Rate Making

Rate making, also known as ratemaking or pricing, is the process of determining the premium rates that insurance companies charge for their policies. It is a critical function that ensures the insurer's profitability and solvency while providing affordable coverage to policyholders.

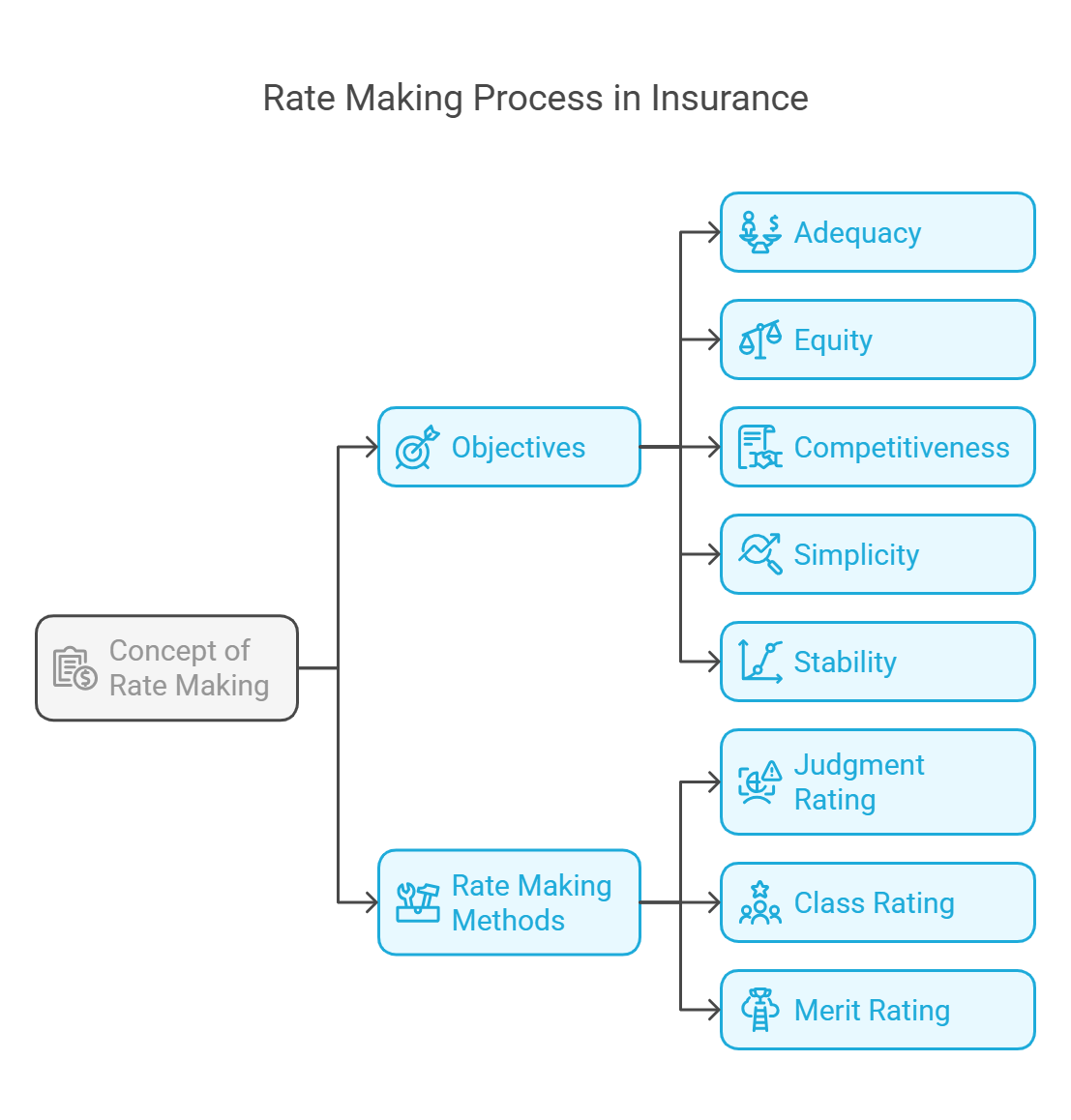

I. Concept of Rate Making:

I. Concept of Rate Making:

-

A. Definition:

- Description: Rate making is the process of estimating the expected cost of future losses and expenses and allocating those costs to individual policyholders in the form of premium rates.

- Goal: To establish rates that are adequate to cover expected losses and expenses, while also being competitive and affordable.

II. Objectives of Rate Making:

-

A. Adequacy:

- Description: Rates must be adequate to cover the insurer's expected losses and expenses, including claims, administrative costs, and a reasonable profit margin.

- Importance: Ensures that the insurer can meet its obligations to policyholders and remain financially solvent.

-

B. Equity:

- Description: Rates should be fair and equitable, reflecting the risk presented by each individual policyholder.

- Importance: Prevents unfair discrimination and ensures that policyholders are not overcharged or undercharged based on their risk profile.

-

C. Competitiveness:

- Description: Rates must be competitive with those of other insurers in the market.

- Importance: Allows the insurer to attract and retain customers.

-

D. Simplicity:

- Description: Rates should be simple and easy to understand for both the insurer and the policyholder.

- Importance: Reduces confusion and disputes and makes the insurance product more attractive to customers.

-

E. Stability:

- Description: Rates should be relatively stable over time, avoiding large fluctuations that can disrupt the market.

- Importance: Provides predictability for both the insurer and the policyholder.

III. Rate Making Methods:

-

A. Judgment Rating:

- Description: Judgment rating relies on the underwriter's experience and judgment to determine the premium rate. It is used when there is limited statistical data available or when the risk is unique and difficult to classify.

- Process: The underwriter considers all relevant factors and makes a subjective assessment of the risk.

-

Use Cases:

- Unique or unusual risks

- New lines of business

- Situations where historical data is limited

-

Advantages:

- Flexibility

- Ability to account for unique circumstances

-

Disadvantages:

- Subjectivity

- Inconsistency

- Potential for discrimination

-

B. Class Rating (Manual Rating):

- Description: Class rating involves classifying risks into groups (classes) based on their shared characteristics and assigning a single rate to all risks within the same class.

-

Process:

- Identify Rating Factors: Determine the factors that are most predictive of losses (e.g., age, gender, location, driving record).

- Create Rating Classes: Group risks into classes based on these factors.

- Calculate Base Rates: Calculate the average loss cost for each class.

- Adjust for Expenses and Profit: Add a loading for the insurer's expenses and profit margin.

-

Use Cases:

- Auto insurance

- Homeowners insurance

- Other lines of business with a large volume of similar risks

-

Advantages:

- Objectivity

- Consistency

- Efficiency

-

Disadvantages:

- May not accurately reflect the risk of individual policyholders

- Can be inflexible

-

C. Merit Rating:

- Description: Merit rating adjusts the class rate to reflect the individual characteristics of the policyholder. It rewards policyholders with good loss experience and penalizes those with poor loss experience.

-

Types:

- Schedule Rating: Credits or debits are applied to the class rate based on specific factors related to the risk (e.g., safety features, loss control measures).

- Experience Rating: The class rate is adjusted based on the policyholder's past loss experience.

- Retrospective Rating: The final premium is adjusted based on the policyholder's loss experience during the policy period.

-

Use Cases:

- Workers' compensation insurance

- Commercial auto insurance

- Other lines of business where individual risk characteristics are important

-

Advantages:

- Fairness

- Incentivizes loss control

-

Disadvantages:

- Complexity

- Potential for manipulation

IV. Numerical Examples (Simplified)

-

Example 1: Class Rating

- Scenario: An insurer is rating auto insurance for drivers in two age groups: 16-24 and 25+.

-

Data:

- Expected loss cost for 16-24 year olds: $1,000 per year

- Expected loss cost for 25+ year olds: $500 per year

- Expenses and profit margin: 20% of premium

-

Calculation:

- Premium for 16-24 year olds: $1,000 / (1 - 0.20) = $1,250

- Premium for 25+ year olds: $500 / (1 - 0.20) = $625

-

Example 2: Merit Rating (Experience Rating)

- Scenario: A company's workers' compensation insurance is experience rated.

-

Data:

- Class rate: 5% of payroll

- Experience modification factor: 0.8 (due to good loss experience)

- Payroll: $1,000,000

-

Calculation:

- Standard premium: 0.05 * $1,000,000 = $50,000

- Experience-rated premium: 0.8 * $50,000 = $40,000

No Comments