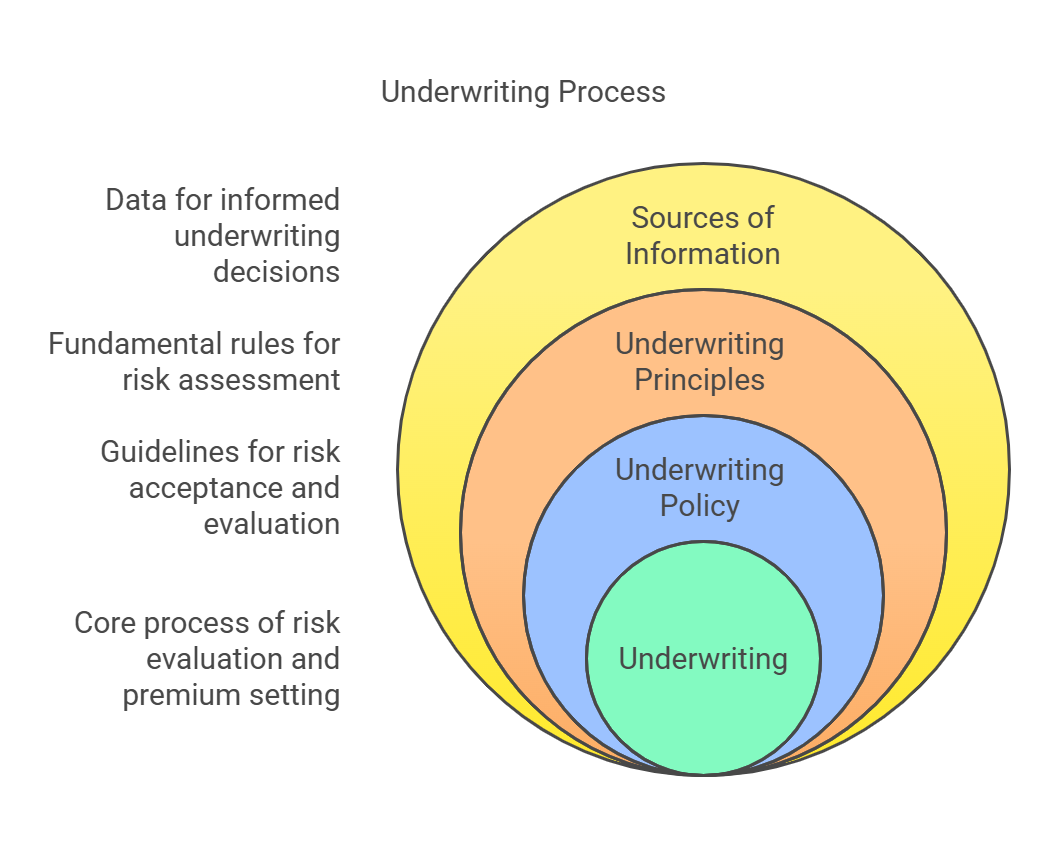

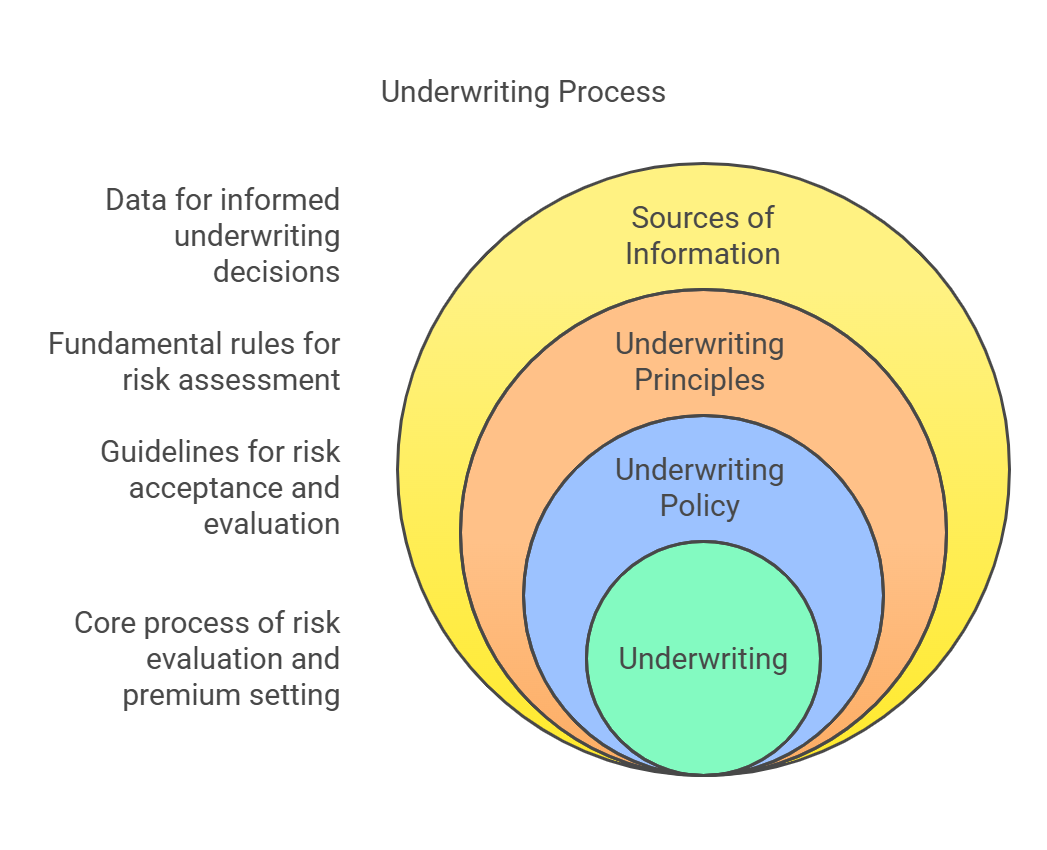

Underwriting

Underwriting is the process by which an insurance company evaluates the risk presented by an applicant and decides whether to offer insurance coverage. If coverage is offered, underwriting also determines the appropriate premium to charge based on the assessed risk. It's a critical function that helps insurers maintain profitability and avoid adverse selection.

- Definition: Underwriting is the process of selecting, classifying, and pricing risks to ensure that the insurance company can meet its financial obligations and maintain profitability.

I. Underwriting Policy:

- Description: An underwriting policy is a set of guidelines that outlines the insurer's risk appetite, acceptable risks, and the procedures that underwriters must follow when evaluating applications. It ensures consistency and fairness in the underwriting process.

-

Key Elements:

- Risk Appetite: Defines the level of risk the insurer is willing to accept.

- Acceptable Risks: Specifies the types of risks the insurer is willing to insure.

- Underwriting Guidelines: Provides detailed instructions on how to evaluate different types of risks.

- Pricing Guidelines: Outlines the factors to consider when determining the appropriate premium.

- Authority Levels: Defines the level of authority that different underwriters have to approve or decline applications.

-

Purpose:

- Ensure Profitability: By carefully selecting and pricing risks, the underwriting policy helps the insurer maintain profitability.

- Maintain Consistency: The underwriting policy ensures that all applications are evaluated consistently, regardless of which underwriter is reviewing them.

- Avoid Adverse Selection: By declining to insure high-risk applicants, the underwriting policy helps the insurer avoid adverse selection (the tendency for people with a higher risk of loss to be more likely to purchase insurance).

- Comply with Regulations: The underwriting policy helps the insurer comply with applicable laws and regulations.

II. Underwriting Principles:

These principles guide the underwriting process and help ensure that the insurer is taking on appropriate risks at appropriate prices.

-

1. Adequate Information:

- Explanation: The underwriter must gather sufficient information about the applicant to accurately assess the risk.

- Implication: Incomplete or inaccurate information can lead to an incorrect assessment of risk and an inappropriate premium.

-

2. Selection of Risks:

- Explanation: The underwriter must carefully select the risks they are willing to insure, based on the insurer's underwriting policy.

- Implication: Accepting too many high-risk applicants can lead to excessive losses.

-

3. Proper Classification:

- Explanation: The underwriter must properly classify the risks they are willing to insure, based on their characteristics and the likelihood of loss.

- Implication: Incorrect classification can lead to underpricing or overpricing of the risk.

-

4. Appropriate Premium:

- Explanation: The underwriter must charge an appropriate premium for the risk, based on its classification and the insurer's pricing guidelines.

- Implication: Charging too low a premium can lead to losses, while charging too high a premium can make the insurer uncompetitive.

-

5. Policy Provisions:

- Explanation: The underwriter must ensure that the policy provisions are clear, unambiguous, and consistent with the insurer's underwriting policy.

- Implication: Ambiguous policy provisions can lead to disputes and litigation.

-

6. Consistent Application:

- Explanation: The underwriter must apply the underwriting policy consistently to all applicants.

- Implication: Inconsistent application can lead to unfair discrimination and legal challenges.

III. Sources of Underwriting Information:

Underwriters rely on a variety of sources to gather information about applicants and assess their risk.

-

1. Application:

- Description: The application is the primary source of information about the applicant. It typically includes questions about the applicant's personal information, medical history, financial status, property characteristics, and other relevant factors.

- Importance: The accuracy and completeness of the application are crucial for the underwriting process.

-

2. Inspection Reports:

- Description: Inspection reports are prepared by independent inspectors who visit the applicant's property or business and assess the risks.

- Use: Common in property insurance to evaluate the condition of the property and identify potential hazards.

-

3. Credit Reports:

- Description: Credit reports provide information about the applicant's credit history, including their payment history, outstanding debts, and credit score.

- Use: Used to assess the applicant's financial stability and their likelihood of paying premiums.

-

4. Medical Examinations and Records:

- Description: Medical examinations and records provide information about the applicant's health status.

- Use: Common in life and health insurance to assess the applicant's risk of illness or death.

-

5. Motor Vehicle Records (MVRs):

- Description: Motor vehicle records provide information about the applicant's driving history, including accidents, traffic violations, and license suspensions.

- Use: Used in auto insurance to assess the applicant's risk of causing an accident.

-

6. Loss History Databases:

- Description: Databases that contain information about past insurance claims.

- Use: Underwriters can use these databases to see if an applicant has a history of filing claims, which may indicate a higher risk of future losses. Examples include the Comprehensive Loss Underwriting Exchange (CLUE) database.

-

7. Government Records:

- Description: Public records maintained by government agencies, such as property tax records, building permits, and court records.

- Use: Can provide information about the applicant's property ownership, legal history, and compliance with regulations.

-

8. Third-Party Data Providers:

- Description: Companies that specialize in collecting and analyzing data for use in underwriting.

-

Use: Can provide information about property characteristics, crime rates, and other factors that may affect risk.

By gathering and analyzing information from these sources, underwriters can make informed decisions about whether to offer insurance coverage and at what premium. This helps insurers manage their risk effectively and maintain profitability.

By gathering and analyzing information from these sources, underwriters can make informed decisions about whether to offer insurance coverage and at what premium. This helps insurers manage their risk effectively and maintain profitability.

No Comments