Regulatory Framework of Insurance in India

The insurance industry in India is governed by a comprehensive regulatory framework designed to protect the interests of policyholders, promote the orderly growth of the industry, and ensure its financial stability. The key components of this framework are the insurance legislation and the Insurance Regulatory and Development Authority of India (IRDAI).

I. Insurance Legislation:

-

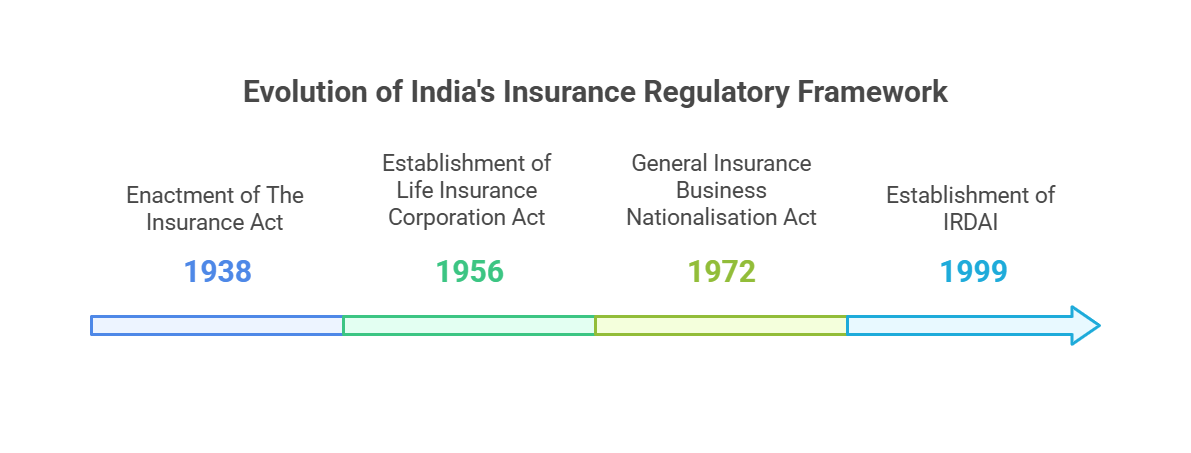

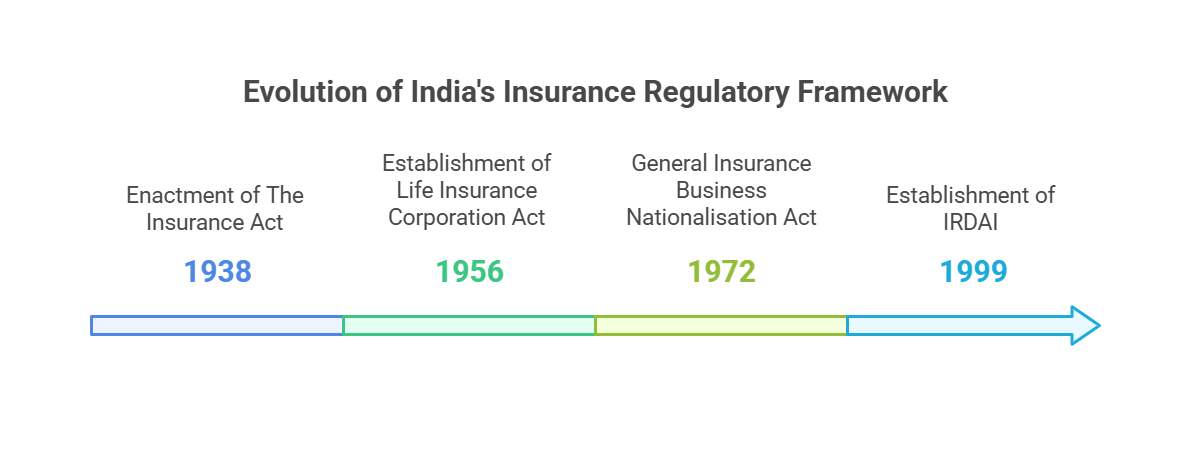

A. The Insurance Act, 1938:

-

Description: This is the primary legislation governing the insurance industry in India. It lays down the basic principles for the conduct of insurance business, including:

- Requirements for registration of insurance companies

- Rules for investment of funds

- Provisions relating to solvency margins

- Regulations for the appointment of agents

- Protection of policyholders' interests

- Significance: Provides the foundational legal framework for the insurance sector.

-

Description: This is the primary legislation governing the insurance industry in India. It lays down the basic principles for the conduct of insurance business, including:

-

B. The Life Insurance Corporation Act, 1956:

- Description: This Act established the Life Insurance Corporation of India (LIC) and nationalized the life insurance business.

- Significance: Historically significant, though the insurance market has since been liberalized.

-

C. The General Insurance Business (Nationalisation) Act, 1972:

- Description: This Act nationalized the general insurance business in India.

- Significance: Similar to the LIC Act, this Act significantly shaped the industry for a long period.

-

D. The IRDA Act, 1999:

- Description: This Act established the Insurance Regulatory and Development Authority (IRDA) as the apex regulatory body for the insurance sector in India.

- Significance: Marked a shift towards liberalization and a more structured regulatory approach.

-

E. Amendments and Updates: The above acts have been amended over time to adapt to changing market conditions and regulatory needs.

II. Insurance Regulatory and Development Authority of India (IRDAI):

-

A. Establishment and Mandate:

- Description: The IRDAI was established as an autonomous statutory body under the IRDA Act, 1999.

- Mandate: To protect the interests of policyholders, to regulate, promote and ensure orderly growth of the insurance industry and for matters connected therewith or incidental thereto.

-

B. Key Functions and Powers:

- Registration and Licensing: Registering and licensing insurance companies, brokers, and agents.

- Regulation and Supervision: Regulating and supervising the operations of insurance companies to ensure their solvency and financial stability.

- Policyholder Protection: Protecting the interests of policyholders by ensuring fair treatment and timely settlement of claims.

- Product Approval: Approving insurance products to ensure that they are fair, transparent, and meet the needs of policyholders.

- Investment Regulations: Regulating the investment of funds by insurance companies to protect policyholder's money.

- Grievance Redressal: Providing a mechanism for resolving disputes between policyholders and insurance companies.

- Promotion of Professionalism: Promoting professionalism and ethical conduct in the insurance industry.

- Setting Solvency Margins: Mandating and monitoring solvency margins to ensure insurers can meet their obligations.

-

C. Key Regulations and Guidelines:

- IRDAI (Registration of Indian Insurance Companies) Regulations: Govern the registration process for new insurance companies.

- IRDAI (Protection of Policyholders' Interests) Regulations: Focus on fair treatment and grievance redressal.

- IRDAI (Investment) Regulations: Dictate how insurers can invest policyholder funds.

- Various Circulars and Guidelines: Issued periodically by IRDAI to provide further clarification and guidance on regulatory matters.

-

D. Objectives of IRDAI:

- Protect the interests of policyholders.

- Promote and ensure the orderly growth of the insurance industry.

- Set high standards of fair dealing and competence in the insurance market.

- Ensure the financial security of insurance companies.

- Bring about speedy and orderly settlement of genuine claims.

-

Manage and supervise resources entrusted to insurance companies effectively.

In summary, the regulatory framework for insurance in India, comprising the Insurance Act and the IRDAI, aims to create a stable, efficient, and customer-centric insurance market that promotes economic growth and provides financial security to individuals and businesses.

In summary, the regulatory framework for insurance in India, comprising the Insurance Act and the IRDAI, aims to create a stable, efficient, and customer-centric insurance market that promotes economic growth and provides financial security to individuals and businesses.

No Comments