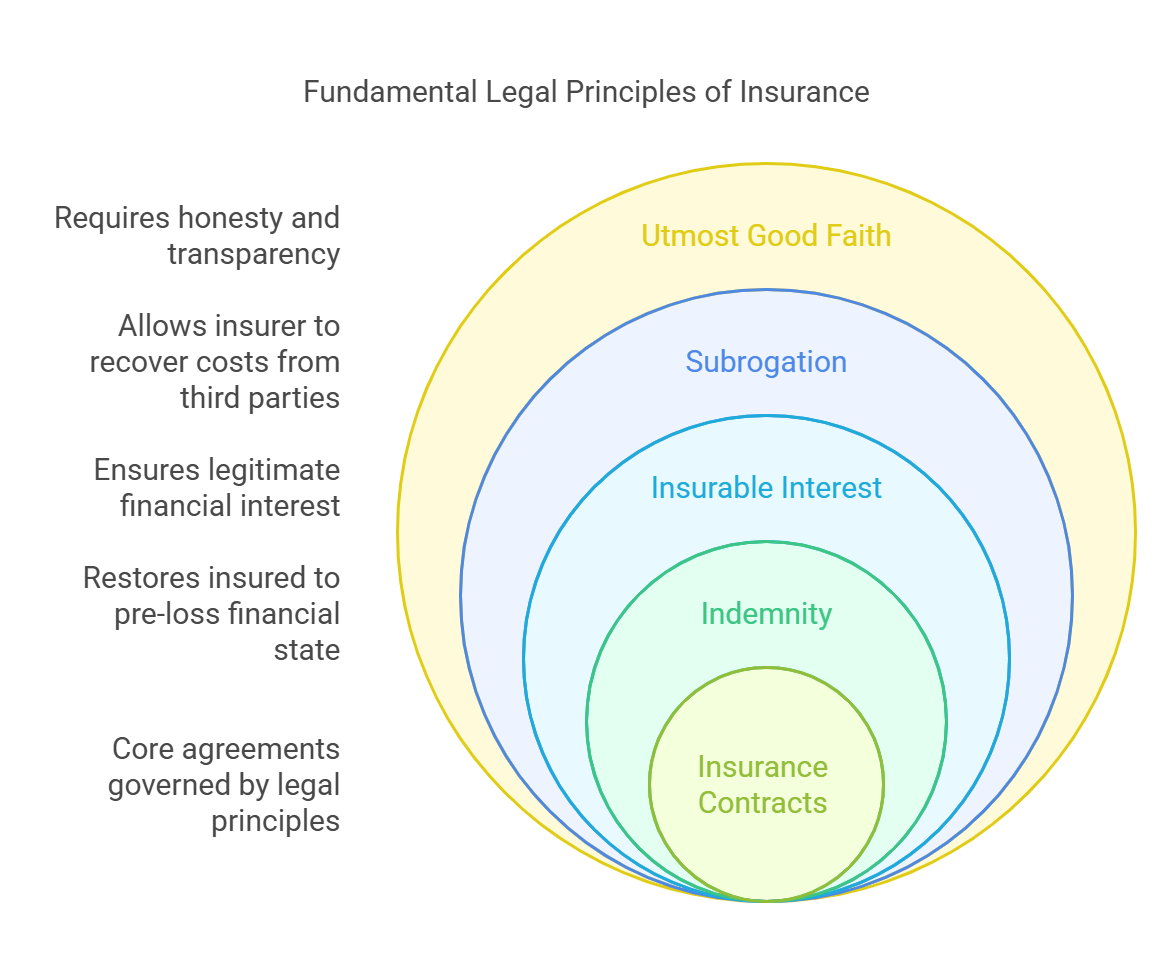

Fundamental Legal Principles of Insurance

Insurance contracts are governed by several fundamental legal principles that ensure fairness and enforceability. These principles shape the nature of the insurance agreement and the rights and obligations of both the insurer and the insured.

I. Principle of Indemnity:

I. Principle of Indemnity:

- Definition: The principle of indemnity states that the purpose of insurance is to restore the insured to the same financial position they were in before the loss occurred. The insured should not profit from a loss; they should only be compensated for the actual amount of their loss, up to the policy limits.

- Purpose: To prevent the insured from making a profit from an insured event.

-

How it Works:

- Actual Cash Value (ACV): Many property insurance policies pay based on the actual cash value of the damaged property, which is the replacement cost less depreciation.

- Replacement Cost Coverage: Some policies provide replacement cost coverage, which pays for the full cost of replacing the damaged property with new property of like kind and quality, without deduction for depreciation (often requiring the property to actually be replaced).

- Valued Policies: In some cases, the insurer and insured agree on the value of the insured item in advance (e.g., for valuable artwork). The insurer pays this agreed-upon value in the event of a covered loss.

-

Exceptions:

- Life Insurance: Life insurance is not strictly a contract of indemnity because human life cannot be precisely valued. The insurer pays a predetermined death benefit to the beneficiary upon the insured's death.

- Valued Policies: As mentioned above, these policies pay a pre-agreed amount.

II. Principle of Insurable Interest:

- Definition: The principle of insurable interest requires that the insured must have a legitimate financial interest in the subject matter of the insurance. This means that the insured must stand to suffer a financial loss if the insured event occurs.

- Purpose: To prevent gambling on losses and to reduce moral hazard (the incentive to cause a loss for financial gain).

-

Requirements:

- Financial Interest: The insured must stand to suffer a financial loss if the insured event occurs.

- Legitimate Interest: The interest must be lawful and not against public policy.

-

Examples:

- Property Insurance: A homeowner has an insurable interest in their home.

- Life Insurance: An individual has an insurable interest in their own life, and spouses typically have an insurable interest in each other's lives. A business partner may have an insurable interest in the life of another partner.

-

Timing:

- Life Insurance: Insurable interest must exist at the time the policy is purchased.

- Property Insurance: Insurable interest must exist at the time of the loss.

III. Principle of Subrogation:

- Definition: The principle of subrogation states that after an insurer has paid a claim to the insured, the insurer has the right to step into the shoes of the insured and pursue any legal remedies that the insured may have against a third party who caused the loss.

- Purpose: To prevent the insured from collecting twice for the same loss (once from the insurer and once from the responsible party) and to hold the responsible party accountable for their actions.

-

How it Works:

- The insurer pays the insured for the loss.

- The insured assigns their right to sue the responsible party to the insurer.

- The insurer then pursues legal action against the responsible party to recover the amount they paid to the insured.

- Example: If a driver is at fault in a car accident and damages another person's car, the at-fault driver's insurance company will pay for the damages to the other person's car. The insurance company then has the right to subrogate against the at-fault driver to recover the amount they paid out.

IV. Principle of Utmost Good Faith (Uberrimae Fidei):

- Definition: The principle of utmost good faith requires both the insurer and the insured to act honestly and disclose all material information relevant to the insurance contract. This principle is based on the idea that insurance contracts are based on trust and that both parties must be transparent in their dealings with each other.

- Purpose: To ensure fairness and honesty in the insurance relationship.

-

Requirements:

- Disclosure: The insured must disclose all material facts that could affect the insurer's decision to issue the policy or the premium charged.

- Honesty: Both parties must act honestly and not misrepresent any facts.

- Consequences of Breach: If either party breaches the duty of utmost good faith, the other party may have the right to void the contract.

-

Examples:

- The insured must accurately disclose their medical history when applying for life insurance.

- The insurer must accurately describe the coverage provided by the policy.

Requirements of an Insurance Contract

For an insurance contract to be legally binding and enforceable, it must meet certain requirements:

-

1. Offer and Acceptance:

- Explanation: There must be a clear offer by one party (the applicant) and an acceptance of that offer by the other party (the insurer).

- Example: The applicant submits an application for insurance, and the insurer approves the application and issues a policy.

-

2. Consideration:

- Explanation: There must be an exchange of something of value between the parties. The insured provides consideration in the form of premium payments, and the insurer provides consideration in the form of a promise to pay benefits if a covered loss occurs.

-

3. Competent Parties:

- Explanation: The parties to the contract must be legally competent to enter into an agreement. This means they must be of legal age, of sound mind, and not under the influence of drugs or alcohol.

-

4. Legal Purpose:

- Explanation: The purpose of the contract must be legal and not against public policy. A contract to insure an illegal activity would not be enforceable.

-

5. Insurable Interest: (already explained above)

-

6. In Writing:

- Explanation: While some contracts can be oral, insurance contracts are generally required to be in writing to be enforceable. This provides clear evidence of the terms of the agreement.

No Comments