Insurance and Investments

Insurance companies are significant investors, managing vast portfolios of assets to meet their obligations to policyholders. The investment strategies of life insurance companies differ from those of property and casualty (P&C) insurance companies due to the nature of their liabilities and the time horizons involved.

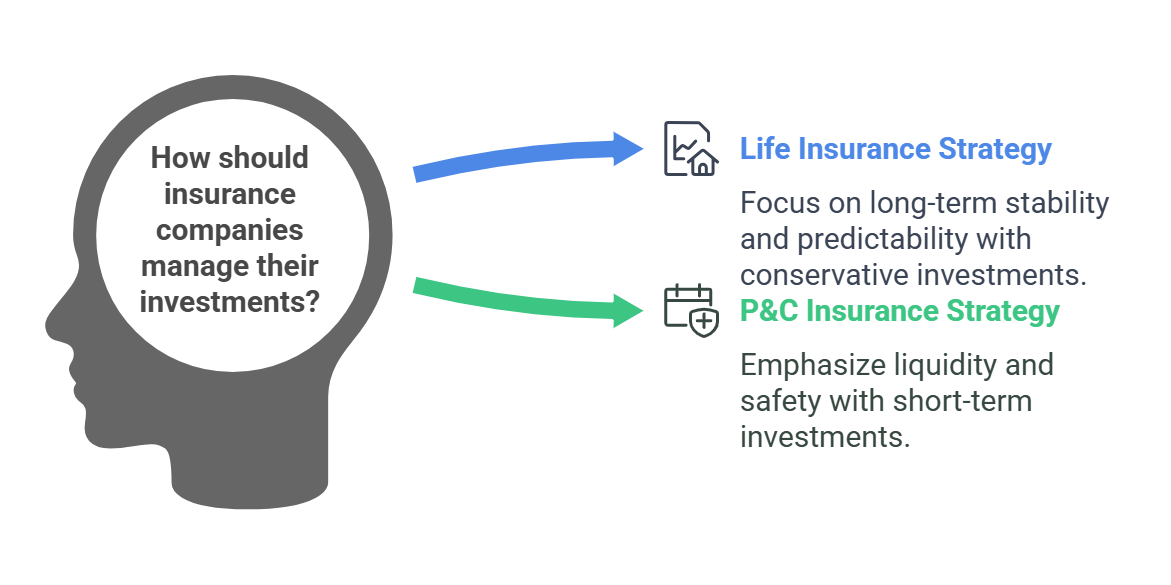

I. Life Insurance Investments:

-

A. Nature of Liabilities:

- Long-Term Liabilities: Life insurance companies have long-term liabilities, as they must pay death benefits or annuity payments over many years.

- Predictable Cash Flows: Life insurance companies can generally predict their cash flows with a reasonable degree of accuracy.

-

B. Investment Objectives:

- Safety and Stability: The primary objective of life insurance investments is to ensure the safety and stability of the company's assets so that it can meet its long-term obligations.

- Adequate Returns: Life insurance companies also seek to generate adequate returns on their investments to meet their policyholder obligations and maintain profitability.

-

C. Investment Strategies:

- Conservative Approach: Life insurance companies typically follow a conservative investment approach, focusing on fixed-income securities.

- Asset-Liability Matching: Life insurance companies carefully match the duration of their assets with the duration of their liabilities to minimize interest rate risk.

- Diversification: Life insurance companies diversify their investments across different asset classes and sectors to reduce risk.

-

D. Common Investment Assets:

- Government Bonds: Considered to be the safest type of investment.

- Corporate Bonds: Provide higher yields than government bonds but also carry more risk.

- Mortgage-Backed Securities (MBS): Provide exposure to the real estate market.

- Real Estate: Can provide diversification and inflation protection.

- Stocks: A smaller portion of the portfolio may be allocated to stocks to enhance returns.

- Private Equity and Alternative Investments: Some life insurers invest in private equity, hedge funds, and other alternative investments to generate higher returns, but these investments are generally subject to stricter regulatory oversight.

II. Property and Casualty Insurance Investments:

-

A. Nature of Liabilities:

- Short-Term Liabilities: P&C insurance companies have shorter-term liabilities, as they must pay claims for property damage, liability claims, and other covered losses.

- Less Predictable Cash Flows: P&C insurance companies' cash flows are less predictable than those of life insurance companies due to the variability of claims.

-

B. Investment Objectives:

- Liquidity: The primary objective of P&C insurance investments is to maintain sufficient liquidity to pay claims promptly.

- Safety: P&C insurance companies also prioritize the safety of their assets.

- Competitive Returns: P&C insurers still need to generate returns, but this is secondary to liquidity and safety.

-

C. Investment Strategies:

- Emphasis on Liquidity: P&C insurance companies invest heavily in liquid assets, such as short-term bonds and cash equivalents.

- Conservative Approach: P&C insurance companies generally follow a conservative investment approach, focusing on fixed-income securities.

- Tax Efficiency: P&C insurers often prioritize tax-efficient investments, such as municipal bonds.

-

D. Common Investment Assets:

- Short-Term Bonds: Provide liquidity and safety.

- Municipal Bonds: Offer tax-exempt income.

- Corporate Bonds: Provide higher yields than government bonds but also carry more risk.

- Mortgage-Backed Securities (MBS): A smaller portion of the portfolio may be allocated to MBS.

- Stocks: A small portion of the portfolio may be allocated to stocks to enhance returns.

- Alternative Investments: P&C insurers typically allocate a smaller percentage of their portfolio to alternative investments compared to life insurers.

III. Regulatory Considerations:

- A. Solvency Requirements: Regulators impose solvency requirements on insurance companies to ensure that they have sufficient assets to meet their obligations to policyholders.

- B. Investment Restrictions: Regulators may restrict the types of investments that insurance companies can make to limit their risk exposure.

- C. Reporting Requirements: Insurance companies are required to report their investment holdings to regulators on a regular basis.

IV. Key Differences:

| Feature | Life Insurance Investments | P&C Insurance Investments |

|---|---|---|

| Liabilities | Long-term, predictable | Short-term, less predictable |

| Investment Objective | Safety, stability, returns | Liquidity, safety, returns |

| Investment Approach | Conservative, asset-liability matching | Conservative, emphasis on liquidity |

| Asset Allocation | Primarily bonds, some stocks and real estate | Primarily short-term bonds and municipal bonds |

Insurance companies play a crucial role in the financial markets as institutional investors. Their investment strategies are shaped by the nature of their liabilities, their investment objectives, and regulatory requirements. By managing their investments prudently, insurance companies can ensure that they are able to meet their obligations to policyholders and contribute to the stability of the financial system.

Insurance companies play a crucial role in the financial markets as institutional investors. Their investment strategies are shaped by the nature of their liabilities, their investment objectives, and regulatory requirements. By managing their investments prudently, insurance companies can ensure that they are able to meet their obligations to policyholders and contribute to the stability of the financial system.

No Comments