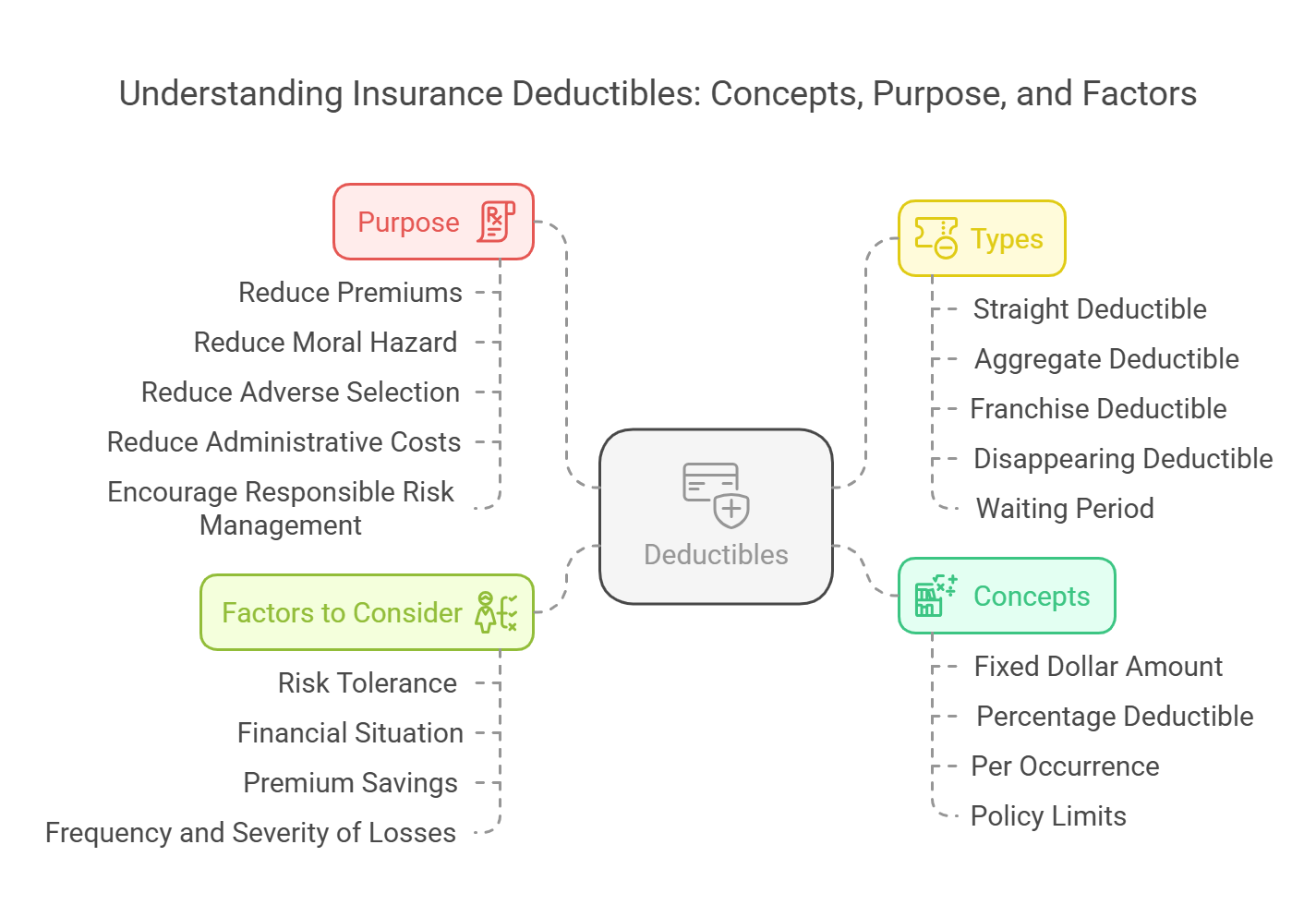

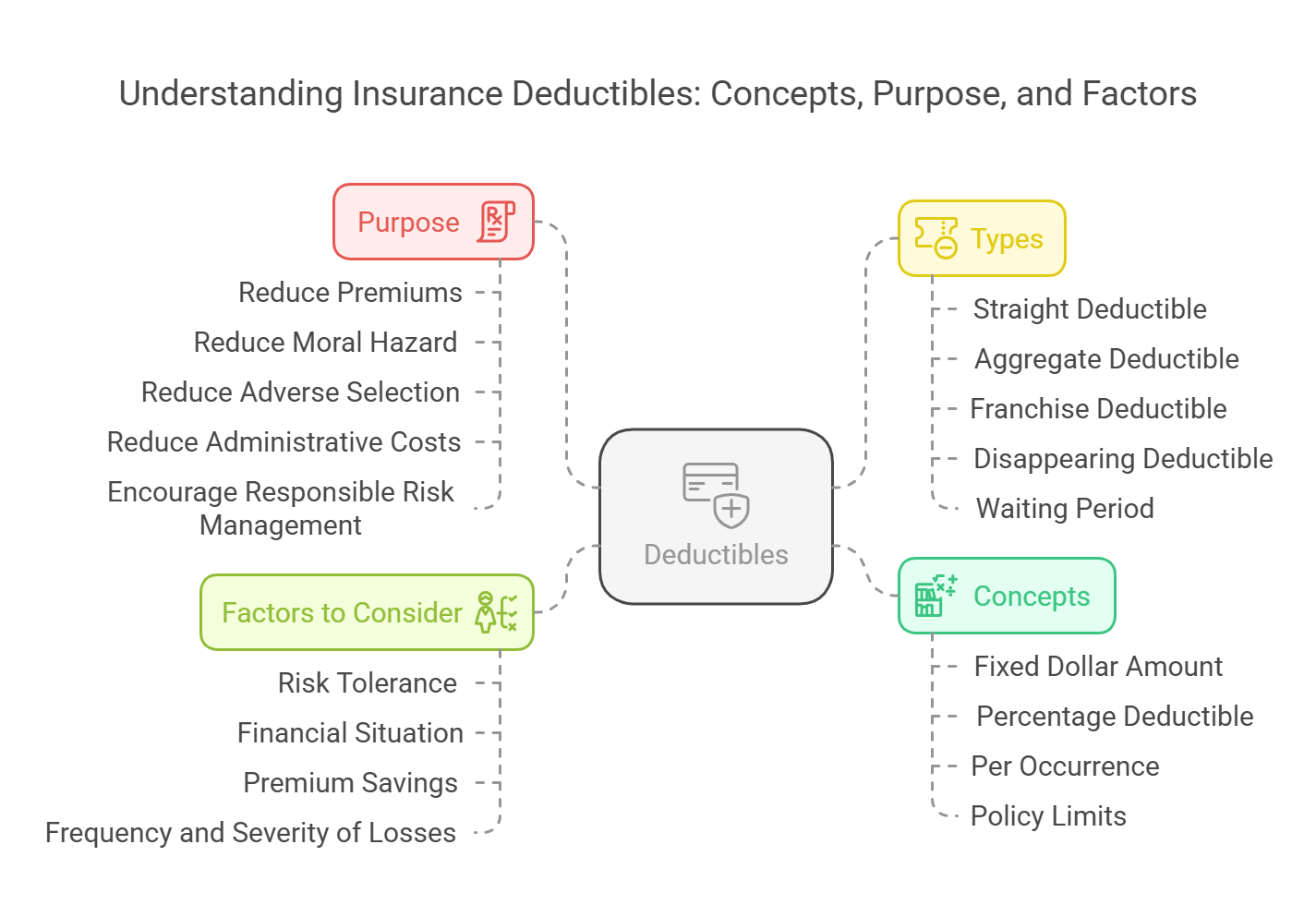

Deductibles – Concepts and Purpose

A deductible is a specified dollar amount that the insured must pay out-of-pocket before the insurance company will pay for a covered loss. Deductibles are a common feature of many types of insurance policies, including property, auto, and health insurance.

- Definition: A deductible is the portion of a covered loss that the insured is responsible for paying. The insurer pays only the amount of the loss that exceeds the deductible.

I. Concepts of Deductibles:

- A. Fixed Dollar Amount: The deductible is typically a fixed dollar amount, such as $250, $500, or $1,000.

- B. Percentage Deductible: In some cases, the deductible may be expressed as a percentage of the insured value or the loss amount.

- C. Per Occurrence: The deductible typically applies to each separate occurrence or loss.

- D. Policy Limits: The deductible does not reduce the policy limits. The insurer will still pay up to the policy limits for a covered loss, after the deductible has been satisfied.

II. Purpose of Deductibles:

III. Types of Deductibles:

- A. Straight Deductible: The insured pays a fixed dollar amount for each loss.

- B. Aggregate Deductible: The insured pays for all losses during the policy period until the aggregate deductible is met. After the aggregate deductible is met, the insurer pays for all remaining covered losses.

- C. Franchise Deductible: If the loss exceeds a specified amount, the deductible is waived, and the insurer pays the entire loss.

- D. Disappearing Deductible: The deductible decreases as the amount of the loss increases.

- E. Waiting Period (in Disability Insurance): Similar to a deductible, the waiting period is the time that must pass after the onset of a disability before benefits are payable.

IV. Factors to Consider When Choosing a Deductible:

-

A. Risk Tolerance:

- Explanation: Individuals with a higher risk tolerance may be willing to accept a higher deductible to save on premiums.

- Consideration: Those who are more risk-averse may prefer a lower deductible for greater financial protection.

-

B. Financial Situation:

- Explanation: Individuals with a strong financial cushion may be able to afford a higher deductible.

- Consideration: Those with limited financial resources may prefer a lower deductible to avoid large out-of-pocket expenses.

-

C. Premium Savings:

- Explanation: The amount of premium savings associated with a higher deductible should be weighed against the potential out-of-pocket expenses.

- Consideration: It's important to determine whether the premium savings are worth the increased risk.

-

D. Frequency and Severity of Losses:

- Explanation: Individuals who are likely to experience frequent but small losses may prefer a lower deductible.

-

Consideration: Those who are likely to experience infrequent but large losses may be willing to accept a higher deductible.

Deductibles play an important role in insurance by reducing premiums, controlling costs, and encouraging responsible risk management. When choosing a deductible, it is important to consider your individual circumstances and weigh the potential benefits and drawbacks.

Deductibles play an important role in insurance by reducing premiums, controlling costs, and encouraging responsible risk management. When choosing a deductible, it is important to consider your individual circumstances and weigh the potential benefits and drawbacks.

No Comments