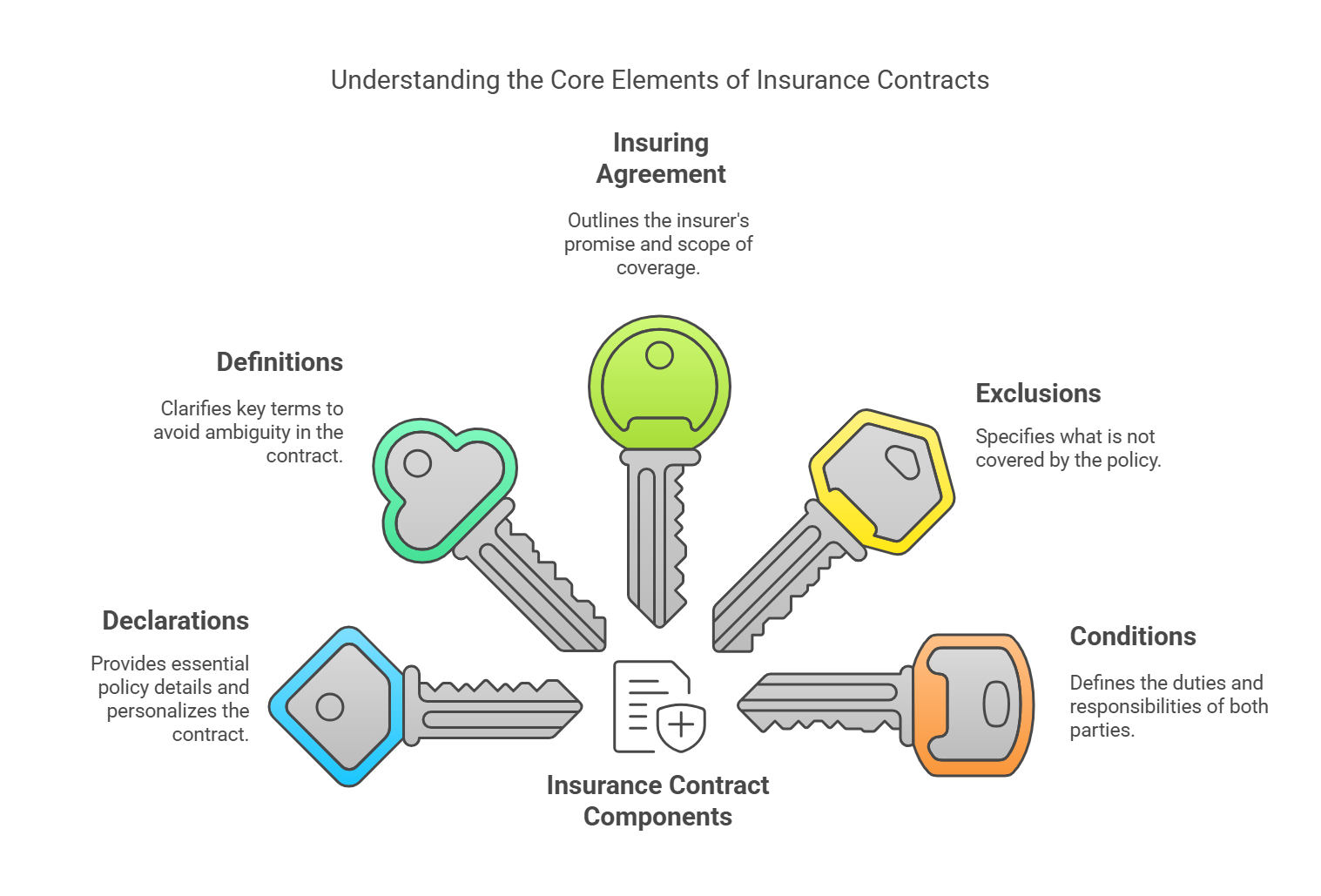

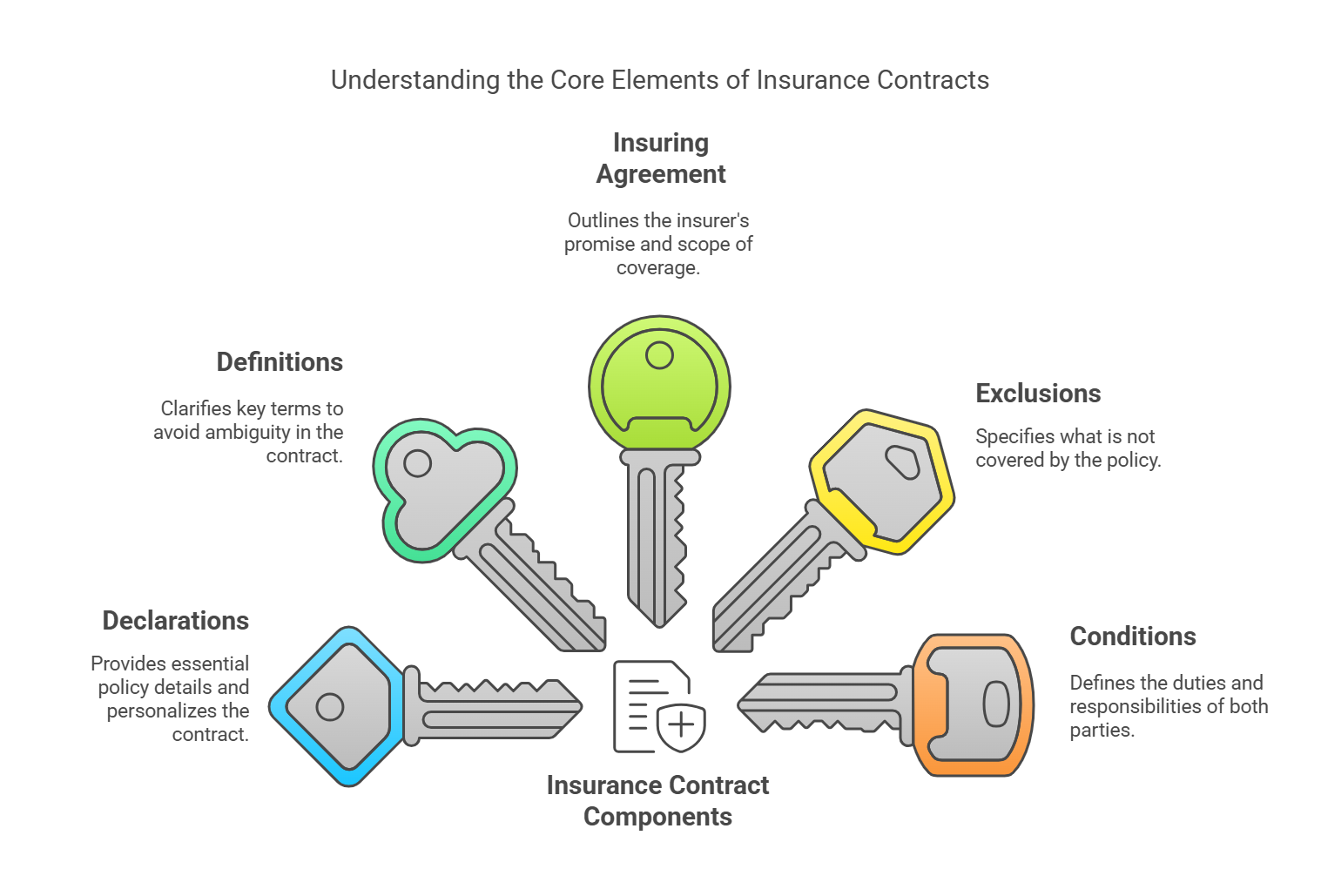

Components of Insurance Contracts

An insurance contract (policy) is a legally binding document that outlines the rights and responsibilities of both the insurer and the insured. It consists of several key components that define the scope and limitations of coverage. Understanding these components is crucial for interpreting the policy and ensuring that it meets your needs.

-

1. Declarations:

- Purpose: Provides basic information about the policy and the insured. It personalizes the policy to the specific insured.

-

Contents:

- Name of the insured

- Address of the insured

- Policy number

- Policy period (effective date and expiration date)

- Description of the insured property or activity

- Policy limits (the maximum amount the insurer will pay for a covered loss)

- Premium amount

- Deductibles (the amount the insured must pay before the insurer pays)

- Endorsements (any modifications or additions to the policy)

- Significance: The declarations page is often the first page of the policy and provides a summary of the key information.

-

2. Definitions:

- Purpose: Clarifies the meaning of key terms used in the policy to avoid ambiguity and ensure that both the insurer and the insured understand the contract.

-

Contents:

- Definitions of terms such as "insured," "property," "occurrence," "accident," "bodily injury," "property damage," and other relevant terms.

- Significance: Carefully reviewing the definitions section is essential for understanding the scope of coverage. Broad or narrow definitions can significantly impact whether a claim is covered.

-

3. Insuring Agreement:

- Purpose: Outlines the insurer's promise to pay benefits if a covered loss occurs. It describes the scope of coverage and the perils that are covered.

-

Types:

- Named-Peril Coverage: Covers only those perils that are specifically listed in the policy. If a peril is not listed, it is not covered.

- All-Risk (Open-Peril) Coverage: Covers all perils except those that are specifically excluded. This provides broader coverage than named-peril coverage.

- Significance: The insuring agreement is the heart of the policy, as it defines what the insurer is agreeing to cover.

-

4. Exclusions:

- Purpose: Specifies the perils, property, or circumstances that are not covered by the policy.

-

Common Exclusions:

- Intentional acts

- War

- Nuclear hazards

- Earthquakes and floods (often covered by separate policies)

- Wear and tear

- Inherent vice

- Pest damage

- Significance: Exclusions narrow the scope of coverage provided by the insuring agreement. It is crucial to understand what is excluded from coverage.

-

5. Conditions:

- Purpose: Sets forth the duties and responsibilities of both the insured and the insurer. They define the rules of the contract.

-

Common Conditions:

- Notice of Loss: The insured must provide timely notice of a loss to the insurer.

- Proof of Loss: The insured must provide documentation to support their claim.

- Cooperation: The insured must cooperate with the insurer's investigation of the claim.

- Other Insurance: Specifies how the policy will interact with other insurance policies covering the same loss.

- Subrogation: Gives the insurer the right to pursue legal remedies against a third party who caused the loss.

- Cancellation: Outlines the conditions under which the insurer or the insured can cancel the policy.

- Misrepresentation and Fraud: States that the policy can be voided if the insured makes material misrepresentations or commits fraud.

- Significance: Failure to comply with the conditions of the policy can result in denial of a claim.

-

6. Miscellaneous Provisions:

- Purpose: Includes various other provisions that do not fit neatly into the other categories.

-

Examples:

- Territorial Restrictions: Specifies the geographic area where coverage applies.

- Policy Assignment: Outlines the conditions under which the policy can be transferred to another party.

- Concealment or Fraud: States that the policy may be voided if the insured has concealed or misrepresented any material fact.

-

Liberalization Clause: Provides that if the insurer broadens coverage without an additional premium, the broadened coverage will automatically apply to existing policies.

s

Understanding each of these components is essential for interpreting an insurance policy and ensuring that it provides the coverage you need. It is always advisable to read the entire policy carefully and to seek clarification from the insurer if you have any questions.

Understanding each of these components is essential for interpreting an insurance policy and ensuring that it provides the coverage you need. It is always advisable to read the entire policy carefully and to seek clarification from the insurer if you have any questions.

No Comments