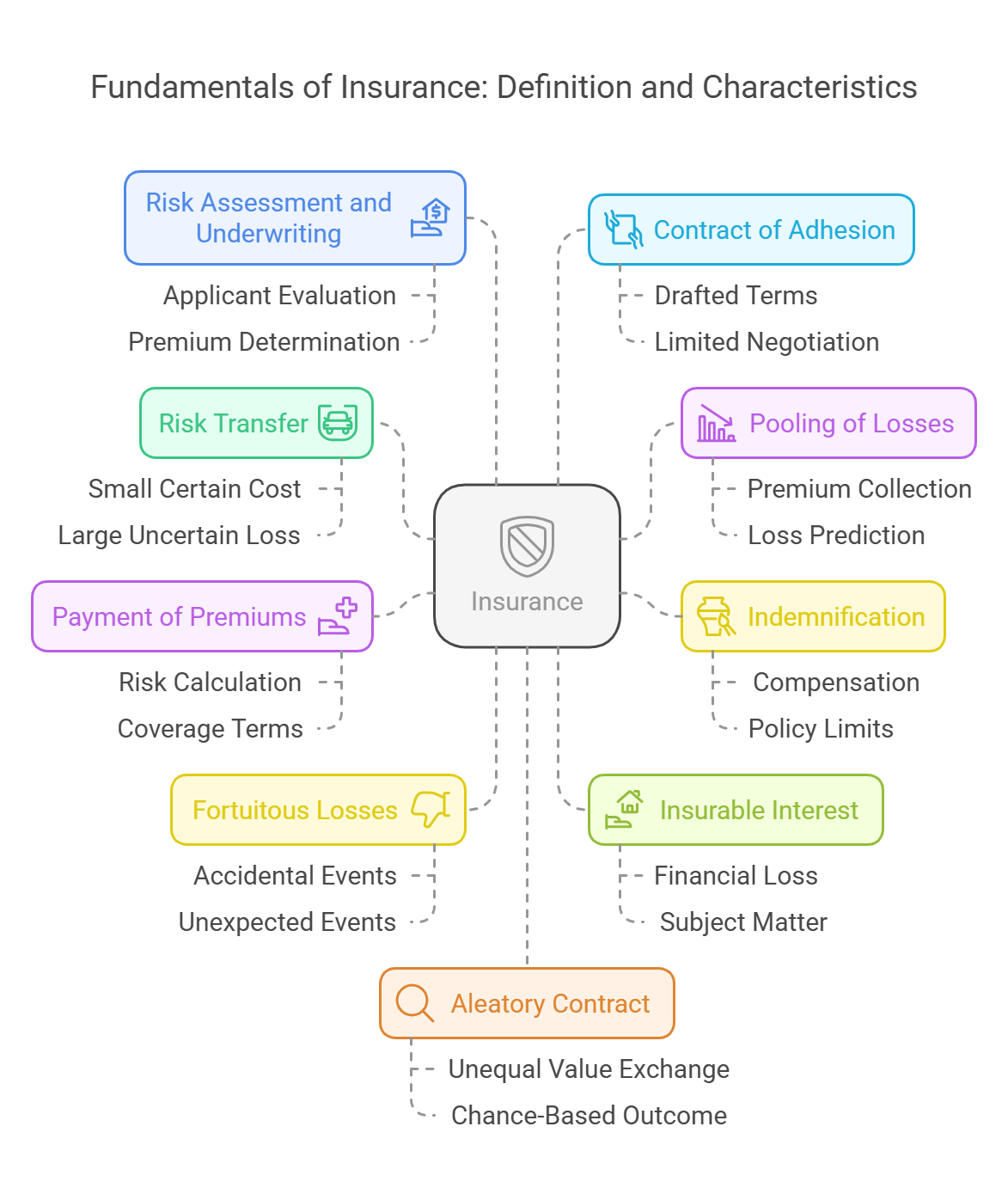

Insurance: Definition and Basic Characteristics

I. Definition of Insurance:

Insurance is a financial mechanism that transfers the risk of a potential loss from an individual or entity (the insured) to an insurance company (the insurer). In exchange for a premium, the insurer agrees to compensate the insured for specified losses if they occur during the term of the insurance contract (the policy).

Key Elements of the Definition:

-

Risk Transfer: The core function of insurance is to transfer risk from the insured to the insurer. The insured pays a relatively small, certain cost (the premium) to avoid the possibility of a large, uncertain loss.

-

Indemnification: Insurance aims to restore the insured to the financial position they were in before the loss occurred. This is known as indemnification. The insurer compensates the insured for the actual losses incurred, up to the policy limits. Note that insurance typically does not allow the insured to profit from a loss.

-

Pooling of Risks: Insurers pool the risks of many individuals or entities, allowing them to predict losses more accurately and spread the cost of those losses across a large group.

-

Contractual Agreement: Insurance is based on a legally binding contract (the insurance policy) that specifies the terms and conditions of coverage, including the perils covered, the policy limits, and the premium.

II. Basic Characteristics of Insurance:

-

A. Risk Transfer: (As mentioned above) This is the fundamental characteristic. The insured transfers the financial risk associated with potential losses to the insurer.

-

B. Pooling of Losses: Insurers collect premiums from a large number of insured parties and use these funds to pay for the losses of a smaller number of insured parties who experience covered losses. This pooling allows insurers to predict losses more accurately and spread the cost of those losses across a large group.

-

C. Indemnification: The insurer agrees to indemnify (compensate) the insured for covered losses, up to the policy limits. The goal is to restore the insured to their pre-loss financial position, not to provide a profit.

-

D. Payment of Premiums: The insured pays a premium to the insurer in exchange for the insurance coverage. The premium is calculated based on the risk of loss, the policy limits, and other factors.

-

E. Fortuitous Losses: Insurance typically covers losses that are accidental and unexpected (fortuitous). Losses that are intentionally caused by the insured are generally not covered.

-

F. Insurable Interest: The insured must have a financial interest in the subject matter of the insurance. This means that the insured must stand to suffer a financial loss if the insured event occurs. For example, a homeowner has an insurable interest in their home.

-

G. Risk Assessment and Underwriting: Insurers assess the risk of loss associated with each applicant and decide whether to offer insurance coverage and at what premium. This process is called underwriting. Insurers use various factors to assess risk, such as age, health, occupation, and location.

-

H. Contract of Adhesion: Insurance policies are typically contracts of adhesion, meaning that the terms are drafted by the insurer, and the insured has little or no opportunity to negotiate the terms. Any ambiguities in the policy are generally interpreted in favor of the insured.

-

I. Aleatory Contract: An insurance contract is aleatory, meaning that the outcome depends on chance. The value exchanged by the parties is unequal. The insured may pay premiums for many years and never experience a covered loss, or they may experience a covered loss shortly after purchasing insurance.

-

J. Utmost Good Faith (Uberrimae Fidei): Both the insured and the insurer have a duty to act in utmost good faith and to disclose all material information relevant to the insurance contract. This is particularly important during the application process.

Understanding these characteristics is essential for comprehending the fundamental principles of insurance and how it operates as a risk management tool.

Understanding these characteristics is essential for comprehending the fundamental principles of insurance and how it operates as a risk management tool.

No Comments