reinsurance

- Scenario: An insurance company has a surplus share treaty with a reinsurer. The ceding company's retention limit is $200,000 per policy, and the treaty limit is $800,000. The insurer issues a policy with a $1,000,000 limit and receives a $10,000 premium. A $400,000 loss occurs.

- Capacity: Treaty capacity = $800,000 / ($1,000,000-$200,000) = 4 lines. The ceding company retains one line and the reinsurer covers 4 lines. Premium is therefore shared 1/5 and 4/5.

- Premium Sharing: Reinsurer receives 4/5 of $10,000 = $8,000. Ceding company retains $2,000.

- Loss Sharing: The reinsurer covers the loss above the ceding company's retention i.e. $400,000 - $200,000 = $200,000. Ceding company and reinsurer both pay $200,000.

Example 3: Excess of Loss Reinsurance (Per Occurrence)

- Scenario: An insurance company has an excess of loss treaty with a reinsurer where the reinsurer covers losses exceeding $500,000 up to a limit of $5,000,000 per occurrence. A $2,000,000 loss occurs.

- Loss Sharing: Ceding company pays the first $500,000 (the retention). Reinsurer pays the remaining $1,500,000 ($2,000,000 - $500,000).

Example 4: Excess of Loss Reinsurance (Aggregate)

- Scenario: An insurance company has an aggregate excess of loss treaty where the reinsurer covers aggregate losses exceeding $10,000,000 up to a limit of $20,000,000 during the year. The ceding company's aggregate losses for the year total $25,000,000.

-

Loss Sharing: Ceding company pays the first $10,000,000. Reinsurer pays $15,000,000 ($25,000,000 - $10,000,000).

These examples illustrate the basic principles of loss sharing under different types of reinsurance agreements. The specific terms and conditions of each agreement will vary depending on the needs of the ceding company and the reinsurer.

These examples illustrate the basic principles of loss sharing under different types of reinsurance agreements. The specific terms and conditions of each agreement will vary depending on the needs of the ceding company and the reinsurer.

No Comments