Personal Risk Management

Personal risk management involves identifying, assessing, and managing the risks that individuals and families face. The goal is to protect personal assets, income, and well-being from potential losses. It’s similar to business risk management, but focuses on the specific risks faced by individuals and families.

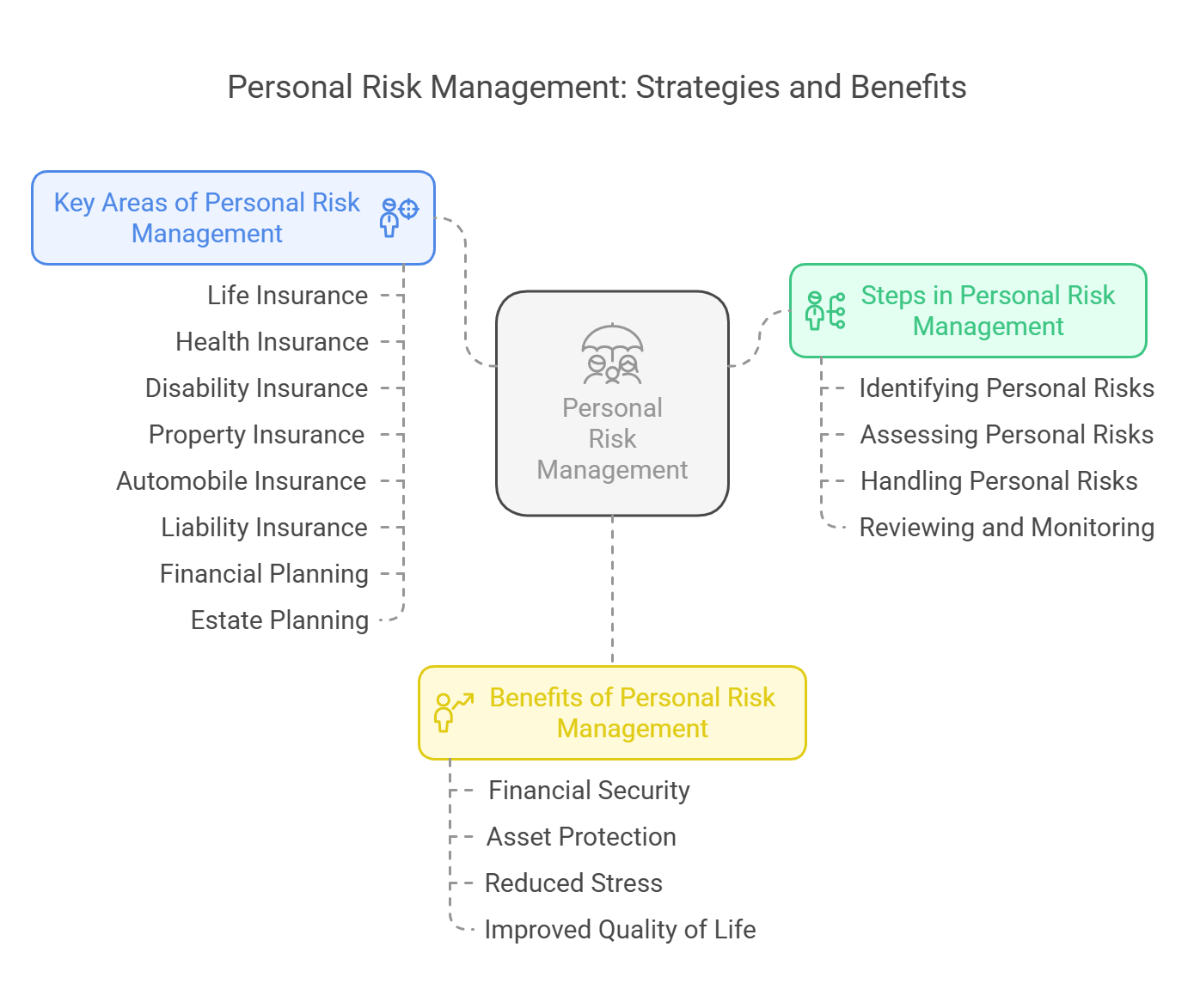

I. Steps in Personal Risk Management:

-

A. Identifying Personal Risks:

-

Description: Identifying potential risks that could lead to financial losses, such as:

- Premature death

- Disability

- Illness

- Property damage (e.g., home, car)

- Liability claims

- Job loss

- Identity theft

-

Techniques:

- Reviewing personal finances and assets

- Considering potential threats to health and safety

- Identifying potential sources of liability

-

Description: Identifying potential risks that could lead to financial losses, such as:

-

B. Assessing Personal Risks:

- Description: Evaluating the likelihood and impact of each identified risk.

-

Considerations:

- How likely is the event to occur?

- What would be the financial impact of the event?

- What are the potential emotional and psychological consequences?

-

C. Handling Personal Risks:

- Description: Selecting and implementing appropriate techniques to manage personal risks.

-

Techniques:

- Risk Avoidance: Avoiding activities that create risk (e.g., not driving, avoiding risky hobbies).

- Risk Reduction: Taking steps to reduce the likelihood or impact of a risk (e.g., installing smoke detectors, exercising regularly, driving safely).

- Risk Transfer: Transferring the risk to another party, typically through insurance (e.g., purchasing life insurance, health insurance, auto insurance, homeowners insurance).

- Risk Retention: Accepting the risk and bearing the financial consequences of a loss (e.g., paying for small losses out of pocket, having an emergency fund).

-

D. Reviewing and Monitoring:

- Description: Regularly reviewing and updating the personal risk management plan to ensure that it remains relevant and effective.

-

Activities:

- Reviewing insurance coverage annually

- Adjusting risk management strategies as circumstances change (e.g., marriage, birth of a child, change in job)

- Monitoring financial performance and making adjustments as needed.

II. Key Areas of Personal Risk Management:

-

A. Life Insurance:

- Purpose: To provide financial support to dependents in the event of premature death.

-

Considerations:

- Amount of coverage needed

- Type of policy (term, whole life, universal life)

- Beneficiary designations

-

B. Health Insurance:

- Purpose: To cover medical expenses due to illness or injury.

-

Considerations:

- Type of plan (HMO, PPO, etc.)

- Coverage limits

- Deductibles and co-pays

-

C. Disability Insurance:

- Purpose: To provide income replacement if unable to work due to illness or injury.

-

Considerations:

- Definition of disability

- Benefit amount

- Waiting period

-

D. Property Insurance (Homeowners/Renters Insurance):

- Purpose: To protect against damage or loss to property.

-

Considerations:

- Coverage limits

- Deductibles

- Types of perils covered

-

E. Automobile Insurance:

- Purpose: To cover damage to vehicles and liability for injuries or damages caused in car accidents.

-

Considerations:

- Coverage limits

- Deductibles

- Liability coverage

-

F. Liability Insurance (Umbrella Policy):

- Purpose: To provide additional liability coverage beyond the limits of other insurance policies.

-

Considerations:

- Coverage limits

- Exclusions

-

G. Financial Planning and Emergency Savings:

- Purpose: To provide a financial cushion for unexpected expenses and losses.

-

Considerations:

- Amount of savings needed

- Investment strategy

-

H. Estate Planning:

- Purpose: To ensure that assets are distributed according to wishes after death.

-

Considerations:

- Wills

- Trusts

- Beneficiary designations

III. Benefits of Personal Risk Management:

- Financial Security: Provides peace of mind knowing that you and your family are protected against potential losses.

- Asset Protection: Helps protect your assets from being depleted by unexpected expenses.

- Reduced Stress: Reduces the stress and anxiety associated with uncertainty.

- Improved Quality of Life: Allows you to live a more comfortable and secure life.

No Comments